Resources

Augusta Mutual Adopts ZestyAI’s Risk Analytics to Strengthen Underwriting Precision

AI-powered property insights support greater rating precision, lower inspection costs, and smarter underwriting decisions across Virginia

ZestyAI today announced that Augusta Mutual has selected ZestyAI’s Roof Age and Z-PROPERTY™ to enhance underwriting and rating accuracy, target inspections more effectively, and support sustainable growth across Virginia.

Based in Staunton, Virginia, Augusta Mutual is a single-state carrier serving Virginia since 1870 with a longstanding reputation for personalized service and local expertise. By upgrading from traditional imagery and inspection approaches to ZestyAI’s computer vision and machine learning technology, the insurer gains broader, more consistent property coverage and a more comprehensive, AI-driven view of property risk—unlocking property-level insights such as verified roof age, roof condition, vegetation overhang, and debris accumulation that directly influence claim frequency and severity.

“ZestyAI’s solutions bring a new level of precision to our underwriting process,” said Gretchen H. Collins, Vice President of Underwriting at Augusta Mutual.

“We moved from legacy property risk tools to gain broader, verified property coverage, helping us make faster, more consistent, and more confident decisions for our policyholders across Virginia.”

ZestyAI’s Roof Age delivers verified roof age by cross-validating building permit records with over 20 years of aerial imagery, detecting roof replacement events and assigning confidence scores across 97% of U.S. properties. Z-PROPERTY™ further enhances this insight by assessing roof complexity, materials, and condition, along with other parcel-level attributes that influence loss potential.

ZestyAI works closely with regulators to ensure transparency, validation, and continuous monitoring of its AI-driven models. Its portfolio of risk models has secured nearly 100 approvals from regulators nationwide, giving insurers confidence they can be deployed immediately with the accuracy and transparency regulators demand.

.webp)

P&C Predictions for 2026

By Attila Toth, Founder & CEO of ZestyAI

The U.S. P&C industry enters 2026 with stronger balance sheets, renewed underwriting profitability, and a sense that the hardest part of the cycle may be behind it. But beneath the surface, the risk environment is moving in the opposite direction. Climate-driven loss volatility, localized catastrophe patterns, and structural property vulnerabilities are accelerating — even as markets begin to soften.

The result is a widening gap between carriers chasing growth and those wiring discipline deeper into how risk is selected, priced, and managed. Here are three dynamics that will define P&C performance in 2026.

1 — A Softer Market Meets a Hard Climate Reality

The industry enters 2026 from a position of renewed financial strength: the last couple of years produced the best U.S. P&C underwriting results in more than a decade, with combined ratios improving into the mid‑90s and a clear swing back to underwriting profit.

Capital has rebuilt, competition is intensifying in many property segments, and some markets are now seeing flat or slightly negative renewals, encouraging carriers to cautiously re‑enter territories that were pulled back during the hard market.

The risk environment, however, has not softened; insured catastrophe losses have exceeded USD 100 billion for multiple consecutive years, and recent nat‑cat studies now describe annual insured losses approaching USD 150 billion as the emerging “new normal,” driven disproportionately by severe convective storms, wildfire, localized flooding, and non‑weather water losses rather than a single headline hurricane season.

In 2026, carriers will not move in lockstep. Some will quietly relax property underwriting and broaden appetite to chase top‑line volume in what feels like a more forgiving market, even as U.S. SCS losses alone have entered a period where annual insured losses now consistently exceed USD 40 billion, while others will double down on discipline by wiring property‑level climate and vulnerability metrics into day‑to‑day decisions.

Early in the year, the visible story may favor the volume‑chasers as premium growth accelerates, but by late 2026 the more revealing story will be in loss ratios, with hail‑, SCS‑, wildfire‑adjacent, and water‑heavy portfolios that were loosely underwritten posting the most uncomfortable deterioration.

