Reports & Research

Explore proprietary research packed with data, insights, and real-world findings to help carriers make smarter decisions.

ZestyAI Publishes Data-Driven Look at 2022 Wildfire Season

2022 Wildfire Season Overview looks back at 2021 and ahead to what may be a long year of wildfires in 2022.

Today, ZestyAI released its 2022 Wildfire Season Overview. Each year, ZestyAI prepares a comprehensive overview to help guide insurers based on recent wildfire events, persistent drought conditions, and advancements in artificial intelligence for managing wildfire risk.

If it seems like wildfires are burning at all times of the year, it's not just you. Very destructive events, like last December's Marshall Fire, are occurring in months not typically associated with high wildfire danger. Those who study wildfires, including ZestyAI, have begun to start thinking in wildfire "years" instead of wildfire "seasons'. Strong wildfire years, with 10+ million acres burned, have quickly become the new normal. The last 10 years have been the worst on record for property and casualty (P&C) insurers when it comes to wildfire. 8 of the top 20 fires in California history, and more than half of the acreage burned by them, occurred in just the years 2020 and 2021.

What can insurers do to prepare themselves for persistent wildfires?

- Understand the Data: Instead of sticking with decades-old approaches, assess wildfire risk at the property level.

- Continue to Bring Transparency and Education to Homeowners: Insights from AI-based wildfire risk models may be passed on to homeowners and agents, enabling a much better understanding of wildfire risk.

- Find the Right Technology Partner: Aerial and satellite imagery, machine learning, and infinitely scalable cloud computing resources were combined to build the most granular wildfire risk assessment model (Z-FIRE™). Using Z-FIRE™, ZestyAI can accurately estimate an individual property’s wildfire risk, plus highlight the key property-level factors that contribute to that risk.

Click here to download ZestyAI's 2022 Wildfire Season Overview.

ZestyAI offers insurers and real estate companies access to precise intelligence about every property in North America. The company uses AI, including computer vision, to build a digital twin for every building in North America, encompassing 200B property insights accounting for all details that could impact a property’s value and associated risks, including the potential impact of natural disasters. Visit https://zesty.ai for more information.

The 2021 Wildfire Season has Devastating Potential

A Data-Driven Conversation about the US West’s Megadrought

Current climate conditions in the West reveal that 2021 may have a higher than normal risk for wildfire losses. While much of this report focuses on California, historically the worst victim of wildfire in the US, the entire western US is of concern in 2021. In particular, the expansion of deep drought into Colorado is of major concern.

Drought is a leading factor in seasonal wildfire risk. With drought extending through every western state this spring, insurers should consider looking deeply into how they are addressing this growing peril. According to AON, last year’s wildfires in the US West cost insurers over $8 billion.

We've released a complete detailing the devastating potential for 2021's wildfire season. The full report is available here.

Nearly Doubling a Property’s Wildfire Survival Rate: New Study from ZestyAI in Collaboration with IBHS Shows Impact of Key Mitigation Action

Research across more than 71,000 properties involved in wildfires draws significant links between fuel management and property survival.

Oakland,Calif., April 8, 2021: ZestyAI, a leader in climate risk analytics powered by Artificial Intelligence (AI), and the Insurance Institute for Business & Home Safety (IBHS) today released new research on how fuel management impacts destruction rates from wildfires. They found property owners who clear vegetation from the perimeter of their home or building can nearly double their structure's likelihood of surviving a wildfire.

ZestyAI, in conjunction with, IBHS studied more than 71,000 properties involved in wildfires between 2016 and 2019 to assess the relationship between vegetation, buildings, and property vulnerability. To do this, ZestyAI leveraged a combination of computer vision and AI to analyze high resolution satellite and aerial imagery of the properties that fell within the wildfire perimeter, which allowed them to determine what effects a property's physical environment had on its likelihood of survival. They found buildings with a high amount of vegetation within 5 feet of the structure were destroyed in a wildfire 78 percent of the time -- a rate nearly twice as high as those with small amounts of perimeter vegetation. This pattern held true as ZestyAI analyzed the other defensible zones, ranging from 30 to 100 feet around the property.

"It's common sense that increased vegetation increases wildfire risk, but this study shows just how powerful individual action can be in safeguarding structures. Mitigation actions that can cut risk nearly in half are statistically meaningful to anyone with a stake in this peril," said Attila Toth, CEO of ZestyAI. "These findings also underscore how wildfire research at IBHS and artificial intelligence at ZestyAI translates to real-world impact at the intersection of homeowners, community leaders, regulators, and insurance carriers. This type of collective action will help protect our communities from the devastating impact of wildfire, which unfortunately has continued to increase over the last decade."

The study also supported and confirmed takeaways from IBHS's Suburban Wildfire Adaptation Roadmaps released last year, which go beyond the home ignition zone to detail additional actions needed across eight aspects of a home to address a home's wildfire vulnerability. ZestyAI's new research found that having other structures in close proximity to a property increases its wildfire risk, particularly for properties in areas with moderate to high vegetation coverage. Buildings in these areas that had another structure within 30 to 100 feet from the property were destroyed in a wildfire 60 percent of the time, compared to a 31 percent destruction rate for homes without another structure in close proximity.

