Resources

ZestyAI expands into the London market with MAP Underwriting partnership

Lloyd's of London managing agency adopts ZestyAI’s Z-FIRE™ to strengthen wildfire risk analysis across its property reinsurance portfolio

ZestyAI today announced MAP Underwriting (Managing Agency Partners), the Lloyd’s of London managing agency, as its first London-market customer. MAP has selected Z-FIRE™, ZestyAI’s wildfire risk model, to enhance how California wildfire exposure is evaluated and managed within its property (re)insurance portfolio.

The partnership marks ZestyAI’s first international expansion and highlights growing global concern from insurers about the impact of wildfires.

Operating Syndicate 2791 at Lloyd’s, MAP is widely respected for its underwriting discipline and technical approach to risk. The firm places exposure analysis at the center of its underwriting strategy, building its own view of risk by synthesizing the most relevant inputs while maintaining a deliberate balance of exposure across its portfolio.

In California, the structural and environmental conditions that drive loss can shift materially across short distances and change faster than broad-scale models can keep up with. That variability places a premium on the quality and resolution of the underlying data. Traditional models often smooth over these localized differences—introducing uncertainty into how exposure is differentiated and priced.

Z-FIRE addresses this gap by providing a more refined view of wildfire risk, predicting which properties are most likely to experience a wildfire and which are most likely to survive. Using computer vision and machine learning, the model captures how structural and environmental characteristics — defensible space, vegetation density, building materials, and topography — interact at the property level to drive loss outcomes, and is trained on the industry’s largest wildfire loss dataset.

Integrated into MAP’s underwriting framework, this intelligence strengthens its exposure analysis—helping the team more precisely distinguish wildfire risk across California and maintain a more consistent, data-driven understanding of portfolio exposure.

"At MAP, we build our own view of risk and rely on high-quality data that strengthens that perspective," said Nick Williams, Deputy Active Underwriter at MAP.

"Z-FIRE enhances MAP’s view of California wildfire risk with a higher-resolution view that integrates cleanly into our framework and supports more confident decisions across our portfolio."

"The London market is paying closer attention to wildfire than ever before, and the bar for hazard intelligence underneath that work has risen with it," said Attila Toth, Founder and CEO of ZestyAI. "MAP is one of the most respected property (re)insurance teams at Lloyd's, and partnering with them on California wildfire is a meaningful first step in bringing Z-FIRE to the broader London Market.

"This partnership highlights the growing international demand for greater risk intelligence solutions and marks an exciting new chapter for ZestyAI."

ACV roof endorsements jump 6x in a decade as carriers quietly rewrite homeowners insurance, ZestyAI analysis finds

Analysis of 2,000+ regulatory filings across more than 60 carriers reveals carriers are increasingly competing not on price, but on how policies present at claim time

- Among the top 10 US homeowners carriers, ACV roof settlement schedules grew from 10% adoption in 2015 to 60% in 2025; percentage deductibles increased from 60% to 90% of policies over the same period

- Cosmetic damage and anti-matching provisions among the top 10 carriers accelerated from 20% adoption in 2015 to 90% in 2025

- Across all ~60 carriers reviewed in catastrophe-exposed states, 93% now use percentage deductibles, 75% use ACV roof settlement schedules, and 49% include cosmetic damage exclusions

- A single roof claim today routinely faces four or more stacked coverage restrictions from one loss event

New analysis by ZestyAI of more than 2,000 homeowners insurance regulatory filings reveals a decade-long, industry-wide rewrite of the homeowners contract - one that has left the modern homeowners policy structurally different from the one sold even a few years ago.

While rising catastrophe losses, rate pressure, and tighter underwriting continue to dominate industry discussion, the analysis identified a more consequential shift: carriers are increasingly competing not on headline price, but on how policies present at claim time.

Among the top 10 US carriers, adoption of Actual Cash Value (ACV) roof settlement schedules has jumped six-fold, from 10% of policies in 2015 to 60% in 2025, while percentage-based deductibles spread from 60% to 90% of policies over the same period. Cosmetic damage and anti-matching provisions, once rare, have accelerated even faster: from 20% adoption in 2015 to 90% in 2025.

