Reports & Research

Explore proprietary research packed with data, insights, and real-world findings to help carriers make smarter decisions.

New Research: "Hail Risk 2024: An Interactive Guide for Insurers"

The landscape of hail risk management is undergoing a significant transformation. Our latest publication, "Hail Risk 2024: An Interactive Guide for Insurers," offers a critical examination, illustrated with compelling data, of the factors contributing to the alarming rise in hail-related losses over the last decade. Major changes to how hail is understood have changed how insurers should view the peril. This guide isn't just about understanding hail risk; it's about redefining how it is managed in the insurance industry.

Why This Guide is Indispensable:

- Losses Rising — Understand the key factors driving record-breaking hail losses, and why there's more to the story than just "climate change."

- Reinsurance — Learn why insurance carriers now shoulder more of the burden due to changing risk transfer relations.

- The Right Tools — Explore how AI-based climate risk models are supplementing stochastic and actuarial models for a full picture of climate risk.

- Actionable Steps — See how leading carriers are applying granular, property-level insights and learn the proactive steps they're taking to mitigate risks and losses.

Ready to get up to speed on hail risk in 2024? Access the guide.

Future-Proofing Insurance: How to Prepare for Intensifying Wildfire Seasons

As ZestyAI unveils its annual Wildfire Season Overview, we can see that insurers are in a pivotal position to navigate the ongoing threat.

The insurance industry has been grappling for years with the skyrocketing losses caused by wildfires. As ZestyAI unveils its annual Wildfire Season Overview, we can see that insurers are in a pivotal position to navigate the ongoing threat.

Wildfire Risk Isn’t Going Anywhere

While we are currently experiencing a brief reprieve from the wildfire devastation of the last few years, the ongoing threat of wildfire remains at an all-time high.

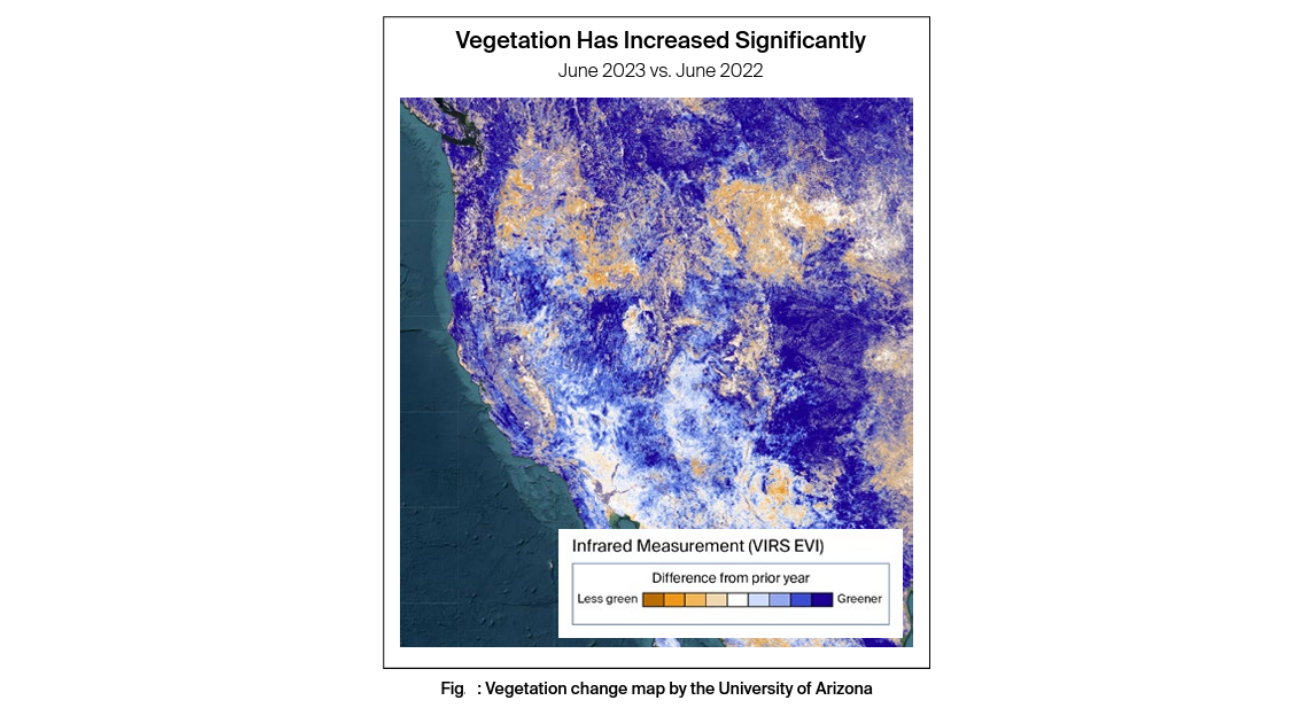

Extreme snow and rainfall across the West in 2023 have led to wetter-than-normal conditions that have acutely reduced the risk of wildfire. However, wetter conditions lead to vegetation growth, so despite 2023 presenting lower wildfire risk, the resulting vegetation accumulation, combined with persistent drought conditions in future years, will likely result in extremely high losses in the coming years. In fact, heavy rainfall has preceded many of the most severe wildfire years ever recorded in California.

Heavy rainfall has preceded many of the most severe wildfire years ever recorded in California.

Preparing for Future Wildfire Seasons

With high wildfire activity on the horizon, what steps can insurance companies take now to prepare for future wildfire seasons?

Here are three essential strategies:

1. Leverage Data for Better Understanding

Research by ZestyAI reveals that wildfires ravage 87% more land during drought years compared to non-drought years. With the western US still experiencing a megadrought that is the worst in over a millennium, it’s critical to understand the data and risks involved.

Not all homes face high risk. For the remainder, detailed property risk insights can highlight areas requiring risk mitigation. Integrate property-specific wildfire risk data into the underwriting and renewal process. This year is also an excellent opportunity to review a complete portfolio using an AI-powered wildfire risk assessment tool like Z-FIRE.

2. Educate and Empower Property Owners Through Transparency

Technology, particularly satellite/aerial imagery and artificial intelligence, can shed light on wildfire risks. Insurers can use this technology to assess the risk reduction measures that policyholders have implemented and understand how a property might withstand a wildfire.

This information is invaluable for educating homeowners and insurance agents. By knowing the specific actions that can be taken to reduce risk, such as clearing brush or using fire-resistant materials, both insurers and homeowners can be better prepared for wildfires.