"This research further demonstrates to homeowners, community leaders, and policy makers just how impactful taking the mitigation actions laid out in the Suburban Wildfire Adaptation Roadmaps can be in protecting homes from wildfire ignition," said Roy E. Wright, President & Chief Executive Officer at IBHS. "Quantifying the effect of mitigating fuel density risk, one of the critical actions identified in the Roadmaps, is a first piece in the larger puzzle of what groups of mitigation actions most improve the chance of home survival and by what level."

ZestyAI is uniquely equipped to support this type of research because of the proprietary wildfire property loss database it developed for Z-FIRE™, its AI model that generates property-specific predictive risk scores. Z-FIRE™ has been trained on more than 1,200 wildfire events across several decades and accounts for the property-level factors that contribute to wildfire risk, including defensible space, building material, and roof pitch, which legacy models fail to consider.

Wright added, "While it is not possible to eliminate wildfire risk we are not powerless against it. We must take a pragmatic approach to mitigate risk at all levels and ultimately reduce property damage through data and science. Through collaborations with modelling organizations like ZestyAI, advanced technology like computer vision and AI help us better understand the impact of these actions at a larger scale. It is encouraging to see emerging progress in just the first months of 2021."

For additional insights you can read the full research paper, ‘Wildfire Fuel Management and Risk Mitigation - Where to Start?' here. For more information on ZestyAI please visit www.zesty.ai, and for more information on IBHS please visit www.ibhs.org.

About ZestyAI (www.zesty.ai): Increasingly frequent natural disasters, such as wildfires, floods and hurricanes devastated communities and drove $2.2 Trillion in economic losses over the past decade. ZestyAI uses 200Bn data points, including aerial imagery, and artificial intelligence to assess the impact of climate change one building at a time. ZestyAI has partnered with leading insurance companies and property owners helping them protect homes, businesses and support thriving communities. ZestyAI was named Top 100 Most Innovative AI Company in the world by CB Insights in 2020, and Gartner Cool Vendor in Insurance by Gartner Research in 2019. For more information visit: https://www.zesty.ai/

About the Insurance Institute for Business & Home Safety (IBHS)

The IBHS mission is to conduct objective, scientific research to identify and promote effective actions that strengthen homes, businesses and communities against natural disasters and other causes of loss. Learn more about IBHS at DisasterSafety.org.

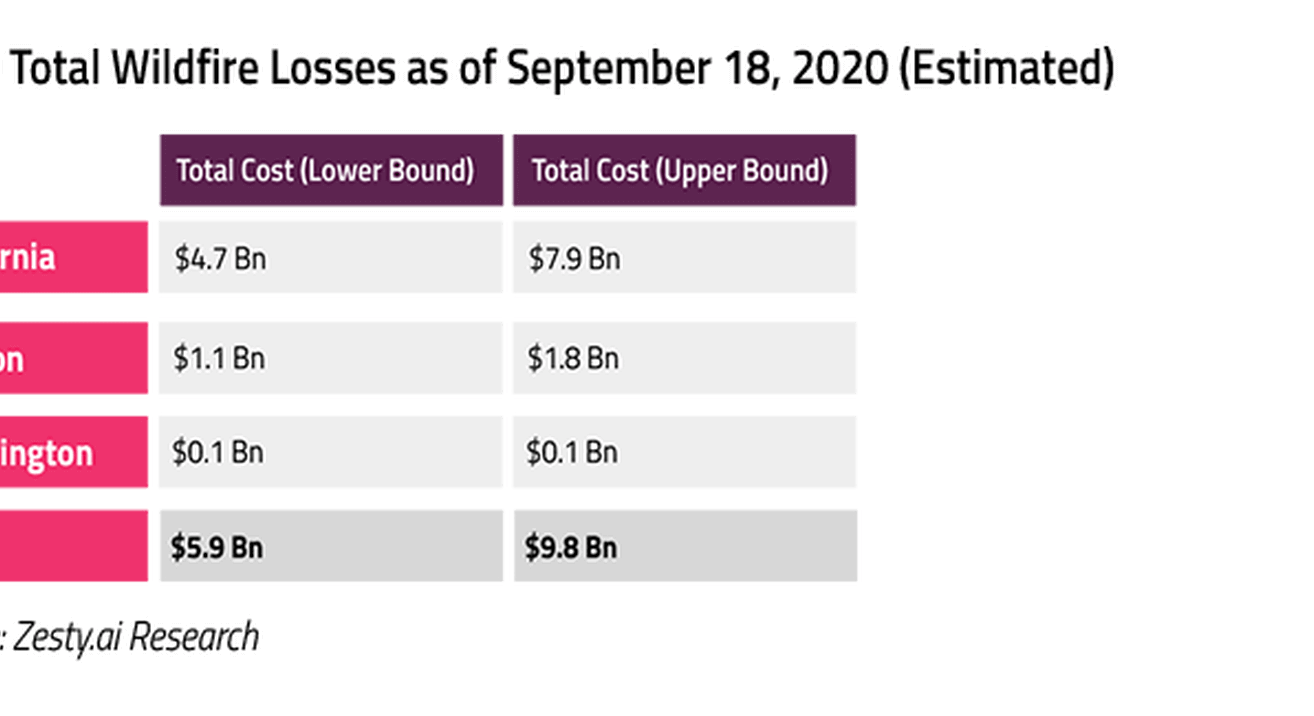

ZestyAI Research: Up to $9.8Bn in Losses Already Caused by Wildfires in 2020

As of September 18th, between $5.9Bn and $9.8Bn in losses have occurred this year alone.