Using its regulatory intelligence platform ZORRO Discover™, ZestyAI analyzed more than 2,000 homeowners insurance filings across approximately 60 carriers operating in catastrophe-exposed states including Texas, Oklahoma, Colorado, Ohio, and North Carolina. The data shows that coverage restrictions, once isolated endorsements or niche products, have become foundational elements of the modern homeowners insurance contract.

Across all carriers reviewed, the analysis found that:

- 93% use percentage-based deductibles

- 78% apply age-based coverage triggers

- 75% use Actual Cash Value (ACV) roof settlement schedules

- 49% include cosmetic damage exclusions

- 30% require mandatory inspections as a condition of coverage

- 17% include anti-matching language

The research shows that carriers facing similar catastrophe pressures are not converging on a single product design. Instead, they are assembling similar coverage controls in different combinations depending on geographic concentration, operating model, and risk appetite.

Texas showed 100% adoption of percentage deductibles among reviewed carriers, while Oklahoma reached approximately 95%. ACV roof settlement schedules were most prevalent in Oklahoma (85%) and Texas (82%), while cosmetic damage exclusions appeared in 57% of reviewed Texas filings and 50% in Colorado.

The analysis also found that coverage restrictions are increasingly layered together rather than introduced individually. In many filings, a single roof claim is simultaneously subject to a percentage deductible, an ACV settlement schedule, an age-based payout trigger, and a cosmetic damage exclusion - creating up to four constraints on recovery from one loss event.

Despite the spread of these restrictions, the analysis found that policyholder dissatisfaction has not yet materially increased. Across the filings examined, coverage restrictions showed a negative correlation with complaint volume - potentially reflecting the fact that these controls can help moderate premium increases at the time of bind. As a result, many policyholders may focus more on their immediate rate than changes to policy language, with the financial impact of coverage restrictions often becoming visible only when a claim occurs.

Stephanie Kuczynski, Director of Risk Analytics at ZestyAI, said:

“Two policies can look nearly identical at bind and behave very differently at claim time. The difference is that one may achieve a lower premium by layering restrictions that shift more risk back to the policyholder. Consumers naturally focus on the price they pay today, while the cumulative impact of a percentage deductible, an ACV roof settlement schedule, an age-based trigger, and a cosmetic exclusion often doesn't become clear until a loss occurs. That's why a decade-long trend like ACV adoption jumping six-fold matters: the economics of a roof claim under those policies can look fundamentally different.”

Roof Coverage Restrictions in Homeowners Insurance: 2015–2025 Adoption Trends From Regulatory Filings

Among the top 10 U.S. homeowners carriers, adoption of Actual Cash Value (ACV) roof settlement schedules has jumped sixfold in a decade, from 10% of policies in 2015 to 60% in 2025. That's the headline finding from a ZestyAI analysis of more than 2,000 homeowners insurance regulatory filings across roughly 60 carriers, cited in a P&C Specialist article published July 1, 2026, by Jennifer Ortakales Dawkins, with commentary from ZestyAI's Director of Risk Analytics, Stephanie Kuczynski, on what a decade of coverage changes means for carriers and policyholders.

Read the full article in P&C Specialist →

How are carriers using ACV roof settlement schedules to manage roof exposure?

Carriers use Actual Cash Value (ACV) roof settlement schedules to cap claim severity on older roofs: the schedule pays the replacement cost of a roof adjusted for age and depreciation, rather than the full cost of replacing it. ACV is one of several coverage controls carriers use to limit exposure on aging roofs, alongside percentage-based deductibles, cosmetic damage exclusions, age-based payout triggers, and anti-matching provisions.

How fast is ACV roof settlement adoption growing among homeowners carriers ?

Sixfold in a decade among the top 10 U.S. homeowners carriers, from 10% of policies in 2015 to 60% in 2025. Looking at all ~60 carriers ZestyAI reviewed in catastrophe-exposed states, 75% now use ACV roof settlement schedules.

What other roof coverage restrictions are carriers filing?