3. Choose a Technology Partner Wisely

ZestyAI's Z-FIRE has set a benchmark by integrating loss data from over 1,500 wildfires and employing cutting-edge technology to derive insights on each property. By combining aerial and satellite imagery with machine learning and cloud computing, ZestyAI created Z-FIRE, a highly detailed wildfire risk assessment model.

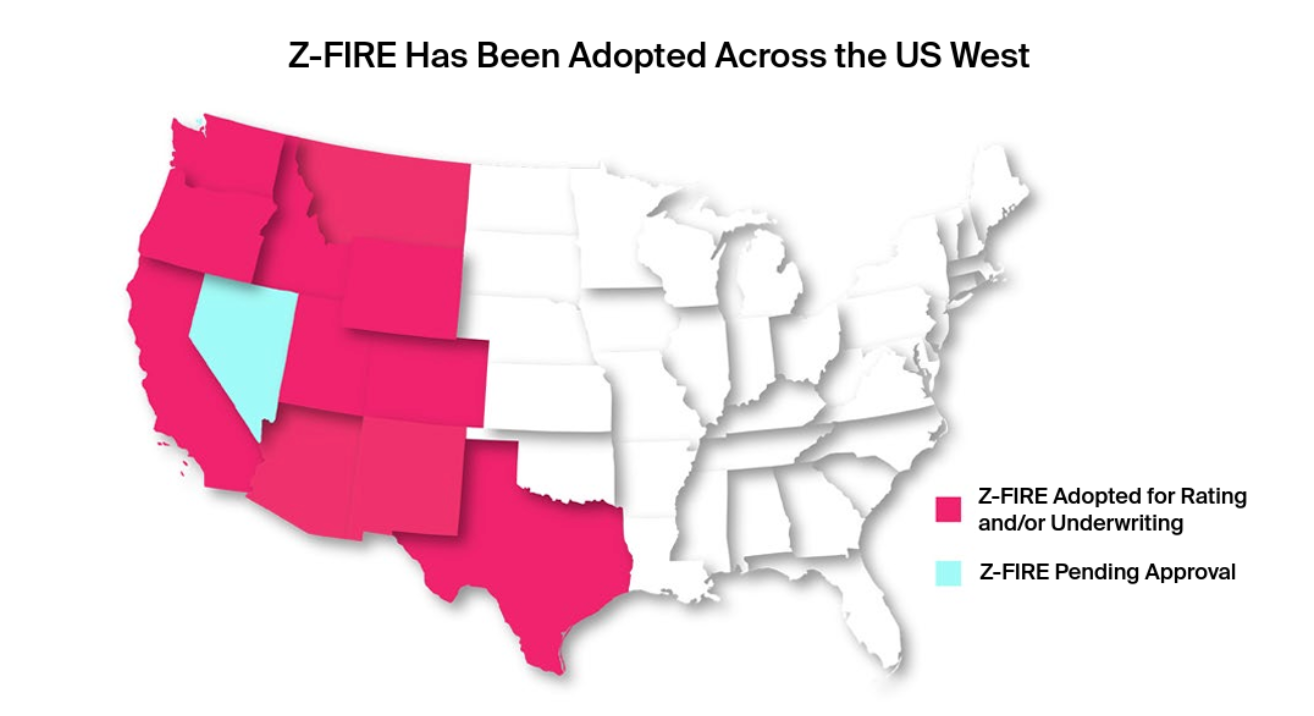

Z-FIRE has been adopted by leading insurance carriers in every single western US state.

In 2022, Z-FIRE demonstrated remarkable performance. Its integration of data through machine learning and computer vision models has established Z-FIRE as a potent tool in wildfire risk assessment for both underwriting and rating.

Make Informed Decisions with Z-FIRE

Using Z-FIRE, insurance carriers, MGAs, and reinsurers can get access to actionable insights developed from detailed property-level risk factors. While wildfire losses may be inevitable, understanding in detail how individual properties contribute to average and tail risks is a large step forward.

The specific time and location of a wildfire is nearly impossible to predict. However, Z-FIRE can give carriers an assessment of the preconditions for that fire, and describe in detail the factors which contribute to it. Knowing, not guessing, which properties fall into a high-risk category is more important now than ever. We look forward to helping our customers through this fire season and many to come.

Z-FIRE Stands Alone in Compliance

Z-FIRE has been developed in partnership with top carriers and has been included in successful filings in California and many other western states. As regulators continue to push for additional transparency and accuracy in how insurers treat wildfire risk, AI-powered solutions provide a clear advantage because of their interpretability and sensitivity to changing conditions.

In 2023, California began requiring insurers to provide discounts based on mitigation measures, and in 2024 Oregon is poised to establish similar requirements on communications to homeowners. All of these changes create a burden on insurers, but those who can adapt to the new regulatory environment by leveraging knowledgeable partners like ZestyAI will have an advantage over competitors. AI is part of the solution, helping address climate risk and maintaining the insurability of properties across the US.

Download ZestyAI's 2023 Wildfire Season Overview

_(1440_%25C3%2597_800_px)_(2).png)

2023 Wildfire Season Overview: The Calm Before the Storm

ZestyAI has released its annual Wildfire Season Overview for 2023. This comprehensive report provides insights to assist insurers in effectively managing wildfire risk.

ZestyAI has released its annual Wildfire Season Overview for 2023. This comprehensive report combines insights from recent wildfire events, prevailing drought conditions, and cutting-edge advancements in artificial intelligence to assist insurers in effectively managing wildfire risk.

Download ZestyAI's 2023 Wildfire Season Overview

Here are some key findings from the report:

A Chance To Prepare While Wildfire Fuels Accumulate

Despite a brief respite from recent wildfire devastation, the current threat remains high. Over the past decade, wildfire risk has notably increased, particularly in California. However, the occurrence of extreme snow and rainfall in the West during 2023 has temporarily reduced the risk due to wetter conditions.

It's important to note that vegetation accumulation and ongoing droughts will likely lead to substantial losses in the coming years. California remains highly susceptible to losses and significant vegetation growth. This temporary relief in 2023 creates an ideal opportunity for insurers to review the risk technologies they have in place and embrace innovative solutions to prevent future losses.

No Role for Drought in Underwriting

Drought is indicative of fire intensity, but not losses. Although drought is an important factor in seasonal wildfire risk, the presence of drought shouldn't drive underwriting. Instead, insurers should look at property-specific solutions that consider wildfire risk over the lifetime of a policy.

Research has shown that this year's heavy rainfall may be a leading indicator for severe wildfire years to come. A comprehensive understanding of buildings, vegetation, and mitigation methods at the property level is necessary to effectively manage future wildfire risk.

A comprehensive understanding of buildings, vegetation, and mitigation methods at the property level is necessary to effectively manage future wildfire risk.