The Zest

ZestyAI has been keeping a close eye on the wildfires burning in the Western United States. Whether by evacuation or smoke, most of our employees have felt the impact firsthand.

Utilizing our vast wildfire data and artificial intelligence resources, we have estimated that as of September 18th, between $5.9Bn and $9.8Bn in losses have occurred this year alone.

What has made 2020 unique?

Two key aspects have made the 2020 Wildfire Season exceptional: the number of acres burned and the timing of the fires.

2018, which previously held the California record for acres burned at 1,975,086 has been eclipsed with months left in the seasons. More than 3.3 million acres have already been charred by wildfire this year in California alone, and more than 5 million in the Western US.

Fire season tends to start in September and peak in November. In August, a large scale lightning event occurred, triggering many of the California wildfires. Oregon, which typically has a shorter wildfire season has also seen early and widespread wildfires.

Analysis Methodology

Using ZestyAI’s comprehensive historical wildfire loss data, up-to-date wildfire perimeter locations for the 2020 season, residential and commercial property information, and fueled by ZestyAI’s AI-driven wildfire damage risk scores, the expected destruction and cost of the 2020 wildfire season so far was calculated for California, Oregon, and Washington.

To estimate the destruction and damages, ZestyAI identified every structure involved in the 2020 wildfire perimeters and their associated wildfire vulnerabilities. Using the historical relationship between the risk profile of the structure, asset value, and economic loss, ZestyAI was able to estimate the full economic loss of those events (including non-insured assets such as uninsured property, and non-insured economic cost). Actual information from CalFire on CZU and LNU incident was used to validate the methodology.

From our extensive historical loss data, a relationship between structural damage expected and the cost of wildfire events was developed based on local property and loss information and expanded to include additional considerations such as smoke damage, displacement costs, and construction.

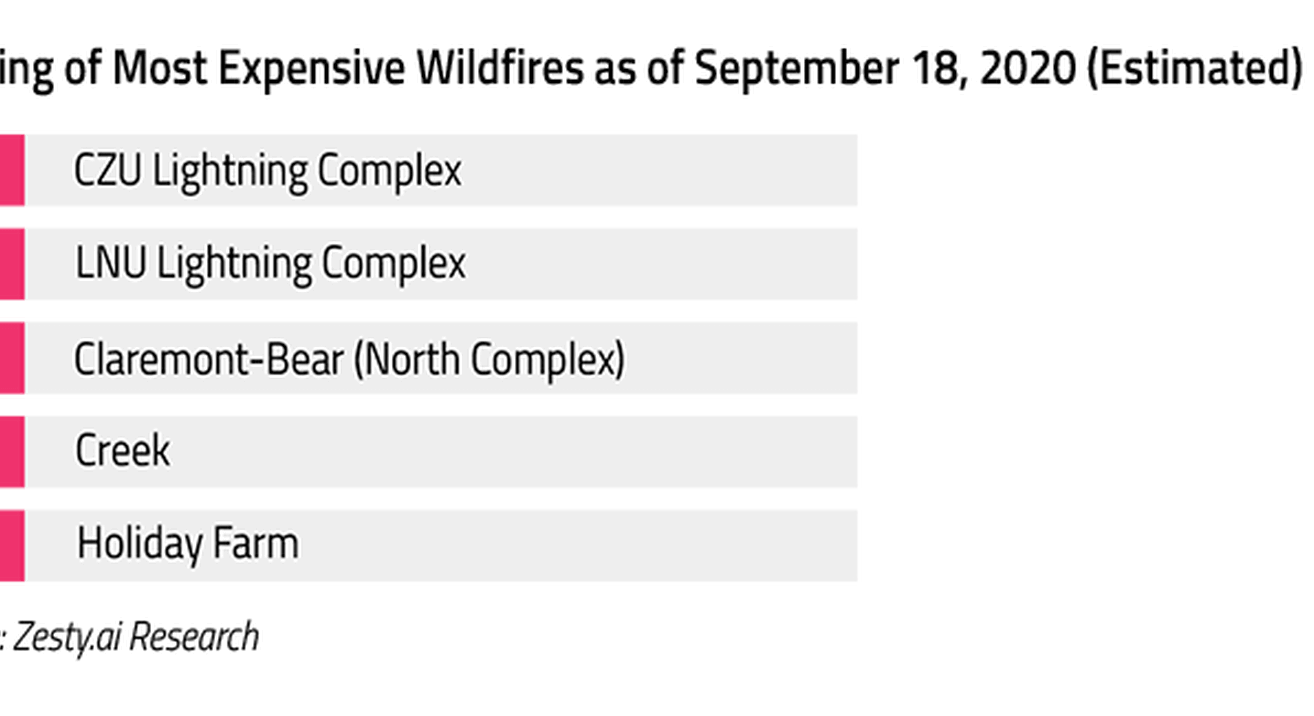

The 5 Most Destructive Fires So Far

Our estimates place the Claremont-Bear (North Complex) at the top of the list of most destructive in terms of number of properties lost. Four of these five wildfires occurred in California with the Alameda Drive fire occurring in Oregon.