2 — Hyperlocal Exposure Management Becomes a Core Profit Lever (and Reinsurers Will Expect It)

Even with some rate relief on better risks, carriers face a structural problem going into 2026: loss volatility is increasingly driven by frequent, highly local events and structural property issues rather than a single major catastrophe.

A two‑block hail cluster, an ember‑exposed hillside parcel at the wildland–urban interface, or aging roofs can generate thousands of mid‑sized claims that erode margin even when headline cat activity looks “average.”

When property‑level secondary modifiers are missing or stale, catastrophe models and capital providers default to conservative assumptions, inflating modeled losses, uncertainty loads, and reinsurance costs; reinsurers are responding by demanding clearer visibility into roofs, vegetation, defensible space, elevation, and mitigation before offering the most favorable terms.

In this environment, hyperlocal exposure management is becoming a core profit lever rather than a niche analytics exercise. Leading carriers are using verified parcel‑level attributes to identify frequency‑prone parcels inside ZIP codes that look stable in aggregate, to counter overly conservative model assumptions with auditable evidence, and to walk into reinsurance renewals with property‑level documentation rather than broad averages.

They are steering appetite, pricing, inspections, and mitigation strategies on a near‑real‑time basis instead of waiting for annual rate cycles, effectively trading unmanaged volatility for intentional, data‑driven control. The net result is that 2026 will reward carriers that can prove property‑level truth to reinsurers, regulators, and their own underwriting teams, replacing assumptions with evidence and episodic adjustments with continuous portfolio management.

3 — Agentic AI Becomes Insurance’s Next Operating System

2026 is shaping up as the year agentic AI shifts from experimental to essential in P&C, as carriers discover that the binding constraint is no longer access to data but the speed, consistency, and defensibility of decisions across underwriting, filings, compliance, and product change. Risk conditions are moving materially faster than traditional annual guideline refreshes can accommodate, supervisors and rating agencies are sharpening expectations around explainability and consistency, and decades of underwriting and regulatory expertise are retiring faster than they can be replaced.

Across the market, early adopters are already using agent‑like systems to flag likely regulatory objections before filings go in, compress filing and approval timelines from months to weeks, and synthesize competitive and regulatory intelligence with strong safeguards and human‑in‑the‑loop review. These systems are also starting to refresh underwriting and pricing playbooks using live property‑risk signals instead of static territorial assumptions, closing the loop between climate data, filings, and front‑line decisions. For many carriers, 2026 will be remembered as the year AI stopped being primarily predictive and became operational infrastructure — software that can understand intent, reason through complex rules, coordinate multi‑step workflows, and take auditable action alongside human teams.

How Leading Carriers Are Responding

The most forward-positioned carriers entering 2026 are already using parcel-level intelligence to refine appetite, pricing, inspections, and mitigation in high-hazard and water-exposed regions, treating hyperlocal data as a core underwriting input rather than an afterthought.

They are refreshing eligibility criteria and underwriting guidelines based on property-specific hazard, vulnerability, and mitigation features, and preparing regulator-ready and reinsurer-ready documentation on defensible space, roof condition, and other secondary modifiers.

They are steering portfolios continuously, adjusting aggregates, concentrations, and mitigation incentives throughout the year instead of relying solely on renewal season to reset course. Together, these behaviors signal a broader shift away from episodic, once-a-year recalibration toward continuous, property-level risk management supported by AI-enabled operating systems.

The Insurance Shift Reshaping the 2026 Property Market

Insurance availability has become a constraint on the housing market.

That’s the central argument Ross Martin, VP of Risk Analytics at ZestyAI, makes in ATTOM’s newly released Q4 2025 Housing News Report—and it’s one that will increasingly shape affordability, underwriting, and buyer behavior heading into 2026.

Housing discussions still focus on mortgage rates and inventory. But in many markets—especially catastrophe-exposed ones—insurance is becoming a gate in the transaction. If a property can’t get insured, or coverage is uncertain, deals stall. And when insurance costs spike unexpectedly, affordability breaks even when the mortgage penciled out.