ACV schedules are only one of several controls carriers are adding. Percentage-based deductibles spread from 60% to 90% of top-10 carrier policies over the same 2015-2025 period. Cosmetic damage and anti-matching provisions — once rare, limiting payouts for damage that's visible but doesn't affect a roof's function — accelerated even faster, from 20% adoption in 2015 to 90% in 2025.

Across all ~60 carriers ZestyAI reviewed in catastrophe-exposed states, the adoption rates were: 93% use percentage-based deductibles, 78% apply age-based coverage triggers, 75% use ACV roof settlement schedules, 49% include cosmetic damage exclusions, 30% require mandatory inspections as a condition of coverage, and 17% include anti-matching language.

How are carriers stacking multiple roof coverage restrictions?

ZestyAI's analysis found that a single roof claim today routinely faces four or more stacked coverage restrictions from one loss event: a percentage deductible, an ACV settlement schedule, an age-based payout trigger, and a cosmetic damage exclusion can all apply simultaneously. Kuczynski described one common pairing: "Attaching a higher flat deductible to your policy specifically targeting wind and hail losses puts a lot more skin in the game for the insured and does help to reduce the cost when claim time does come."

Which states have the highest adoption of roof coverage restrictions?

Texas and Oklahoma lead. ZestyAI found Texas at 100% adoption of percentage deductibles among reviewed carriers, with Oklahoma at approximately 95%. ACV roof settlement schedules were most prevalent in Oklahoma (85%) and Texas (82%), while cosmetic damage exclusions appeared in 57% of Texas filings and 50% of Colorado filings. Carriers facing similar catastrophe pressure aren't converging on one product design; they're assembling the same controls in different combinations depending on geographic concentration, operating model, and risk appetite.

Do roof coverage restrictions increase policyholder complaints?

Not so far. ZestyAI cross-referenced coverage restrictions against state insurance department complaint volumes and found a negative correlation; filings with more restrictions were associated with fewer complaints, not more. "There are less complaints coming in immediately, and theoretically that is due to premium breaks," Kuczynski said. "Everybody likes to have more cash, but we're not seeing any pushback from insureds for this loss of coverage."

Why are carriers layering coverage restrictions instead of relying on rate alone?

Coverage design can target roof-specific severity in ways base rate changes cannot. Controls like percentage wind/hail deductibles and ACV schedules shift a defined share of each loss back to the insured, reducing claim costs while funding the premium relief that appears to be keeping complaint volumes down. For carriers facing rate pressure in catastrophe-exposed states, coverage architecture has become a second lever alongside rate.

What does coverage architecture mean for carrier competitive strategy?

Coverage architecture, how coverage restrictions are layered within a policy, now differentiates carriers as much as rate, because two policies can look nearly identical at bind and behave very differently at claim time, according to Kuczynski. "The difference is that one may achieve a lower premium by layering restrictions that shift more risk back to the policyholder. Consumers naturally focus on the price they pay today, while the cumulative impact of a percentage deductible, an ACV roof settlement schedule, an age-based trigger, and a cosmetic exclusion often doesn't become clear until a loss occurs. That's why a decade-long trend like ACV adoption jumping six-fold matters: the economics of a roof claim under those policies can look fundamentally different."

The broader takeaway: as coverage design increasingly shapes what a roof claim actually pays out, clearer visibility into how these terms are layered — for carriers designing products, regulators reviewing filings, and policyholders comparing coverage — is becoming as important as the rate itself.

How can carriers benchmark their roof coverage against competitors?

Approved regulatory filings show which controls competitors have filed, in which states, and in what combinations. ZestyAI’s analysis drew on more than 2,000 homeowners filings across roughly 60 carriers to quantify adoption of ACV schedules, percentage deductibles, cosmetic exclusions, and age-based triggers. ZORRO Discover gives carriers this filing intelligence on demand: competitor coverage language, adoption rates, and state-by-state comparisons, so product teams can see where their own coverage architecture sits relative to the market.