The 5 Most Expensive Fires So Far

While the Claremont-Bear (North Complex) fire is estimated to have destroyed the most properties, the CZU Lightning Complex fire is currently estimated to be the most costly at up to $2.6B. That makes it responsible for ~27% of all total economic losses from fires in the 2020 season so far.

Putting Numbers on Destruction

By ZestyAI estimates, between $5.9Bn and $9.8Bn of economic losses have occurred in California, Oregon, and Washington so far this year. California, which also leads in acres burned (5M+) makes up the lion’s share at up to $7.9B.

It’s important to state that the fire season is not yet over. In much of the Western US, it could be just beginning. With a number of fires still active and the potential for more to start, these numbers are almost certain to rise between now and the end of the year.

Looking Forward

Multiple estimates place the 2018 wildfire season at around $15Bn in total losses. While exceptional in terms of total acres burned, the 2020 wildfire season has not yet reached that level of economic loss. Without any doubt, this will be one of the costliest years on record, and with months left in the season, the potential exists for this year to surpass 2018 if it continues at its current pace.

ZestyAI will continue to monitor this fire season. As in years past, new data continues to refine our models and analyses. Insurance professionals and media who would like more information about this analysis or about how artificial intelligence can help insurers protect themselves and their customers from wildfire should contact us.

.png)

Now Streaming: The Hidden Redesign of P&C Insurance

What 2 Million Filings Reveal About 2026 Product Strategy

P&C Insurance Is Being Rewritten - Quietly but Rapidly.

Filings from the last three years show faster shifts in P&C products than at any point in recent history - and those changes are now surfacing at scale.

Endorsements, exclusions, deductibles, and appetite resets are reshaping coverage and competitive positioning across carriers. But the pace isn't uniform. National carriers, regionals, MGAs, and farm bureaus are moving in different directions - and most teams don't have visibility into how quickly competitors are adjusting forms and filings.

This session breaks down the signals that matter for 2026 product strategy.

Drawing on 2M+ carrier filings, Stephanie Kuczynski reveals the real trends reshaping P&C product strategy headed into 2026.

You'll learn what's accelerating, where carriers diverge, and how to translate these shifts into action.

What You Will Gain

- Which changes are accelerating fastest — and where carriers diverge. State-by-state adoption patterns for endorsements, deductibles, and coverage restrictions.

- How strategies differ by carrier size and focus — niche players vs. nationals. The creative, targeted approaches emerging from regionals and MGAs versus the broad strategies deployed by national carriers.

- Where regulators are drawing the line on coverage restrictions. Prepare for closer state-level inspection, due diligence, and shifting expectations across markets.

- How these shifts impact 2026 product strategy and competitive positioning. Why the pace and direction of changes matter — and how to ensure your strategy reflects where the market is heading.

Watch Now

Southern Oak Expands Use of ZestyAI After Nine Months of Proven Impact

Florida-based insurer broadens its use of ZestyAI as property-level intelligence becomes integral to portfolio management

ZestyAI today announced that Southern Oak Insurance Company has expanded its partnership with ZestyAI following nine months of demonstrated impact on portfolio decisions across its Florida homeowners portfolio.

Southern Oak initially adopted ZestyAI in 2025 to gain clearer visibility into property-level risk in one of the most complex and loss-prone insurance markets in the U.S.

Z-PROPERTY applies computer vision and machine learning across aerial imagery, building permits, tax assessment records, and other verified data sources to evaluate properties in 3D—assessing structural condition, exposure, and characteristics that influence claim frequency and severity across perils, including roof complexity, materials, and condition.

Tony Loughman, CEO of Southern Oak Insurance Company, said:

“Within months of deploying ZestyAI, it became clear that property-level intelligence needed to play a larger role in how we evaluate and manage risk. Expanding our partnership allows us to build on that foundation with greater confidence in the data behind our decisions, particularly in a market where roof condition, complexity, and exposure can materially impact outcomes.”

The expanded partnership reflects Southern Oak’s continued focus on proactive risk management in Florida’s volatile insurance environment, where traditional data sources often fail to capture the real condition and vulnerability of individual homes.

“Southern Oak’s decision to expand just nine months in is a strong signal of the value property-level intelligence delivers when it’s put into production,” said Attila Toth, Founder and CEO of ZestyAI.