Using Advanced Models to Adapt to Changing Risks & Regulations

AI-powered risk models play a key role in mitigation. Insurers who write business in wildfire states have found increasing value in AI-powered wildfire risk models as they offer actionable risk insights, adapt quickly to changing climate risks, and comply with all regulations.

Over the last year, several western states have begun to implement new regulations for insurers in response to the changing risk environment. Discounts and transparency for mitigation efforts and property-specific decisions may become an industry standard as they have in California and Oregon.

What This Means for Insurers

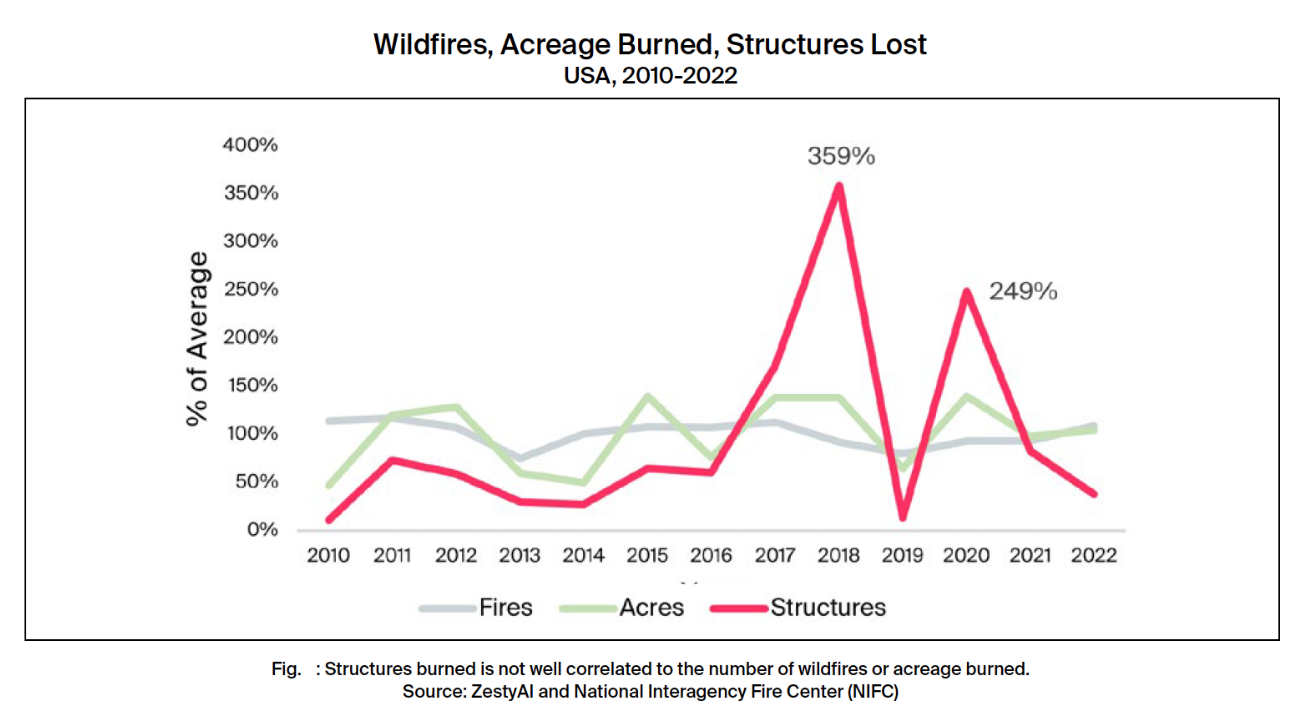

In evaluating wildfire risk, many analyses tend to focus on the number of fires and the size of the area they burn. However, what really matters to insurance companies and property owners is the loss of structures and what can be done to mitigate those losses.

For example, those providing insurance in California might be surprised to learn that despite smaller losses in 2022 compared to 2021, the total national count of acres burned and fires ignited in 2022 actually exceeded that of 2021. This mismatch between yearly wildfire activity and the number of structures lost suggests that wildfire losses are not simply dictated by wildfire activity.

The most significant factor is not how many fires start, or how far they spread, but the potential resilience of every structure and what the communities and homeowners have done to prepare for wildfire exposure. Research from ZestyAI and IBHS shows that for a more precise understanding of potential losses, insurers need to zoom in on individual properties. They should consider a structure’s location, building materials, surrounding vegetation, and efforts taken by the surrounding community to prepare for wildfires.

Modern wildfire risk tools like ZestyAI's Z-FIRE do just that. They analyze individual property features and measure the impact of those features on the probability of loss. They also factor in nearby vegetation, community preparations, local infrastructure, and the lay of the land. This property-centric approach doesn’t try to predict exactly what a wildfire will do. Instead, it gives valuable information on how and why properties might be damaged by wildfires.

These models don't just offer a simple risk score, but also help explain what makes a particular property vulnerable and what steps can be taken to protect it.

Find out more, including how Z-FIRE performed in 2022, in this year’s Wildfire Season Overview.

Download ZestyAI's 2023 Wildfire Season Overview

.png)

As Hail Damage Continues Across the U.S., New Research From ZestyAI and IBHS Works to Make Hail Losses More Predictable

Research considers valuable data on smaller hailstone impacts, which are likely responsible for 99 percent of the impacts on a roof from a hailstorm.

San Francisco, CA, April 19, 2023 – Today ZestyAI, the leading provider of climate and property risk analytics solutions powered by artificial intelligence (AI), and the Insurance Institute for Business & Home Safety (IBHS) released new research examining catastrophic losses from severe convective storms, particularly hail. The study focuses on hail-driven losses in property and casualty insurance.

Hail losses are a persistent problem for property insurers’ risk management efforts. Historically, carriers have focused on intense events to predict hail risk, with supporting data confined to storms with hailstones larger than one or two inches. The study Small Hail, Big Problems, New Approach shows high concentrations of small hail are more important than previously thought, pointing to an opportunity to broaden data sets to account for the cumulative effect all hailstorms have on a roof’s susceptibility to damage over time, leading to a claim.

This new research shows all hail needs to be accounted for when modeling and ultimately understanding losses. Using data from all hail events, not just those with hail that meet the severe criteria of one inch or greater, allows carriers to consider valuable data on smaller hailstone impacts. Additionally, insurers can integrate climate and materials science to better understand hail frequency and severity. Research suggests using this new approach could perform as much as 58 times more accurately than looking at events with large and very large maximum hail sizes alone, allowing carriers to more effectively assess hail risk, achieve more profitable underwriting and open up ratings to previously avoided areas.