Ross’s point isn’t simply that insurance is getting more expensive. It’s that availability and predictability now matter as much as price—and the market would function better with clearer, property-level risk signals.

Today, homes in similar locations can carry meaningfully different risk based on factors like roof condition and materials, defensible space and vegetation management, yard and debris conditions, and documented improvements captured in permits or listing data. When those distinctions aren’t consistently reflected in underwriting or pricing, mitigation efforts go unrewarded—and higher-risk properties don’t get early, property-specific signals to improve.

For insurers, this lack of granularity creates real portfolio risk. When individual properties aren’t differentiated clearly enough, volatility increases, adverse selection becomes harder to avoid, and long-term participation in catastrophe-exposed markets becomes less sustainable. Property-level, mitigation-aware models help address this by improving segmentation and enabling insurers to stay in market with more confidence.

Recent advances in property-specific data and modeling now make this differentiation possible at scale. Insurers can assess dozens of attributes—including roof age and materials, defensible space, vegetation conditions, building permits, occupancy type, and hazard-specific science—to build a clearer view of a structure’s vulnerability. Just as importantly, these models can recognize mitigation actions—like roof replacements, defensible space creation, and debris removal—and incorporate them more consistently into underwriting and pricing.

When mitigation is visible and rewarded:

- Homeowners and investors gain more control over premiums

- Insurers can maintain more stable portfolios, even in high-risk regions

- Housing markets get clearer signals—making insurance availability and long-term cost less of a guessing game for buyers and lenders

Regulators are paying attention as well. In several states, regulators are examining how property-level data, mitigation, and modern risk modeling approaches can be incorporated more consistently into rate structures, with transparency as a common objective.

The takeaway is straightforward: insurance is shifting from a background cost to an active constraint—and clearer, property-level risk signals are key to easing that constraint. As 2026 approaches, the ability to differentiate risk at the individual property level will play a growing role in restoring predictability, supporting availability, and shaping housing market outcomes.

Read the full article, “The Insurance Shift Reshaping the 2026 Property Market,” in ATTOM’s Q4 2025 Housing News Report.

Insurance Filings: The Overlooked Dataset That Drives Competitive Advantage

Insurance carriers submit 500,000+ regulatory filings annually—but most can't analyze them. Learn why Agentic AI is the key to unlocking competitive intelligence hidden in plain sight.

By Abdul Mohammed, Director of Product Marketing, ZestyAI

Every year, carriers and filers submit hundreds of thousands of rate, rule, and form transactions to state insurance departments (DOIs), many through SERFF. In 2023 alone, SERFF processed 517,571 transactions (NAIC SERFF, reported 2025). These filings are the DNA of the insurance market: the definitive record of how competitors set rates, where they plan to expand, and where they get approval for new ideas or pull back.

Even though much of this information is publicly available in many jurisdictions, with different rules for access and confidentiality, most carriers still miss out on the competitive signals hiding in plain sight.

Key takeaways

- Regulatory filings are a strategic dataset, not just compliance paperwork. They reveal competitor intent and market shifts.

- “Public” does not mean “easy to analyze.” Filings are often massive, cross-referenced, and inconsistently structured, making manual review at scale impossible.

- The winning approach is a filing intelligence stack. Success requires filing data tracked across amendments and effective dates, structured parsing, deterministic calculation, and precise citations.

How Filings Got So Complicated

From 1945 to The Modern Filing Ecosystem

The story begins with the McCarran-Ferguson Act of 1945, which gave states the power to regulate insurance rather than the federal government. As a result, requirements differ by state, making rates, rules, and forms complicated across jurisdictions.

In 1998, the National Association of Insurance Commissioners (NAIC) introduced SERFF (System for Electronic Rate and Form Filings), developed in collaboration with regulators and industry to digitize rate and form submissions. While it successfully moved filings online, the underlying complexity of the content remained.