“With Z-PROPERTY embedded in its risk decisions, Southern Oak sees risk more clearly, acts earlier, and makes more defensible decisions in a highly regulated, high-risk market.”

ZestyAI’s models are built with transparency, validation, and regulatory readiness at the forefront, giving insurers confidence to rely on them in portfolio decisions. The platform is used by leading insurers to improve underwriting accuracy, manage exposure, and reduce loss volatility across weather- and non-weather-driven perils.

Lilypad-Centauri Partners With ZestyAI to Strengthen Coastal Portfolio Using AI-Driven Risk Analytics

Lilypad-Centauri adopts roof and parcel-level insights to sharpen exposure data and strengthen risk decisions

ZestyAI today announced that Lilypad-Centauri is using ZestyAI’s Roof Age and Z-PROPERTY™ solutions to enhance its view of property risk across coastal homeowners and dwelling fire portfolios.

Lilypad-Centauri focuses on delivering stable and reliable coverage to homeowners and property owners in hurricane- and catastrophe-exposed coastal communities. By leveraging ZestyAI’s building attributes and parcel-level characteristics, Lilypad-Centauri gains a clearer view of property risk and how exposure accumulates across its coastal portfolio.

Lilypad-Centauri, through its managing general agency, is deploying two of ZestyAI’s proven solutions to gain a more granular, defensible view of property risk:

- Roof Age delivers verified roof age by cross-validating building permit records with over 20 years of aerial imagery, detecting roof replacement events, and assigning confidence scores across 97% of U.S. properties.

- Z-PROPERTY™ applies AI to high-resolution aerial imagery to assess roof complexity, materials, and condition, while evaluating parcel-level features such as vegetation overhang, yard debris, and secondary structures that influence claim frequency and severity across multiple perils.

“Coastal properties present a unique combination of exposure, from roof condition and construction features to how the parcel is maintained,” said Tony Hare, Chief Operating Officer & Chief Underwriting Officer of Lilypad-Centauri.

“ZestyAI’s roof and parcel-level analytics give us a clearer, property-level view of the homes we insure, helping us reduce uncertainty and better manage portfolio volatility.”

“Lilypad-Centauri is building a more resilient coastal portfolio by replacing exposure unknowns with verifiable property‑level truth,” said Attila Toth, Founder and CEO of ZestyAI.

“Granular, regulator-approved analytics bring confidence to the risk and capital decisions behind reliable customer protection.”

ZestyAI works closely with regulators to ensure transparency, validation, and continuous monitoring of its AI-driven models. Its portfolio of risk models has secured nearly 100 approvals from regulators nationwide, giving insurers confidence they can be deployed immediately with the accuracy and transparency regulators demand.

ZestyAI Provides AI-Driven Risk Analytics for Marsh McLennan Agency

MMA’s Private Client Services division adopts wildfire, roof, and parcel-level insights to drive better outcomes for its high-net-worth clients

ZestyAI, the Risk and Decision Intelligence Platform for the insurance industry, today announced that Marsh McLennan Agency (MMA), a subsidiary of Marsh (NYSE: MRSH), has adopted its risk analytics

By leveraging three cutting-edge solutions from ZestyAI, Z-FIRE™, Roof Age, and Z-PROPERTY™, the MMA Private Client Services team was able to improve wildfire risk evaluation for these homeowners by analyzing detailed property data and loss history and assessing roof age and condition using high-resolution aerial imagery. This strategic deployment enhanced their ability to offer more precise, customized insurance and risk management solutions for their clients’ high-value homes.

“Safeguarding the lifestyles and legacies of our clients requires a forward-looking approach to risk,” said Robert Pritula, Senior Vice President, National Placement and Solutions Leader of MMA’s Private Client Services division.

“We are always looking for new ways to leverage cutting-edge technologies that will allow us to offer clients tailored and effective solutions to mitigate the threats facing their most valuable assets, including their homes.”

“MMA has built its reputation on exceptional client service and proactive risk management,” said Attila Toth, Founder and CEO of ZestyAI.

“With granular risk analytics backed by industry standards and proven accuracy, they are leading the way in how high-value portfolios can be protected with confidence.”

ZestyAI works closely with regulators to ensure transparency, validation, and continuous monitoring of its AI-driven models. Its portfolio of models has secured more than 80 approvals from regulators nationwide, including Z-FIRE™, which has been approved across every wildfire-prone state, giving insurers confidence they can be deployed immediately with the accuracy and transparency regulators demand.

What Winter Storm Fern Reveals about Interior Water Losses and Systemic Risk

ZestyAI Product Insights

Winter Storm Fern has evolved into a historic catastrophe for the U.S. insurance industry. Between January 23-27, 2026, the storm shattered records by placing over 230 million Americans under severe winter alerts, with a death toll of 85 as of February 3rd.

Preliminary industry estimates place insured losses at $6.7 billion, potentially making Fern the third-costliest U.S. winter storm on record, trailing Elliott (2022) and Uri (2021). The crisis is far from over. The National Weather Service warns of a "historic duration" of extreme cold, with temperatures 15 to 25 degrees below average, that continues to hamper mitigation efforts.