“As we’ve learned more about hailstorms, we've discovered storms that produce large concentrations of small hail are more common than we thought, and despite causing less individual damage than a single large hailstone, small hail, especially in high concentrations, is likely a meaningful contributor to the loss we see each year from hail,” said Dr. Ian Giammanco, managing director of standards and data analytics at IBHS. “Experiments also show large concentrations of smaller hailstones cause degradation to the asphalt shingles, specifically dislodging large amounts of granules. Once enough granules are lost, the underlying asphalt material can become more susceptible to aging and weathering. Repeated exposure to these types of hailstorms can shorten the life of an asphalt shingle roof and increase the damage caused by large hailstones in the next storm.”

“Hail losses are a persistent problem for property insurers’ risk management efforts,” said Attila Toth, founder and CEO of ZestyAI. “Three of the nation’s five largest publicly-traded P&C carriers mentioned hail as a key concern in 2022 financial reports. Greater losses have brought attention to hail risk, and the insurance industry needs better approaches to solve this problem.”

“Three of the nation’s five largest publicly-traded P&C carriers mentioned hail as a key concern in 2022 financial reports. Greater losses have brought attention to hail risk, and the insurance industry needs better approaches to solve this problem.”

Hail risk can be especially costly to insurers because, unlike other catastrophic perils like hurricanes and wildfires, it can be difficult to identify the storm that caused a hail claim. As a result, insurance carriers could be forced to raise overall premiums or introduce high deductibles to compensate for the added costs.

As climate and materials science have developed, more data has become available providing improved hail risk evaluation options that can lead to better decisions at earlier stages of the policy life cycle. Other benefits could include more profitable underwriting, a greater ability to rate previously-avoided areas and significantly reduced loss ratios.

For the complete ZestyAI and IBHS research paper visit this page.

About ZestyAI

ZestyAI offers insurers and real estate companies access to precise intelligence about every property in North America. The company uses AI, including computer vision, to build a digital twin for every building across the country, encompassing 200 billion property insights accounting for all details that could impact a property’s value and associated risks, including the potential impact of natural disasters. Visit zesty.ai for more information.

About the Insurance Institute for Business & Home Safety (IBHS)

The IBHS mission is to conduct objective, scientific research to identify and promote effective actions that strengthen homes, businesses and communities against natural disasters and other causes of loss. Learn more about IBHS at ibhs.org.

###

For more information, contact:

Linsey Flannery

Director of Communications, ZestyAI

416-939-9773

Mary Anne Byrd

Communications Director, IBHS

803-669-4216

90-Second Fact Sheet: The Reinsurance Market in 2023

Reinsurance rates are spiking to an all-time high. Fitch estimated a 20-60% rate increase for cedants in the overall property reinsurance market at the January 1st renewals.1 Terms and conditions are also tightening - many reinsurers are limiting their cedants to much higher attachment points2, or exiting CAT-exposed lines altogether

The main drivers for uptick in reinsurance rates

Our research has found three drivers underpinning the trend:

1. Devastating CAT losses, particularly from secondary perils

59% of all CAT losses come from secondary perils3, and those losses have caused major shifts in the reinsurance landscape. Howden estimates that global property CAT reinsurance rates were up 37% at the January renewals4.

2. A new urgency to improve return on capital

“When the cost of capital is equal to the rate of return, something has to change.” - Aditya Dutt, CEO of Aeolus Capital Management5. The reinsurance industry has underperformed since 2017, with an average return on equity of just under 5%6. Poor underwriting performance was a key driver, with an industry average 101% combined ratio over the same period7. Reinsurers are poised to use the tightening market as a chance to improve performance, with Fitch forecasting a 4pp underwriting margin expansion for reinsurers in 20238. Unfortunately for primary insurers, Goldman Sachs predicts that the same tightening market will create significant volatility for cedants9.

3. Value erosion in reinsurer investment portfolios

Macroeconomic factors are driving significant unrealized investment losses for reinsurers, particularly on fixed income portfolios due to rising interest rates. Aon estimates that these investment portfolio losses drove a 17% decline in global reinsurance capital across the first 9 months of 2022, with some players reporting equity value losses as high as 40-50% over that period10. Reinsurers will look to shore up these losses with better underwriting performance, which likely means tougher rates for primary carriers.

How property insurers can improve their odds with AI-powered predictive climate and property risk platforms

These factors mean that primary insurers can expect challenging reinsurance negotiations at the June 1st renewal deadline, particularly on property lines. However, new AI-powered predictive climate and property risk platforms can improve the odds for property insurers in three areas:

1. Rapid improvements in risk mitigation

Implementation-free portfolio reviews can quickly drive major loss ratio improvements.

2. Turn the tables of CAT risk screening in your favor

Improving data quality can lead to more favorable stochastic model portfolio screens, particularly with insight about the roof.

3. Enter the room as a leader in cutting-edge risk practices

Showing the same commitment to new technologies as industry leaders can help cedants build a better case.

Conclusion

With the right mitigation action and a cutting edge view of portfolio risk, cedants can navigate the upcoming 6/1 renewal successfully.

Learn more about how an AI-powered predictive climate and property risk platform can help you.

------------------------------------------------------------------------

Sources

1 & 8 - Fitch, Reinsurers’ Underwriting Margins to Expand by 4pp in 2023

2 & 3 - Gallagher Re, Gallagher Re Natural Catastrophe Report 2022

4 - Howden, Howden’s renewal report at 1.1.2023: The Great Realignment

5 - AM Best, Reinsurance: Roundtable Discussion on Renewals and What 2023 May Hold

6, 7 & 10 - AON, Reinsurance Market Dynamics

9 - Reinsurance News, Hard market to increase volatility for primary insurers: Goldman Sachs

ZestyAI Announces 180-day Playbook to Navigate First-of-its-kind Wildfire Regulatory Requirements in California

Playbook Leverages Historic Regulatory Success of ZestyAI’s Wildfire Model (Z-FIRE™) to Lead Insurance Carriers Towards Regulatory Compliance in the Largest Insurance Market in the U.S.

San Francisco, CA, September 20, 2022 – ZestyAI, the leading provider of property risk analytics solutions powered by Artificial Intelligence (AI), has developed a 180-day playbook to support insurance carriers as they work to meet the Mitigation in Rating Plans and Wildfire Risk Models regulation expected to be adopted by the California Department of Insurance (CDI) before year-end. The playbook reflects the company’s unique ability as the only comprehensive solution in the marketplace to help insurers meet or exceed every single requirement in the new regulation — meeting 100 percent compliance inside the tight 180-day window.