Read the full article Shrinking Roof Lifespans Create a Pricing Problem for Home Insurers → P&C Specialist, July 1, 2026, by Jennifer Ortakales Dawkins. Includes ZestyAI's regulatory filing analysis and commentary from Stephanie Kuczynski, ZestyAI's director of risk analytics.

DUAL North America Expands Partnership with ZestyAI to Power Wildfire Underwriting in California

Z-FIRE™ to support new California program with property-level wildfire risk intelligence.

ZestyAI today announced that DUAL North America(“DUAL”) is expanding its partnership with ZestyAI to power wildfire underwriting for a new California homeowners program. As part of this expansion, DUAL will use Z-FIRE™ to assess wildfire exposure at the property level and support disciplined growth in catastrophe-exposed regions.

California continues to present significant wildfire volatility, requiring insurers to move beyond broad geographic indicators toward more granular, property-specific insights. Z-FIRE uses machine learning to evaluate each property’s unique characteristics—including defensible space, vegetation proximity, topography, building materials, and surrounding fire behavior patterns—to predict wildfire vulnerability at the individual structure level.

This property-level insight helps insurers identify structures most likely to suffer catastrophic loss, and those far more likely to survive a wildfire event.

“Launching a California program requires a disciplined, data-driven approach to wildfire risk,” said Luke Wolmer, Chief Actuary at DUAL.

“Z-FIRE delivers the property-level insight we need to confidently assess exposure, differentiate risk within the same territory, and offer coverage with greater clarity and consistency. That level of precision is essential as we grow our portfolio with greater confidence.”

This expansion builds on DUAL’s late-2025 adoption of Z-STORM™ to strengthen hail and wind underwriting across its U.S. portfolio, marking a rapid expansion of its use of the ZestyAI platform.

“After strengthening severe storm underwriting with Z-STORM, DUAL is now extending that strategy to wildfire with Z-FIRE.” said Attila Toth, Founder and CEO of ZestyAI.

“This expansion shows how insurers can grow responsibly in challenging markets when decisions are grounded in verified, property-level intelligence.”

Z-FIRE is approved across Western wildfire markets and was the first AI-based wildfire model approved as part of a carrier rate filing in California. ZestyAI’s broader portfolio of risk models has secured more than 200 regulatory approvals nationwide.

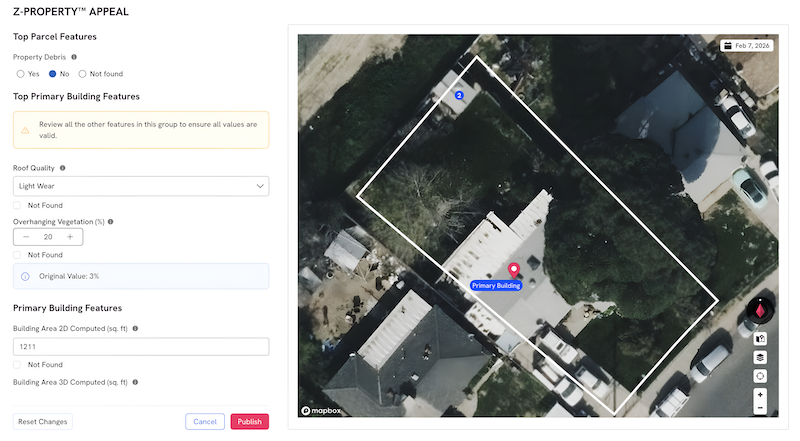

Mitigation-Aware Scoring: When a Property Changes, the Score Can Too

Property risk changes over time, but property data doesn't always keep up. A roof is replaced. Defensible space is cleared. Vegetation is removed. These improvements can materially change risk, yet the data behind a score often lags behind the property itself. That can mean overpricing lower-risk homes and frustrating policyholders who invested in mitigation. Mitigation-Aware Scoring gives carriers a governed, auditable way to update verified property attributes within the ZestyAI platform and recalculate risk when those changes affect the score.

What Mitigation-Aware Scoring Does

Mitigation-Aware Scoring allows authorized users to update property attributes within the ZestyAI platform when they have more accurate or more current information.

Some property attributes are used as inputs to ZestyAI risk models and may change the property's risk score when updated. Other attributes are informational only and update the property record without affecting the risk score.

