Reports & Research

Explore proprietary research packed with data, insights, and real-world findings to help carriers make smarter decisions.

Case Study: Adapting to Escalating Severe Convective Storm Risk

Insights from a 5-year retrospective on ZestyAI’s models in action

The Rising Threat of Severe Convective Storms

The past few decades have seen a dramatic rise in the frequency and intensity of severe convective storms, resulting in significant financial repercussions for the insurance industry. In the last year alone, insured losses from severe convective storms reached an astounding $60 billion, marking an average annual growth rate of over 11% over the past twenty years. This alarming trend means a new approach is needed to manage and mitigate the escalating risks associated with severe weather events.

In the last year alone, insured losses from severe convective storms reached an astounding $60B, marking an average annual growth rate of over 11% over the past twenty years.

The traditional methods of risk assessment and management are no longer sufficient to cope with the increasing unpredictability and severity of these weather events. As the risk evolves, so must the solutions. Changing risks call for innovative solutions that leverage advanced technology and data analytics to enhance the accuracy and effectiveness of risk modeling.

A New Approach

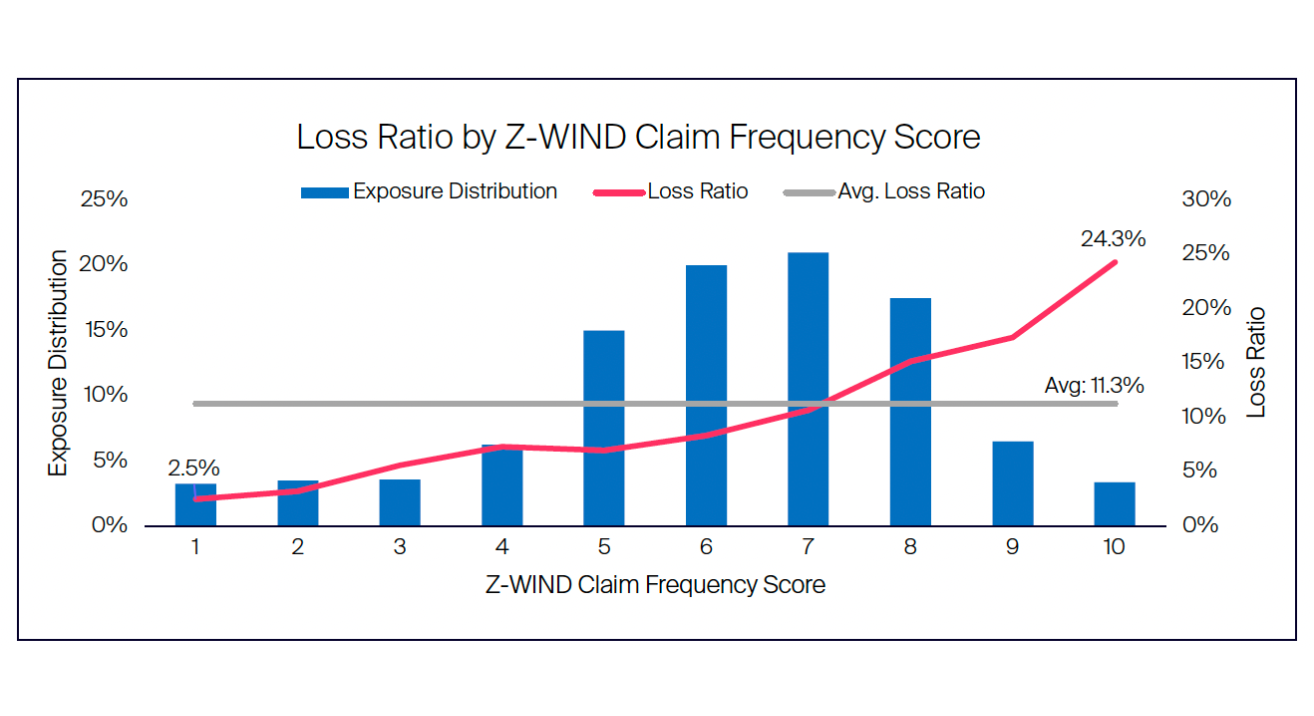

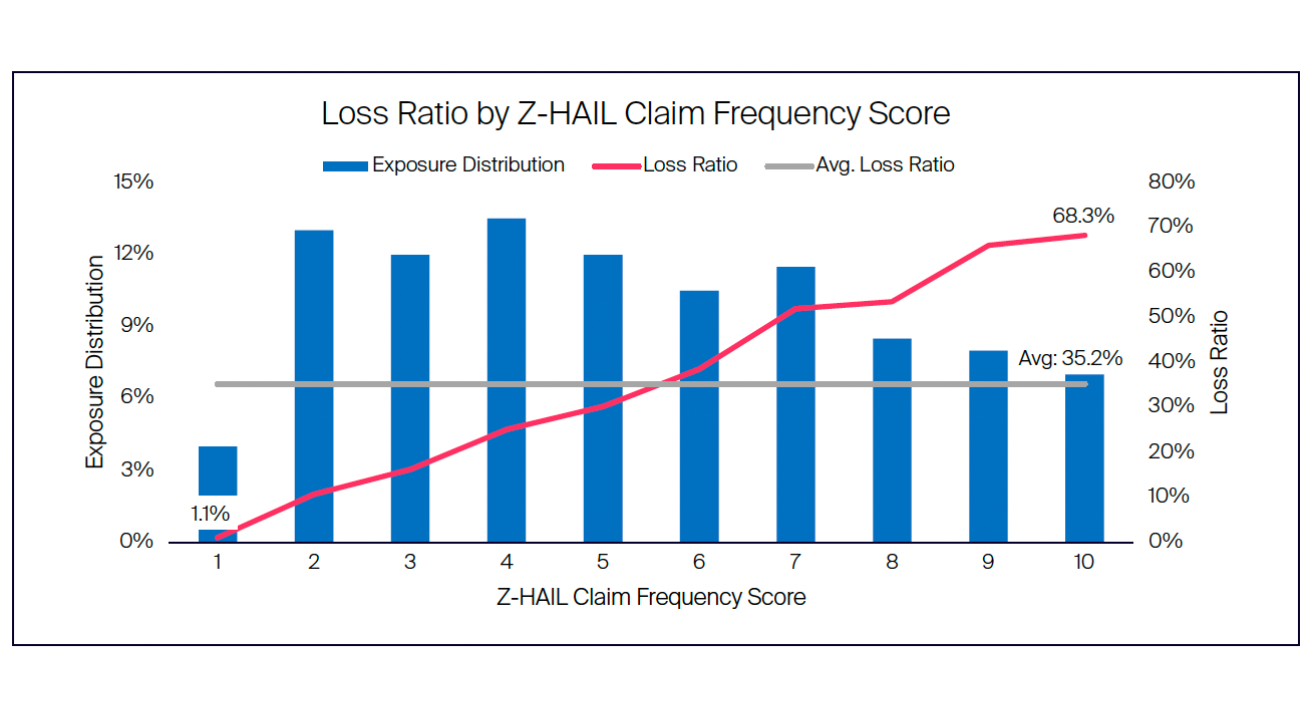

ZestyAI’s Z-HAIL and Z-WIND models are specifically designed to address the challenges posed by severe convective storms. In a new retroactive case study, we explore the performance of these models on a carrier’s book of business over the prior five years, highlighting their effectiveness in delivering comprehensive coverage and precise risk segmentation.

Key findings from the case study include:

Comprehensive Coverage with High Accuracy

One of the standout results from the case study is the exceptional hit rate of 99.7% achieved by Z-HAIL and Z-WIND. This shows the models were able to accurately identify and assess the risk of severe convective storms for nearly all the properties in the carrier's portfolio.

Strong Risk Segmentation

The models demonstrated remarkable capability in risk segmentation, with Z-HAIL generating a lift of 62X and Z-WIND achieving a lift of 9.7X. This means that the models were able to effectively differentiate between high-risk and low-risk properties, even within small geographic areas such as a single zip code. Accurate risk segmentation allows insurers to tailor their policies and pricing strategies more precisely, leading to better management of their risk exposure.