On September 7, 2022, Insurance Commissioner Ricardo Lara announced he had submitted the department’s insurance rating regulation recognizing wildfire and safety mitigation efforts made by homeowners and businesses, to the California Office of Administrative Law for final approval. This first-of-its-kind regulation will require all insurers in California to refile their existing rating plans on an aggressive 180-day timeline.

“Eight of the ten most destructive wildfires in California’s history have occurred in the last five years,” said Attila Toth, Founder and CEO of ZestyAI. “While the new wildfire regulations will have a significant impact on California’s insurance industry, adapting to this peril is key to having a sustainable insurance ecosystem in California. As the leader in property-specific wildfire risk assessment, we have offered input at each step of this process. We are here to support admitted carriers with a turnkey solution complying with every single requirement as they navigate this process and work to meet the new regulations.”

The new wildfire safety regulation requires insurance companies to consider the structure of a home, its surroundings, and community-level mitigation. Insurers with concerns about the regulation can reach out to ZestyAI to get a complete explanation of how the regulations will impact them. This includes access to the 180-day playbook, which breaks down the regulatory compliance process into an orderly roadmap that addresses all three major challenges that insurers will face:

- Operational — The process of rapidly integrating new data sources, educating the public on how wildfire mitigation affects insurance policies, and a framework for a compliant appeals process.

- Rating — How to weight property-specific characteristics, including those with and without historical loss data, in rating plans as well as guidance on mitigation credits.

- Filing — Carriers who use a rating plan reliant on traditional wildfire models without property-specific information will need to overhaul their rating framework. Relying on multiple approved rate filings, ZestyAI has developed a comprehensive filing toolkit that can support carriers at every facet of the filing process.

ZestyAI’s Z-FIRE™ model has quickly become the leader in property-specific wildfire risk assessment. Using AI algorithms trained on more than 1,500 wildfire events across 20 years of historical loss data, Z-FIRE™ provides a level of detail that is of essential value to both the insurer and the homeowner.

The model was the first AI model ever approved as part of a rate filing by the CDI and the second wildfire risk model. It has been widely adopted across the Western U.S., where its use has been approved for both underwriting and rating. During 2021's APCIA Western Region Conference, CDI representatives expressed that the agency’s familiarity with Z-FIRE™ means in future filings the focus will be limited to the carrier's specific use of the model, not the details of the model itself, potentially greatly expediting the reviews of carriers using the Z-FIRE™ model.

ZestyAI’s Z-FIRE™ considers features such as topography and historical climate data in combination with factors extracted from high-resolution imagery of the property itself and its surroundings, including homeowner and community mitigation efforts, to provide both neighborhood and property-specific risk scores.

A significant advantage to insurance carriers is that they can use these data elements to communicate with homeowners on what specific actions can be taken to lower their property’s risk, such as upgrading building materials and cutting down surrounding dry brush or overhanging vegetation. The impact of mitigation efforts can be significant. A joint study by the Insurance Institute for Business & Home Safety (IBHS) and ZestyAI, which studied over 71,100 wildfire-exposed properties, found that property owners who clear vegetation from the perimeter of their home or building can nearly double their structure's likelihood of surviving a wildfire.

About ZestyAI

ZestyAI offers insurers and real estate companies access to precise intelligence about every property in the United States. The company uses AI, including computer vision, to build a digital twin for every building across the country, encompassing 200 billion property insights accounting for all details that could impact a property’s value and associated risks, including the potential impact of natural disasters. Visit zesty.ai for more information.

.png)

Now Streaming: The Hidden Redesign of P&C Insurance

What 2 Million Filings Reveal About 2026 Product Strategy

P&C Insurance Is Being Rewritten - Quietly but Rapidly.

Filings from the last three years show faster shifts in P&C products than at any point in recent history - and those changes are now surfacing at scale.

Endorsements, exclusions, deductibles, and appetite resets are reshaping coverage and competitive positioning across carriers. But the pace isn't uniform. National carriers, regionals, MGAs, and farm bureaus are moving in different directions - and most teams don't have visibility into how quickly competitors are adjusting forms and filings.

This session breaks down the signals that matter for 2026 product strategy.

Drawing on 2M+ carrier filings, Stephanie Kuczynski reveals the real trends reshaping P&C product strategy headed into 2026.

You'll learn what's accelerating, where carriers diverge, and how to translate these shifts into action.

What You Will Gain

- Which changes are accelerating fastest — and where carriers diverge. State-by-state adoption patterns for endorsements, deductibles, and coverage restrictions.

- How strategies differ by carrier size and focus — niche players vs. nationals. The creative, targeted approaches emerging from regionals and MGAs versus the broad strategies deployed by national carriers.

- Where regulators are drawing the line on coverage restrictions. Prepare for closer state-level inspection, due diligence, and shifting expectations across markets.

- How these shifts impact 2026 product strategy and competitive positioning. Why the pace and direction of changes matter — and how to ensure your strategy reflects where the market is heading.

Watch Now

Southern Oak Expands Use of ZestyAI After Nine Months of Proven Impact

Florida-based insurer broadens its use of ZestyAI as property-level intelligence becomes integral to portfolio management

ZestyAI today announced that Southern Oak Insurance Company has expanded its partnership with ZestyAI following nine months of demonstrated impact on portfolio decisions across its Florida homeowners portfolio.

Southern Oak initially adopted ZestyAI in 2025 to gain clearer visibility into property-level risk in one of the most complex and loss-prone insurance markets in the U.S.

Z-PROPERTY applies computer vision and machine learning across aerial imagery, building permits, tax assessment records, and other verified data sources to evaluate properties in 3D—assessing structural condition, exposure, and characteristics that influence claim frequency and severity across perils, including roof complexity, materials, and condition.

Tony Loughman, CEO of Southern Oak Insurance Company, said:

“Within months of deploying ZestyAI, it became clear that property-level intelligence needed to play a larger role in how we evaluate and manage risk. Expanding our partnership allows us to build on that foundation with greater confidence in the data behind our decisions, particularly in a market where roof condition, complexity, and exposure can materially impact outcomes.”

The expanded partnership reflects Southern Oak’s continued focus on proactive risk management in Florida’s volatile insurance environment, where traditional data sources often fail to capture the real condition and vulnerability of individual homes.

“Southern Oak’s decision to expand just nine months in is a strong signal of the value property-level intelligence delivers when it’s put into production,” said Attila Toth, Founder and CEO of ZestyAI.

“With Z-PROPERTY embedded in its risk decisions, Southern Oak sees risk more clearly, acts earlier, and makes more defensible decisions in a highly regulated, high-risk market.”