For carriers, Fern is a complex, multi-peril challenge. Claims teams are navigating a surge of freeze-related losses, ice-driven structural damage, and widespread business interruptions across 34 states.

To understand the stakes, one needs to look no further than February 2021, when Winter Storm Uri brought Texas to its knees and generated over $11 billion in insured losses from a single state. Fern’s footprint is broader, and its secondary effects are still unfolding.

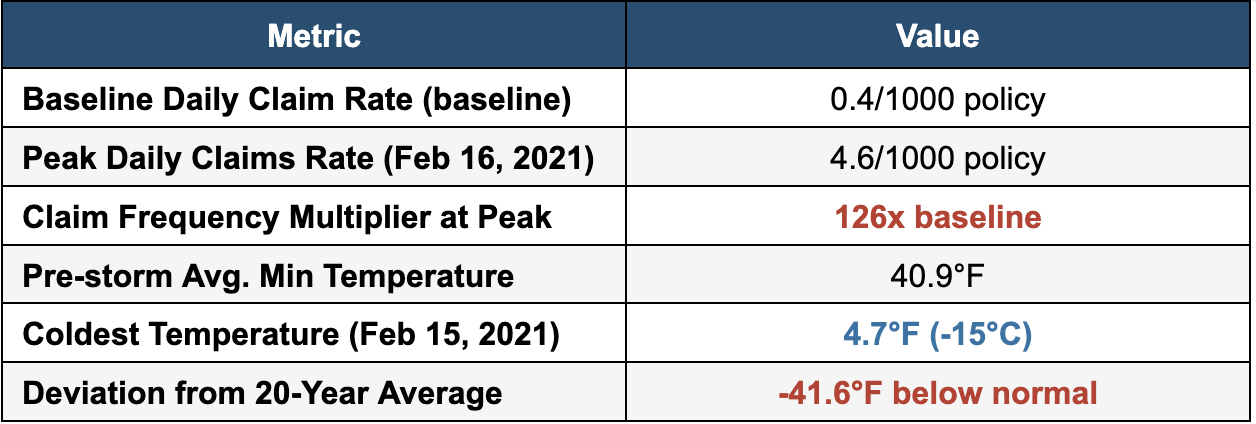

The Cold Hard Numbers from Storm Uri: Why Claims Explode Below 5°F

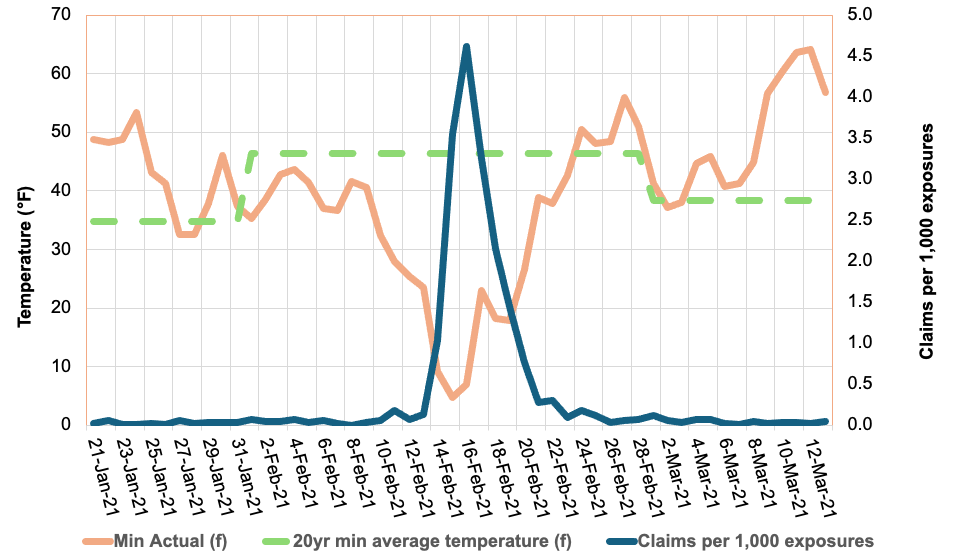

Our analysis of the 2021 Storm Uri reveals a striking relationship between temperature deviation and claim frequency for the non-weather water and freeze perils. Using data from multiple carriers, we tracked daily claim rates against minimum temperatures: before, during, and after the storm window (February 11-20, 2021).

The results show how rapidly falling temperatures can transform a routine winter pattern into a systemic loss event, allowing us to monitor the market’s response in real-time as conditions deteriorated, peaked, and normalized.

The results are dramatic:

Figure 1: Daily claim rates (blue line) surged 126X above the baseline in a temporal spike as temperatures (orange line) plunged below the 20-year average (dashed green line) during Winter Storm Uri.

The chart reveals a clear inverse relationship: as minimum temperatures dropped from the mid-40s°F to below 5°F, daily claim rates didn’t just rise, they increased 126X, from a baseline of 0.04% to 0.46% at the peak. This dramatic surge underscores the significant consequences of extreme cold events on insurance liability.