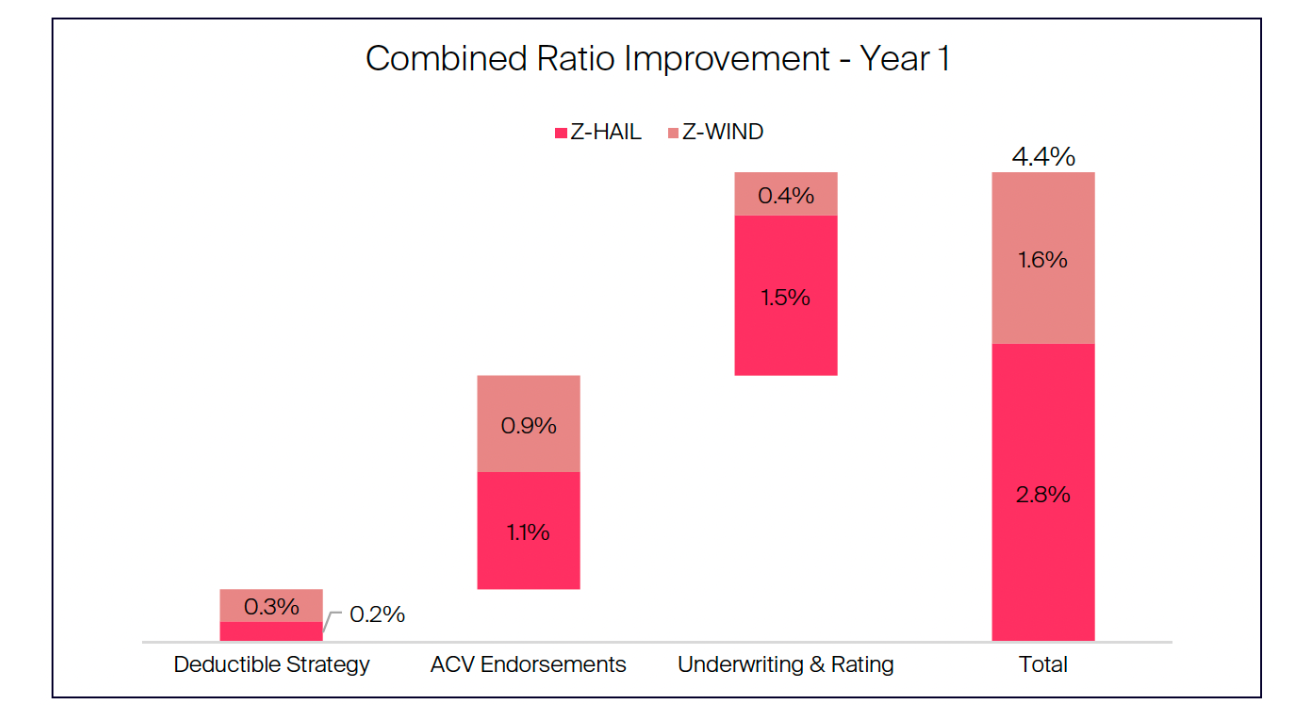

Improved Combined Ratio

Implementing Z-HAIL and Z-WIND would significantly enhance a carrier’s combined ratio, calculated to be approximately 4 points in the first year. This improvement can be attributed to the models’ ability to optimize underwriting, rating, and the application of deductibles and Actual Cash Value (ACV) endorsement strategies. By accurately assessing the risk and applying appropriate measures, insurers can reduce their loss ratios and improve overall profitability.

The Need for Innovative Solutions

As severe convective storms continue to pose significant challenges to the insurance industry, adopting innovative solutions like ZestyAI’s severe convective storm models can help insurers better manage this escalating risk.

These models provide comprehensive coverage, accurate risk segmentation, and improved financial performance. By embracing advanced technology and data-driven analytics, insurers can navigate the complexities of severe weather events and safeguard their portfolios against future losses.

To learn more about the detailed findings and benefits

Download the full case study.

Now Streaming: Roof Risk Master Class

Effective strategies for better risk management

Are rising storm costs and inaccurate roof assessments impacting your bottom line?

Now available to stream, The Science of Roof Risk master class will equip you with the latest strategies and techniques to master roof risk assessment.

- Enhance your roof risk assessment by 60X

- Improve your combined ratio

- Reduce storm-related roof claims

- Strengthen new business selection

What we cover:

Your presenters, Ross Martin (VP, Risk Analytics) and Sam Fetchero (Head of Marketing) will share with you:

- The Problem of the Roof: Uncover the underlying factors driving rising storm losses and why traditional risk assessment methods fall short.

- The Science Behind Predicting Losses: Explore key factors impacting roof risk and loss prediction, including roof age, condition, complexity, and peril-specific models.

- Accuracy-focused Risk Models: Discover advanced modeling techniques that enhance predictive accuracy.

- Understanding Storm Climatology: Learn how storm climatology impacts roof risk and how to integrate these insights into your risk assessment strategies.

- Real-World Results: Witness a comparative analysis of these predictive factors using actual carrier data. Understand the strengths and weaknesses of each approach.

- Priorities of Leading P&C Insurers:

See what your peers asked with valuable insights to take back to your team.