ZestyAI’s models are built with transparency, validation, and regulatory readiness at the forefront, giving insurers confidence to rely on them in portfolio decisions. The platform is used by leading insurers to improve underwriting accuracy, manage exposure, and reduce loss volatility across weather- and non-weather-driven perils.

Lilypad-Centauri Partners With ZestyAI to Strengthen Coastal Portfolio Using AI-Driven Risk Analytics

Lilypad-Centauri adopts roof and parcel-level insights to sharpen exposure data and strengthen risk decisions

ZestyAI today announced that Lilypad-Centauri is using ZestyAI’s Roof Age and Z-PROPERTY™ solutions to enhance its view of property risk across coastal homeowners and dwelling fire portfolios.

Lilypad-Centauri focuses on delivering stable and reliable coverage to homeowners and property owners in hurricane- and catastrophe-exposed coastal communities. By leveraging ZestyAI’s building attributes and parcel-level characteristics, Lilypad-Centauri gains a clearer view of property risk and how exposure accumulates across its coastal portfolio.

Lilypad-Centauri, through its managing general agency, is deploying two of ZestyAI’s proven solutions to gain a more granular, defensible view of property risk:

- Roof Age delivers verified roof age by cross-validating building permit records with over 20 years of aerial imagery, detecting roof replacement events, and assigning confidence scores across 97% of U.S. properties.

- Z-PROPERTY™ applies AI to high-resolution aerial imagery to assess roof complexity, materials, and condition, while evaluating parcel-level features such as vegetation overhang, yard debris, and secondary structures that influence claim frequency and severity across multiple perils.

“Coastal properties present a unique combination of exposure, from roof condition and construction features to how the parcel is maintained,” said Tony Hare, Chief Operating Officer & Chief Underwriting Officer of Lilypad-Centauri.

“ZestyAI’s roof and parcel-level analytics give us a clearer, property-level view of the homes we insure, helping us reduce uncertainty and better manage portfolio volatility.”

“Lilypad-Centauri is building a more resilient coastal portfolio by replacing exposure unknowns with verifiable property‑level truth,” said Attila Toth, Founder and CEO of ZestyAI.

“Granular, regulator-approved analytics bring confidence to the risk and capital decisions behind reliable customer protection.”

ZestyAI works closely with regulators to ensure transparency, validation, and continuous monitoring of its AI-driven models. Its portfolio of risk models has secured nearly 100 approvals from regulators nationwide, giving insurers confidence they can be deployed immediately with the accuracy and transparency regulators demand.

ZestyAI Provides AI-Driven Risk Analytics for Marsh McLennan Agency

MMA’s Private Client Services division adopts wildfire, roof, and parcel-level insights to drive better outcomes for its high-net-worth clients

ZestyAI, the Risk and Decision Intelligence Platform for the insurance industry, today announced that Marsh McLennan Agency (MMA), a subsidiary of Marsh (NYSE: MRSH), has adopted its risk analytics

By leveraging three cutting-edge solutions from ZestyAI, Z-FIRE™, Roof Age, and Z-PROPERTY™, the MMA Private Client Services team was able to improve wildfire risk evaluation for these homeowners by analyzing detailed property data and loss history and assessing roof age and condition using high-resolution aerial imagery. This strategic deployment enhanced their ability to offer more precise, customized insurance and risk management solutions for their clients’ high-value homes.

“Safeguarding the lifestyles and legacies of our clients requires a forward-looking approach to risk,” said Robert Pritula, Senior Vice President, National Placement and Solutions Leader of MMA’s Private Client Services division.

“We are always looking for new ways to leverage cutting-edge technologies that will allow us to offer clients tailored and effective solutions to mitigate the threats facing their most valuable assets, including their homes.”

“MMA has built its reputation on exceptional client service and proactive risk management,” said Attila Toth, Founder and CEO of ZestyAI.

“With granular risk analytics backed by industry standards and proven accuracy, they are leading the way in how high-value portfolios can be protected with confidence.”

ZestyAI works closely with regulators to ensure transparency, validation, and continuous monitoring of its AI-driven models. Its portfolio of models has secured more than 80 approvals from regulators nationwide, including Z-FIRE™, which has been approved across every wildfire-prone state, giving insurers confidence they can be deployed immediately with the accuracy and transparency regulators demand.

What Winter Storm Fern Reveals about Interior Water Losses and Systemic Risk

ZestyAI Product Insights

Winter Storm Fern has evolved into a historic catastrophe for the U.S. insurance industry. Between January 23-27, 2026, the storm shattered records by placing over 230 million Americans under severe winter alerts, with a death toll of 85 as of February 3rd.

Preliminary industry estimates place insured losses at $6.7 billion, potentially making Fern the third-costliest U.S. winter storm on record, trailing Elliott (2022) and Uri (2021). The crisis is far from over. The National Weather Service warns of a "historic duration" of extreme cold, with temperatures 15 to 25 degrees below average, that continues to hamper mitigation efforts.

For carriers, Fern is a complex, multi-peril challenge. Claims teams are navigating a surge of freeze-related losses, ice-driven structural damage, and widespread business interruptions across 34 states.

To understand the stakes, one needs to look no further than February 2021, when Winter Storm Uri brought Texas to its knees and generated over $11 billion in insured losses from a single state. Fern’s footprint is broader, and its secondary effects are still unfolding.