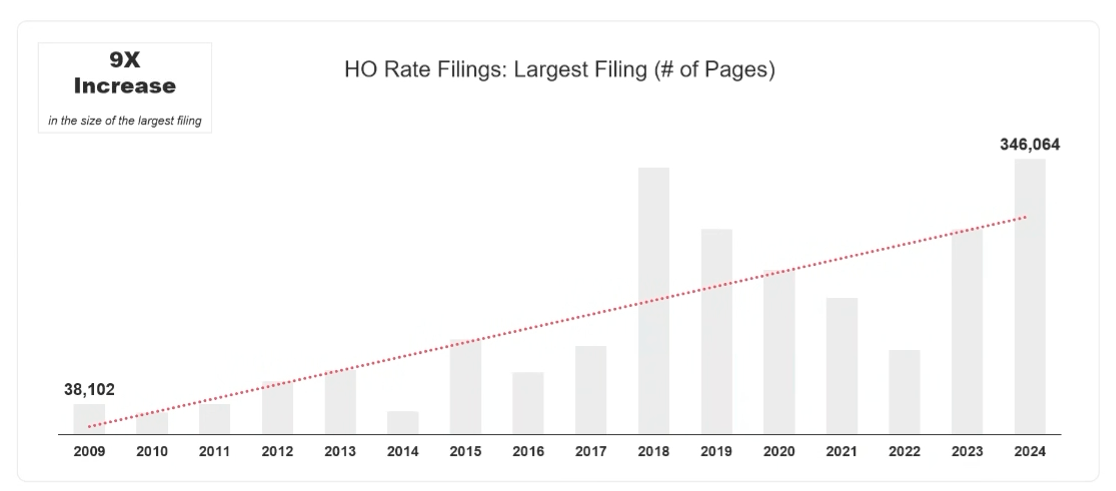

Since then, the volume and complexity of filings have exploded. Our analysis of SERFF filing packages shows that the largest homeowners’ rate filing now exceeds 300,000 pages, including attachments, exhibits, and correspondence. In our data, the biggest package grew from 38,102 pages in 2009 to 346,064 pages in 2024.

Page counts reflect the total number of PDF pages across all documents attached to the filing package, including exhibits, attachments, and objection/response correspondence.

Why Public Filings Remain Inaccessible for Analysis

A public filing is not always easy to access or understand. Carriers know that regulators, consumers, and competitors will review their filings, so the resulting documents are often dense, cross-referenced, and hard to piece together. If you have ever tried to reverse engineer a competitor rate change, you have probably faced these challenges:

The Trade Secret Exception

Some carriers request confidential treatment for specific elements of a filing that may qualify as trade secrets under state rules, such as granular territorial data or specific model inputs. When those sections are redacted or withheld, you lose visibility into important details even though the overall filing is public, and the level of protection varies by jurisdiction.

"When a Product Filing contains Trade Secret information, the Product Filer may identify those portions of the Product Filing, including correspondence with the Compact Office, that contain Trade Secret and seek to protect their disclosure."

Interstate Insurance Product Regulation Commission, FIN 2024-1

The Reference Maze

Sometimes, instead of putting all rate information in one document, a filing will reference several other filings across multiple years. To fully understand the change, an analyst has to track down and reconcile multiple historical filings, creating a confusing trail of "breadcrumbs" that is almost impossible to follow manually.

The PDF Image Trap

Many carriers submit rate tables as scanned images in PDFs instead of machine-readable text. While human eyes can read these tables, most data tools and basic OCR software treat them as pictures, so the information cannot be easily searched, filtered, or analyzed at scale.

The Objection and Response Trail

Often, the most valuable intelligence isn't in the initial filing, but in the "Objection and Response" exchanges between the carrier and the state regulator. These discussions can reveal rationale, supporting evidence, and the boundaries regulators will accept. However, this material is often spread across multiple attachments and correspondence, making it easy to miss critical insights without a structured way to collect and review them.

Non-Standard Nomenclature

There is no universal dictionary for insurance variables. One carrier might call the roof age factor “rf_yr_mod”, while another uses “const_age_rel”. Without a way to normalize these labels, mapping equivalent factors across carriers becomes manual work, making benchmarking slow, error-prone, and difficult to repeat.