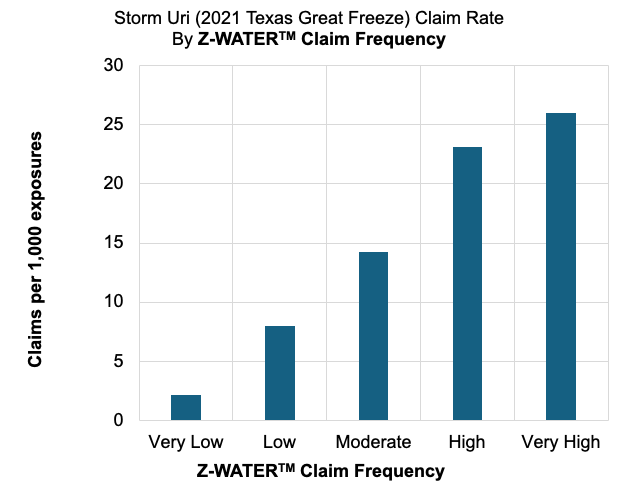

Figure 2: ZestyAI’s Z-WATER™ demonstrated an 11X increase in claim frequency between ‘Very High’ and ‘Very Low’ risk tiers during Winter Storm Uri

We used ZestyAI’s Z-WATER™ to segment the property-specific non-weather water risk across the 10-day storm window. Z-WATER™ is a risk model that accounts for how plumbing design, local climate, and infrastructure reliability interact to drive non-weather water and freeze losses. By capturing real-world dynamics, such as temperature swings that stress pipes and electrical grid failures that amplify claims, the model delivers a scientifically grounded view of property-level risk.

The results were definitive: properties that Z-WATER™ scored as ‘Very High’ risk filed 26 claims per 1,000, compared to just 2.2 claims per 1,000 for those scored as ‘Very Low’, an 11X increase in claim frequency.

This accurate segmentation reveals a clear path to managing volatility. Z-WATER™ provides a deep understanding of a home’s resilience across the full spectrum of loss mechanisms, from everyday plumbing failures to expensive outlier events like Storms Uri and Fern. By enabling precise intra-territory risk splitting, the model allows carriers to price and underwrite more reliably, ensuring premiums reflect the true risk profile while protecting the portfolio against systemic losses.

The January 2026 Storm: History Rhyming?

While we can already see the immediate impact of Winter Storm Fern, the primary difference between Fern and Winter Storm Uri is the duration of the freezing event itself, rather than any changes in how quickly policyholders are filing their claims.

As shown in Figure 1, NWW claims rise rapidly as temperatures fall and taper off quickly once conditions normalize. The risk in prolonged cold events lies in how long properties stay below the Plumbing Design Temperature; the longer the freeze, the greater the likelihood of systemic plumbing failure.

During Winter Storm Uri, extended sub-freezing conditions significantly increased the number of days in which vulnerable properties were exposed to frozen pipe failures, driving aggregate losses to historic levels. Fern is now exhibiting a similar duration profile, with sub-freezing conditions persisting for up to 10 consecutive days across parts of the Northeast. The National Weather Service has warned this “could be the longest duration of cold in several decades,” raising the likelihood of elevated losses even if individual claims remain tightly clustered in time.

For carriers, the warning signs are already flashing:

- The Power Failure Multiplier: During the storm's peak, over 1 million customers lost power. In the South, where homes lack the heavy thermal insulation of northern properties, a power outage is the primary driver of catastrophic pipe bursts. Without active heating, a property can reach the "burst threshold" within hours.

- The $30,000 Claim Severity Benchmark: Recent State Farm data underscores the high stakes of these events. Winter water damage claims totaled over $628 million, with the average claim payment now exceeding $30,000. For carriers, this high per-claim severity means even a moderate frequency surge can quickly erode Q1 margins.

- Regional Fragility in the South: While the initial assessments are still surfacing, early industry estimates for privately insured losses from Winter Storm Fern puts the damage at $4 billion to $7 billion. With Texas and Tennessee identified as the hardest-hit states, carriers are facing a "Uri-style" scenario in which infrastructure wasn't designed for a 10-day deep freeze.

From Reactive to Predictive: Solving the $6.7 Billion Freeze Risk Equation

The 2021 Texas freeze taught us that traditional approaches to freeze risk are highly insufficient. Many properties that experienced burst pipes were in areas that rarely see extended freezing temperatures, meaning they lacked adequate winterization.

This is where predictive analytics becomes essential. By modelling the interaction between property-level vulnerabilities and local temperature thresholds, carriers can better identify which properties are most vulnerable to freeze events before the damage actually occurs.

Key Risk Drivers Identified in Our Latest Analysis:

- The Design Mismatch: The greatest risk isn't just the cold; it's the sudden change in temperature. Properties in states like Texas or Tennessee face a higher risk because they are built to release heat, not trap it. They lack the heavy insulation and deep-buried pipes needed to survive a 10-day freeze.