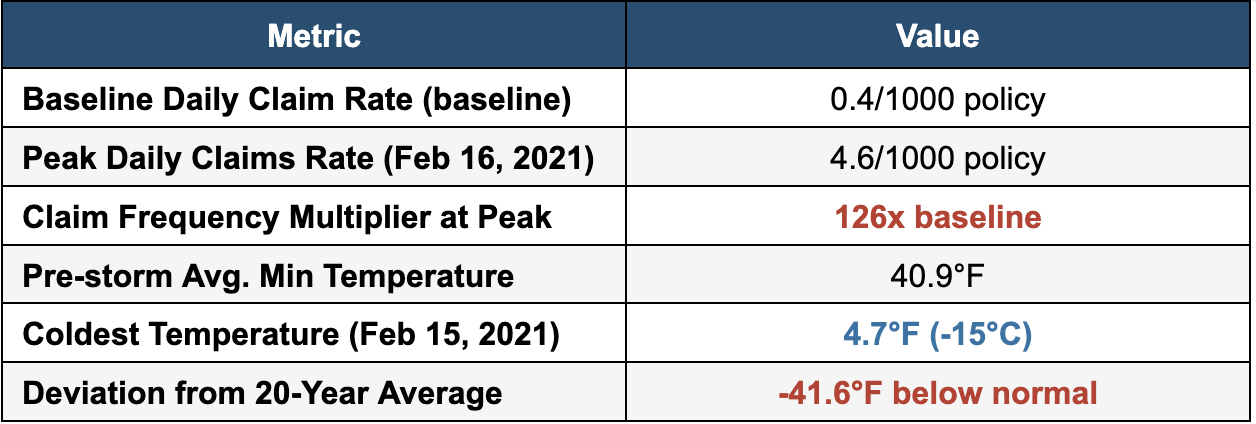

The Cold Hard Numbers from Storm Uri: Why Claims Explode Below 5°F

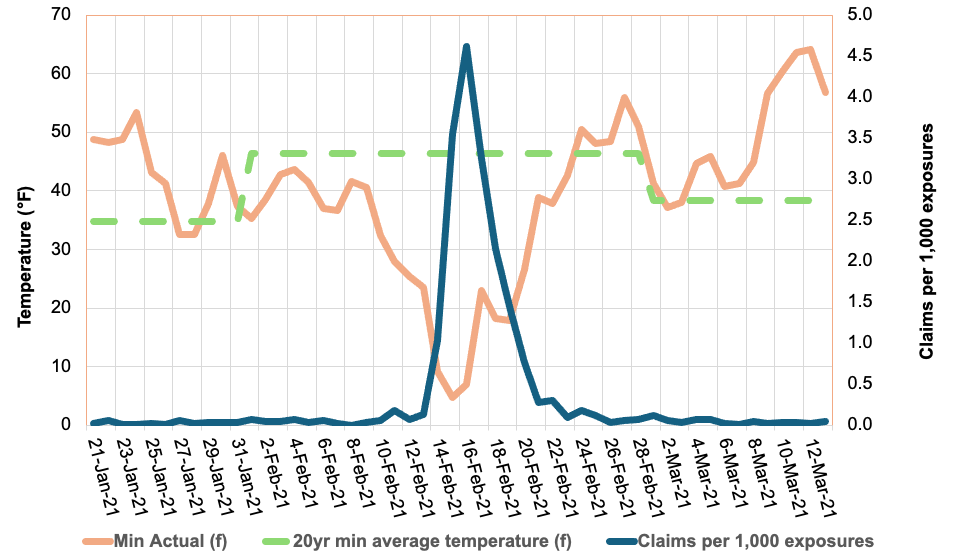

Our analysis of the 2021 Storm Uri reveals a striking relationship between temperature deviation and claim frequency for the non-weather water and freeze perils. Using data from multiple carriers, we tracked daily claim rates against minimum temperatures: before, during, and after the storm window (February 11-20, 2021).

The results show how rapidly falling temperatures can transform a routine winter pattern into a systemic loss event, allowing us to monitor the market’s response in real-time as conditions deteriorated, peaked, and normalized.

The results are dramatic:

Figure 1: Daily claim rates (blue line) surged 126X above the baseline in a temporal spike as temperatures (orange line) plunged below the 20-year average (dashed green line) during Winter Storm Uri.

The chart reveals a clear inverse relationship: as minimum temperatures dropped from the mid-40s°F to below 5°F, daily claim rates didn’t just rise, they increased 126X, from a baseline of 0.04% to 0.46% at the peak. This dramatic surge underscores the significant consequences of extreme cold events on insurance liability.

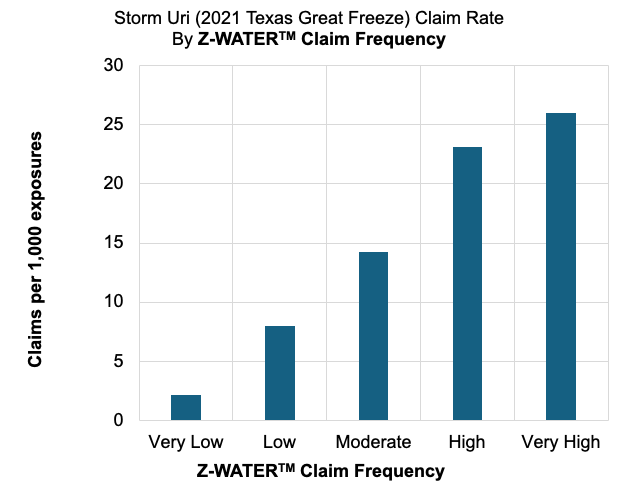

Figure 2: ZestyAI’s Z-WATER™ demonstrated an 11X increase in claim frequency between ‘Very High’ and ‘Very Low’ risk tiers during Winter Storm Uri

We used ZestyAI’s Z-WATER™ to segment the property-specific non-weather water risk across the 10-day storm window. Z-WATER™ is a risk model that accounts for how plumbing design, local climate, and infrastructure reliability interact to drive non-weather water and freeze losses. By capturing real-world dynamics, such as temperature swings that stress pipes and electrical grid failures that amplify claims, the model delivers a scientifically grounded view of property-level risk.

The results were definitive: properties that Z-WATER™ scored as ‘Very High’ risk filed 26 claims per 1,000, compared to just 2.2 claims per 1,000 for those scored as ‘Very Low’, an 11X increase in claim frequency.

This accurate segmentation reveals a clear path to managing volatility. Z-WATER™ provides a deep understanding of a home’s resilience across the full spectrum of loss mechanisms, from everyday plumbing failures to expensive outlier events like Storms Uri and Fern. By enabling precise intra-territory risk splitting, the model allows carriers to price and underwrite more reliably, ensuring premiums reflect the true risk profile while protecting the portfolio against systemic losses.

The January 2026 Storm: History Rhyming?

While we can already see the immediate impact of Winter Storm Fern, the primary difference between Fern and Winter Storm Uri is the duration of the freezing event itself, rather than any changes in how quickly policyholders are filing their claims.

As shown in Figure 1, NWW claims rise rapidly as temperatures fall and taper off quickly once conditions normalize. The risk in prolonged cold events lies in how long properties stay below the Plumbing Design Temperature; the longer the freeze, the greater the likelihood of systemic plumbing failure.

During Winter Storm Uri, extended sub-freezing conditions significantly increased the number of days in which vulnerable properties were exposed to frozen pipe failures, driving aggregate losses to historic levels. Fern is now exhibiting a similar duration profile, with sub-freezing conditions persisting for up to 10 consecutive days across parts of the Northeast. The National Weather Service has warned this “could be the longest duration of cold in several decades,” raising the likelihood of elevated losses even if individual claims remain tightly clustered in time.

For carriers, the warning signs are already flashing:

- The Power Failure Multiplier: During the storm's peak, over 1 million customers lost power. In the South, where homes lack the heavy thermal insulation of northern properties, a power outage is the primary driver of catastrophic pipe bursts. Without active heating, a property can reach the "burst threshold" within hours.