Why General Purpose LLMs Often Struggle Here

We are in the age of Generative AI, so the natural question is: "Why not just upload these PDFs into a tool like ChatGPT or Gemini and ask questions?"

You can upload filing PDFs to ChatGPT or Gemini, and you may get a helpful summary. But insurance filing work is not “writing assistance.” It is a precision workflow in which small mistakes lead to incorrect conclusions. General-purpose LLMs are built to generate plausible text from the input you give them, not to reliably preserve filing structure, track versions, run exact calculations, and produce audit-ready citations.

The following are the top reasons why general LLMs often struggle in the inusrance domain:

1. The Math Problem

Insurance filings require exact math and exact linkage across tables, factors, relativities, and formulas. LLMs are probabilistic; they predict likely answers rather than performing exact calculations. If you ask an LLM to calculate a 3.5% rate increase over three years using a specific table, it may give a confident answer that is still wrong. In insurance, even a 0.01% mistake can mean millions in lost premium. As actuarial researchers noted in a 2024 paper from Cambridge University Press, “while LLMs can explain concepts, they often provide inaccurate or incorrect mathematical facts, sometimes in subtle ways.”

2. Structure Blindness

LLMs are mostly trained on regular text, such as books and articles. They are not skilled at understanding tables, following footnotes, or applying formulas consistently across multi-part exhibits, especially when documents are scanned or formatted inconsistently. A standard LLM treats a table as plain text and often fails to understand how the cells are logically and mathematically connected.

3. Context Window Overload

State filings are often longer than what standard LLMs can handle. If you give a model a 2,000-page document, it may lose track of what appeared earlier in the filing and still try to answer questions as if it remembered everything. This can cause the AI to make up numbers (hallucinate) to fill in missing information.

What a Modern Filing Intelligence Approach Looks Like

The industry does not need a better chatbot. It requires a filing intelligence stack that combines structured data, deterministic computation, and auditable reasoning.

Below are the key steps in building this intelligence stack:

Build a clean, versioned filing archive

Ingest filings continuously and preserve them with consistent metadata such as state, carrier, line, status, effective date, and relationships to related submissions. This creates a single, reliable system of record for all filing history.

Parse filings into insurance native components

Break filings into rates, rules, forms, exhibits, objections, and responses. Store rating tables, factors, and hierarchies as structured data instead of plain text, so they can be queried and reused.

Pair language with deterministic calculation

Use deterministic engines for calculations and rate reconstruction, then use language models to explain the results, clarify their meaning, and support structured analysis. The math engine produces the numbers; the LLM explains what they mean.

Make everything traceable

Every conclusion should link back to the exact filing section it came from. This traceability is what turns AI output into something regulators, actuaries, and executives can trust and defend.

The Future Belongs to the Agile

The number of filings and their sizes keep growing. As climate risk reshapes markets, rate reviews and underwriting changes will happen more often. The carriers who succeed will be those who treat regulatory filings as a source of strategic insight rather than a compliance burden.

Those who don’t will pay the price. Without visibility into how competitors are changing rates, rules, and eligibility in near-real time, carriers slip out of sync with the market, underwriting yesterday’s risk at today’s loss costs. That gap is where adverse selection takes hold.

Having access to filings is not enough to gain an edge. The real advantage comes from understanding them quickly and accurately, in a way that can be repeated across teams and product lines. To do this well, you need systems built for the job, not just a general-purpose model. This is where a purpose-built filing intelligence stack changes what is possible.

TruStage Partners with ZestyAI for Commercial Property Analytics Solution

TruStage implements ZestyAI’s suite of climate risk solutions for underwriting insights and to help respond to wildfire regulations in California

ZestyAI today announced an agreement with TruStage. This partnership will leverage ZestyAI’s suite of advanced property analytics solutions for valuable insights during commercial property underwriting.