- The Power Grid Vulnerability: Our analysis shows that areas prone to power outages face a compounded risk. In the South, a home’s primary defense is its heating system so when the power fails and the heater stops, the "burst threshold" can be reached in just a few hours.

- Building Vulnerabilities: Our analysis shows that older homes and properties with plumbing routed through exterior walls are disproportionately represented among $30,000 non-weather water losses.

The Bottom Line for Carriers

The 2021 Texas freeze was a pivotal moment for the industry, generating more than 500,000 claims and $11.2 billion in insured losses in a single state. Today, Winter Storm Fern represents an even broader systemic threat, with weather alerts impacting 230 million people across more than 30 states.

While the final tally for Fern is still developing, the data is already clear: temperature shocks drive claims at exponential rates. With early industry assessments estimating privately insured losses between $4 billion and $7 billion, it is evident that the prolonged duration and geographic anomaly of extreme weather events are the primary drivers of this volatility.

For carriers looking to protect their Q1 margins, predictive analytics are no longer a luxury; they are a requirement. By analyzing property-level characteristics, regional vulnerabilities, and historical temperature deviations, you can move from reactive claims handling to proactive risk management.

The question isn't whether another major freeze will occur, but whether your portfolio is prepared for the next 126-fold surge.

Learn More About Z-WATER

ZestyAI’s Z-WATER™ provides the industry’s most granular view of interior water risk, helping carriers accurately and reliably assess properties in areas prone to temperature shock events. By analyzing detailed property-level characteristics alongside historical weather patterns and regional risk factors, our advanced models predict the likelihood of Non-Weather Water (NWW) and freeze claims as well as their associated severity. This deeper level of analysis empowers carriers to make smarter pricing decisions before the next major storm hits.

Methodology: Analysis based on aggregated claims from multiple Texas carriers during Winter Storm Uri (February 2021). Temperature data reflects mean daily minimums across the exposure footprint, weighted by ZIP Code to account for geographic density. The claim/exposure ratio was calculated by dividing daily claims by the average policy-day exposure.

-----------------------------------------------------------------

1CNN Weather, "More than 230 million people under alerts for potential ice, heavy snow and extreme cold," January 2026. [link]

2Fox News, "Noem coordinates with Mississippi officials as state recovers from deadly winter storm," January 2026. [link]

3Insurance Innovation Reporter, “KCC Estimates $6.7 Billion in Insured Losses from Winter Storm Fern,“ February 2026 [link]

4Texas Department of Insurance, "Insured Losses Resulting from the February 2021 Texas Winter Weather Event," March 2022. [link]

5Fox Business, “More than 1 million Americans lose power as monster winter storm sweeps across the US,” January 2025 [link]

6Carrier Management, “Frozen Pipes Lead to $628M in Losses for State Farm,” January, 2026 [link]

7 Barrons, “Winter Storm Fern Packed a Wallop. Now the Cost Estimates Are Rolling In.,“ February 2026 [link]

Logic Underwriters Adopts ZestyAI to Strengthen Texas Property Underwriting with AI-Powered Hail and Wind Models

Storm and property insights help inform risk-aligned coverage decisions

ZestyAI today announced that Logic Underwriters has adopted ZestyAI’s Z-PROPERTY™, Z-HAIL™, and Z-WIND™ solutions to improve underwriting and rating precision across its personal and commercial property portfolio in Texas.

Texas is the most expensive severe convective storm market in the United States, with hail and damaging wind driving billions of dollars in insured losses every year.

"Texas is one of the most challenging storm markets in the U.S., and we need tools that match that reality," said Bill Motz, Director of Operations, Logic Underwriters.

"ZestyAI's detailed property insights and dedicated hail and wind models will help us continue to provide exemplary service to our clients—from more accurate risk assessments to better loss prevention guidance in increasingly volatile weather conditions."

ZestyAI’s property-specific hail and wind models predict the likelihood and severity of storm-driven claims by analyzing how local climatology interacts with detailed property characteristics—helping underwriters to distinguish meaningful differences in risk within the same rating territory. Each model is trained on validated claims data, offering transparent explanations of the key factors driving risk.

Z-PROPERTY applies AI to high-resolution aerial imagery and multi-source data to assess roof condition, structural complexity, and parcel-level features such as vegetation overhang, yard debris, and secondary structures—factors that directly influence claim frequency and severity across multiple perils.

“Logic Underwriters is exactly the kind of forward-looking partner that is redefining underwriting in high-exposure states,” said Attila Toth, Founder and CEO of ZestyAI.

"This collaboration shows how property-level intelligence can support underwriting excellence and disciplined decision-making while helping policyholders better understand and protect their properties. When insurers can identify specific risk factors like roof condition or vegetation overhang, they can provide actionable guidance that helps clients reduce their exposure and minimize losses."

ZestyAI’s severe convective storm models are approved in 30 states, spanning the nation’s highest-exposure hail and wind markets, and used by leading insurers across the country.

See How Insights Turn Into Decisions

ZestyAI transforms data into action. Get a demo to see how the same AI powering our reports helps carriers make faster, smarter, regulator-ready decisions.