Once submitted, the updated value is stored for that carrier and made available to the underwriting, pricing, and operations teams, so they can make decisions from the same property view.

It supports two review paths:

- Carrier-initiated review: When an underwriter, risk team, or operations team determines a property attribute should be adjusted, they can update it in the platform with an auditable record.

- Policyholder, agent, or inspection updates: When new information comes from a homeowner, agent, field inspection, or third-party source, authorized users can apply that information directly on the platform after the carrier's review process.

How Mitigation-Aware Scoring Works

The workflow happens in the ZestyAI platform:

- Search for the property by address

- Review property features and current model inputs

- Enter Mitigation-Aware Scoring mode and update the relevant property attribute

- Update the attribute value and review any resulting score changes

- Submit the change and preserve the audit trail

Carriers Stay in Control

The carrier controls how Mitigation-Aware Scoring is used.

Carriers determine:

- Which users can submit or manage updates

- How long each update remains in effect

- What evidence or internal process is required before an update is applied

Original and updated values appear side by side with dates, making every change traceable. Updates apply only within that carrier's environment, so one carrier's updates do not change another carrier's scores.

Available Across ZestyAI Models

Mitigation-Aware Scoring is now available across all ZestyAI risk models, including Z-FIRETM, Z-HAILTM, Z-STORMTM, Z-WINDTM, Z-WATERTM, and Z-PROPERTYTM.

The Bigger Picture

Mitigation-Aware Scoring gives carriers a practical way to ensure underwriting and pricing decisions reflect verified property improvements.

It helps carriers:

- Recognize completed mitigation and maintenance

- Support policyholder requests to review property risk scores

- Support underwriting and pricing based on current property conditions

- Maintain an auditable record of each update

To see how ZestyAI risk models can support your underwriting and pricing workflows, book a demo.

Frequently Asked Questions About Mitigation-Aware Scoring

What is Mitigation-Aware Scoring?

Mitigation-Aware Scoring allows insurers to update verified property attributes within the ZestyAI platform and recalculate property risk scores when those changes affect the model.

Can property updates change a ZestyAI risk score?

Yes. Updates to model-relevant attributes can recalculate the risk score, and the platform records every change.

Which ZestyAI models support Mitigation-Aware Scoring?

Mitigation-Aware Scoring is available across Z-FIRE, Z-HAIL, Z-STORM, Z-WIND, Z-WATER, and Z-PROPERTY.

Five ZORRO Discover Updates That Turn Rate Filings Into Market Intelligence

Rate filings are where competitors reveal their strategy. Every day, competitors signal where they are heading: which segments they want, which risks they are retreating from, which states they are prioritizing, and how regulators are responding. That information is public, but it is scattered across filings, PDFs, exhibits, objections, revisions, and supporting documents. Most teams still need to stitch that picture together manually: finding the relevant filings, extracting the data, adding market context, and interpreting what it means for pricing, product, and competitive strategy. The latest ZORRO Discover release adds five capabilities that help remove the biggest bottlenecks in filing research: benchmarking rate activity, researching objections, interpreting filings in market context, monitoring competitor moves, and getting filing data ready for analysis. Together, these updates reflect the pace of innovation behind ZORRO Discover: a platform built to expand how carriers use agentic AI for competitive and regulatory intelligence.

1. Reading Competitor Filings in Market Context

A filing is easier to interpret when teams know the carrier’s market position.

A rate change from a carrier with meaningful market share in a state may deserve more attention than a similar filing from a smaller writer. Without that context, teams can spend the same effort on filings that carry very different competitive weight. To assess the importance of a filing, an analyst usually has to look up market share for that carrier in a separate source, then return to the filing to interpret what it means.

The new Market-Share-Aware Chat brings annually reported carrier size and market position into ZORRO Discover responses.

Teams can run filing research with each carrier's market position in mind, so activity from the most relevant competitors surfaces first rather than getting lost among smaller, regional filings. For example, a search for separate wind/hail percentage deductibles in Texas may surface filings from carriers of very different sizes, making market context essential. ZORRO Discover can prioritize results from carriers with larger market positions, helping teams focus on the competitors most likely to shape the market.