TruStage will utilize three of ZestyAI's innovative property risk analytics models: Z-HAIL™, Z-FIRE™, and Z-PROPERTY™. Additionally, TruStage will use ZestyAI's Wildfire Mitigation Pre-Fill solution in response to new wildfire mitigation regulations set forth by the California Department of Insurance (CDI) with scalable, high-accuracy wildfire mitigation data without the need for expensive on-site inspections.

“Global insured catastrophe claims are expected to top 100 billion dollars again this year, driven increasingly by secondary perils like hail and wildfire,” said Attila Toth, Founder and CEO of ZestyAI.

“By using AI‑driven, property‑specific intelligence instead of coarse territory‑level averages, TruStage can price risk more precisely, respond to California’s new wildfire mitigation requirements, and better protect its commercial policyholders.”

Z-HAIL is an AI-powered climate risk model that predicts the frequency and severity of hail claims for every property in the US. Z-HAIL examines the interaction of climatology, geography, and the unique characteristics of every structure and roof, including accumulated damage. This information can be used in both underwriting and rating at the time of quote. Using insights into a roof’s susceptibility to severe convective storms and the potential severity of those claims, insurers can accurately segment properties by risk level.

In addition to Z-HAIL, TruStage will use ZestyAI’s Z-FIRE product, an AI-powered, predictive wildfire risk model built on decades of real insurer loss data, and ZestyAI’s Z-PROPERTY platform, which uses computer vision and machine learning to extract insights from aerial and satellite imagery, among other unique data sources, for over 150 million residential and commercial properties.

By leveraging multiple products on the ZestyAI Climate and Property Risk platform, TruStage is empowered to make informed and transparent risk decisions and deliver best-in-class services to its valued customers.

ZestyAI’s Z-WATER™ Greenlit in Five States as Non-Weather Water Losses Intensify

Regulators Review and Accept AI Model Addressing $13B in Annual Non-Weather Water Losses

ZestyAI, the Risk and Decision Intelligence Platform for the insurance industry, today announced that its non-weather water risk model, Z-WATER™, has been reviewed and accepted for use in underwriting and rating in Illinois, Indiana, Iowa, Louisiana, and Wisconsin.

Insurers in these states will now be able to set property-specific rates, align coverage with home-level vulnerabilities, and target inspections and mitigation strategies—including smart water sensors—to reduce cross-subsidization and improve portfolio performance.

Non-weather water has become a major pressure point for carriers, with losses now exceeding $13 billion annually and ranking as the third-costliest peril in homeowners insurance.

Routine failures like burst pipes and hidden leaks are now producing catastrophe-scale losses that surpass hurricanes in severity. Yet the peril has been difficult to model using traditional rating tools, which rely on territory-level or age-based proxies that overlook the property-specific factors driving interior water losses.

Using verified insurer loss data, Z-WATER applies computer vision to aerial imagery and incorporates property-level data, permitting history, localized climatology, and infrastructure context to capture the property-specific drivers of interior water losses. By modeling how these variables interact, Z-WATER predicts both the frequency and severity of non-weather water claims with up to 18× greater accuracy than traditional models.

Bryan Rehor, Director of Regulatory Strategy at ZestyAI, said:

“Non-weather water losses place real pressure on carriers’ books, but they’re also highly preventable when you understand where the risks actually lie.

Z-WATER helps insurers pinpoint those vulnerabilities at the property level and price them appropriately, while meeting regulators’ expectations for clarity and fairness.”

These approvals add to ZestyAI’s broader regulatory momentum. Across five perils—including wildfire, hail, wind, storm, and now non-weather water—ZestyAI has secured more than 80 approvals nationwide. Z-PROPERTY™, the company’s property and roof analytics solution, has also earned broad state-level approval, giving insurers and reinsurers trusted parcel-level insights with the same regulatory-grade transparency.

Ready to see how ZestyAI works on your book of business?

Tell us a little about your needs. We'll show you how we reduce losses and help you price with precision.