- The $30,000 Claim Severity Benchmark: Recent State Farm data underscores the high stakes of these events. Winter water damage claims totaled over $628 million, with the average claim payment now exceeding $30,000. For carriers, this high per-claim severity means even a moderate frequency surge can quickly erode Q1 margins.

- Regional Fragility in the South: While the initial assessments are still surfacing, early industry estimates for privately insured losses from Winter Storm Fern puts the damage at $4 billion to $7 billion. With Texas and Tennessee identified as the hardest-hit states, carriers are facing a "Uri-style" scenario in which infrastructure wasn't designed for a 10-day deep freeze.

From Reactive to Predictive: Solving the $6.7 Billion Freeze Risk Equation

The 2021 Texas freeze taught us that traditional approaches to freeze risk are highly insufficient. Many properties that experienced burst pipes were in areas that rarely see extended freezing temperatures, meaning they lacked adequate winterization.

This is where predictive analytics becomes essential. By modelling the interaction between property-level vulnerabilities and local temperature thresholds, carriers can better identify which properties are most vulnerable to freeze events before the damage actually occurs.

Key Risk Drivers Identified in Our Latest Analysis:

- The Design Mismatch: The greatest risk isn't just the cold; it's the sudden change in temperature. Properties in states like Texas or Tennessee face a higher risk because they are built to release heat, not trap it. They lack the heavy insulation and deep-buried pipes needed to survive a 10-day freeze.

- The Power Grid Vulnerability: Our analysis shows that areas prone to power outages face a compounded risk. In the South, a home’s primary defense is its heating system so when the power fails and the heater stops, the "burst threshold" can be reached in just a few hours.

- Building Vulnerabilities: Our analysis shows that older homes and properties with plumbing routed through exterior walls are disproportionately represented among $30,000 non-weather water losses.

The Bottom Line for Carriers

The 2021 Texas freeze was a pivotal moment for the industry, generating more than 500,000 claims and $11.2 billion in insured losses in a single state. Today, Winter Storm Fern represents an even broader systemic threat, with weather alerts impacting 230 million people across more than 30 states.

While the final tally for Fern is still developing, the data is already clear: temperature shocks drive claims at exponential rates. With early industry assessments estimating privately insured losses between $4 billion and $7 billion, it is evident that the prolonged duration and geographic anomaly of extreme weather events are the primary drivers of this volatility.

For carriers looking to protect their Q1 margins, predictive analytics are no longer a luxury; they are a requirement. By analyzing property-level characteristics, regional vulnerabilities, and historical temperature deviations, you can move from reactive claims handling to proactive risk management.

The question isn't whether another major freeze will occur, but whether your portfolio is prepared for the next 126-fold surge.

Learn More About Z-WATER

ZestyAI’s Z-WATER™ provides the industry’s most granular view of interior water risk, helping carriers accurately and reliably assess properties in areas prone to temperature shock events. By analyzing detailed property-level characteristics alongside historical weather patterns and regional risk factors, our advanced models predict the likelihood of Non-Weather Water (NWW) and freeze claims as well as their associated severity. This deeper level of analysis empowers carriers to make smarter pricing decisions before the next major storm hits.

Methodology: Analysis based on aggregated claims from multiple Texas carriers during Winter Storm Uri (February 2021). Temperature data reflects mean daily minimums across the exposure footprint, weighted by ZIP Code to account for geographic density. The claim/exposure ratio was calculated by dividing daily claims by the average policy-day exposure.

-----------------------------------------------------------------

1CNN Weather, "More than 230 million people under alerts for potential ice, heavy snow and extreme cold," January 2026. [link]

2Fox News, "Noem coordinates with Mississippi officials as state recovers from deadly winter storm," January 2026. [link]

3Insurance Innovation Reporter, “KCC Estimates $6.7 Billion in Insured Losses from Winter Storm Fern,“ February 2026 [link]

4Texas Department of Insurance, "Insured Losses Resulting from the February 2021 Texas Winter Weather Event," March 2022. [link]

5Fox Business, “More than 1 million Americans lose power as monster winter storm sweeps across the US,” January 2025 [link]

6Carrier Management, “Frozen Pipes Lead to $628M in Losses for State Farm,” January, 2026 [link]

7 Barrons, “Winter Storm Fern Packed a Wallop. Now the Cost Estimates Are Rolling In.,“ February 2026 [link]

Logic Underwriters Adopts ZestyAI to Strengthen Texas Property Underwriting with AI-Powered Hail and Wind Models

Storm and property insights help inform risk-aligned coverage decisions

ZestyAI today announced that Logic Underwriters has adopted ZestyAI’s Z-PROPERTY™, Z-HAIL™, and Z-WIND™ solutions to improve underwriting and rating precision across its personal and commercial property portfolio in Texas.

Texas is the most expensive severe convective storm market in the United States, with hail and damaging wind driving billions of dollars in insured losses every year.

"Texas is one of the most challenging storm markets in the U.S., and we need tools that match that reality," said Bill Motz, Director of Operations, Logic Underwriters.

"ZestyAI's detailed property insights and dedicated hail and wind models will help us continue to provide exemplary service to our clients—from more accurate risk assessments to better loss prevention guidance in increasingly volatile weather conditions."

ZestyAI’s property-specific hail and wind models predict the likelihood and severity of storm-driven claims by analyzing how local climatology interacts with detailed property characteristics—helping underwriters to distinguish meaningful differences in risk within the same rating territory. Each model is trained on validated claims data, offering transparent explanations of the key factors driving risk.

Z-PROPERTY applies AI to high-resolution aerial imagery and multi-source data to assess roof condition, structural complexity, and parcel-level features such as vegetation overhang, yard debris, and secondary structures—factors that directly influence claim frequency and severity across multiple perils.

“Logic Underwriters is exactly the kind of forward-looking partner that is redefining underwriting in high-exposure states,” said Attila Toth, Founder and CEO of ZestyAI.

"This collaboration shows how property-level intelligence can support underwriting excellence and disciplined decision-making while helping policyholders better understand and protect their properties. When insurers can identify specific risk factors like roof condition or vegetation overhang, they can provide actionable guidance that helps clients reduce their exposure and minimize losses."

ZestyAI’s severe convective storm models are approved in 30 states, spanning the nation’s highest-exposure hail and wind markets, and used by leading insurers across the country.

See How Insights Turn Into Decisions

ZestyAI transforms data into action. Get a demo to see how the same AI powering our reports helps carriers make faster, smarter, regulator-ready decisions.