The impact: a more focused competitive strategy based on relevant competitors, without switching between filings, market-share reports, and separate data sources.

2. Responding to Regulator Objections with Precedent

When a state department of insurance raises an objection, the response can shape the speed, defensibility, and outcome of a filing.

Teams need to know whether other carriers have faced a similar issue, how they responded, which responses succeeded, and which arguments drew more pushback. That requires digging through old filings, objection letters, response documents, and supporting exhibits. The right precedent may exist, but finding it is slow and inconsistent.

The new Objection Research helps teams find relevant precedent across more than two million filings.

Teams can surface similar objections, review how other carriers responded, and compare how regulators handled comparable issues. For example, a carrier in Florida facing an objection on its hurricane deductible methodology can see which responses succeeded on comparable filings and build on what worked, helping the team craft a stronger response and move through review faster.

The impact: faster objection resolution, fewer manual research cycles, and a clearer path to filing approval.

3. Knowing the Moment a Competitor Files

Important filings often surface too late.

Teams may discover a competitor filing through a manual SERFF check, a colleague, a meeting, or a leadership request. By then, the filing may already be approved, or the window to respond may be limited.

The new Watchlist helps teams monitor the carriers, states, lines of business, filing types, and rate-impact thresholds that matter to them. When a matching filing appears, ZORRO Discover delivers alerts by email and in-app.

For example, a homeowners carrier in Texas can monitor its top five competitors for material rate changes, track a specific line of business across the state, or set an alert on a keyword like "wildfire deductible" to catch relevant filings as they appear. That gives the team more time to brief leadership, evaluate the move, adjust pricing assumptions, or prepare a competitive response.

The impact: earlier visibility into competitor activity and less reliance on manual filing checks.

4. Turning Filing Tables into Analysis-Ready Data

Rate filings often include valuable data in tables, exhibits, factors, assumptions, relativities, and supporting schedules. Much of that data is locked inside PDFs.

Extracting it manually requires opening the document, finding the right table, copying or retyping values, and rebuilding the structure in a spreadsheet. That work is slow and can introduce errors.

The new Table Extraction pulls filing tables and exhibits into clean CSV files in one click, preserving structure and values for analysis.

For example, an actuary running competitor rate analysis in New Jersey can export rating factor tables directly from ZORRO Discover rather than manually copying data between PDFs.

The impact: analysis-ready data in minutes, without manual transcription.

5. Benchmarking Your Rates Against the Market

Before a carrier commits to a rate strategy, it needs a clear read of the market.

Understanding rate activity in a state or line of business means locating the relevant filings, extracting rate changes, comparing carriers, normalizing formats, and identifying which moves are material. That requires filing searches, PDF review, spreadsheet work, and manual normalization, repeated every cycle.

The new Rate Intelligence Dashboard brings key rate activity into a single view.

Pricing, actuarial, and product teams can compare rate changes across carriers, states, and lines of business. They can see who is moving rates, how large the changes are, which markets are seeing the most activity, and which filings carry the greatest business impact. For example, a carrier preparing for a Texas rate review can see how approved rate changes from competitors have trended over the past year and whether its planned action is directionally aligned with the market.

The impact: faster competitive benchmarking and better-informed rate review decisions.

The Bigger Picture

Each update removes a specific filing research bottleneck. Together, they shift filing research into a market intelligence workflow

ZORRO Discover brings assembly, analysis, and interpretation into one workflow.

Filings become structured, contextualized, monitored, exportable, and easier to interpret through an insurance-specific intelligence layer. The platform is built on ZestyAI's regulatory and competitive intelligence expertise, including experience with more than 200 filing approvals.

ZORRO Discover helps insurance teams turn millions of filings into citation-backed insights that reveal pricing trends, competitor moves, regulatory patterns, and market signals with up to 20X greater research efficiency. Get access to ZORRO Discover today.

Ready to see how ZestyAI works on your book of business?

Tell us a little about your needs. We'll show you how we reduce losses and help you price with precision.