Who Should Watch?

This video is ideal for Executives, Product Managers, Actuaries, Underwriters, and CAT Modelers committed to enhancing their roof risk assessment capabilities.

Bonus Guide

As a bonus for watching, you'll receive a downloadable study on the latest roof risk assessment strategies: Preparing for the Storm: The Insurers Guide to Roof Risk.

Access Now

Exclusive Webinar: Mitigating Non-Weather Water Risk

New strategies to turn off the tap on insurance losses

From Costly Water Losses to Millions in Savings

Non-weather water claims are a leading cause of property insurance losses, costing insurers over $20 billion annually.

Join us for a FREE live webinar where our experts will discuss the latest trends, challenges, and insights to help you mitigate non-weather water risk.

What We'll Cover

Our experts Rob Silva, ACAS (Director of Customer Success) & Sam Fetchero (Head of Marketing) will present:

- Current Trends: Understand the rise in severity and total loss costs of non-weather water claims.

- Risk Assessment Challenges: Learn why traditional methods fall short in assessing non-weather water vulnerability.

- Key Risk Factors: Identify the main drivers of non-weather water damage.

- Strategic Insights: Discover strategies to improve your management of non-weather water claims.

- Z-WATER in Action: Experience our new AI-powered model that predicts non-weather water risk with unparalleled accuracy.

- Interactive Q&A: Get your questions answered by our experts.

Who Should Attend

This webinar is ideal for Executives, Product Managers, Actuaries, Underwriters, and CAT Modelers committed to enhancing their understanding and management of non-weather water risks.

Bonus Content

As a bonus, you'll receive our exclusive infographic, "Below the Surface: Research Reveals Knowledge Gap in Homeowner Water Loss Prevention and Coverage."

This research gives key insights into water loss experiences, coverage details, homeowner protection measures, and information on water shutoff devices and heater conditions.

Register Now

Now Available: The Insurers Guide to Roof Risk

Learn how leading insurers are mastering roof risk and maximizing lift

It’s hard to overstate how important the roof is from an insurability standpoint. The roof represents significant risks and potential opportunities, making it a critical focus area for insurers. This has become even more important in recent years as the impact of severe convective storms is often reflected in roof losses. Understanding this, ZestyAI has released new research for property insurers called The Insurers Guide to Roof Risk.

Download The Insurers Guide to Roof Risk

In an era where the severity and frequency of roof-related claims are on the rise, particularly due to the increasing impact of severe convective storms, innovative tools and strategies are essential. The Insurers Guide to Roof Risk provides actionable insights to improve risk assessment, underwriting processes, and overall business strategy.

What’s Inside the Guide?

The Insurers Guide to Roof Risk includes:

- Roof Failure Factors: Learn the underlying contributing factors behind why older roofs fail more often.

- Beyond Roof Age: Discover why roof complexity, condition, and climate are more important than roof age alone.

- Identifying Missing Risk Factors: Understand the key factors to roof risk that most traditional models miss.

- Advanced Risk Segmentation: See how using machine learning and new data sources can split risk more than 60 times better than traditional models.

- Portfolio Optimization: Access a comprehensive toolbox to optimize your portfolio and new business selection to generate exponential lift versus traditional models.

Now Available: ZestyAI’s 2024 Wildfire Season Overview

Annual Wildfire Season Overview provides insights to assist insurers in effectively managing wildfire risk.

Annual Wildfire Season Overview provides insights to assist insurers in effectively managing wildfire risk.

ZestyAI has released its annual Wildfire Season Overview for 2024. This year’s guide provides critical insights carriers need to stay ahead of the rapidly evolving wildfire landscape. Offering more than just data, this year’s guide is designed to help insurers make informed risk decisions in some of the country’s most volatile states.

Download ZestyAI's 2024 Wildfire Season Overview

This year’s guide includes:

- Countrywide Wildfire Impact Analysis: Understand how wildfires are affecting regions beyond traditional hotspots like CA, including significant events in TX & NM.

- Future Wildfire Trends: Explore predictions for the 2024 wildfire season and understand the long-term implications of current conditions on wildfire risks.

- Regulatory Insights: Stay updated on the latest regulations affecting wildfire risk assessment insurance practices.

- AI-driven Risk Models: Learn how ZestyAI's Z-FIRE model accurately predicts wildfire risks and assists insurers in making informed decisions.

- Property-Level Risk Assessments: Discover the importance of granular, property-specific risk evaluations to improve underwriting accuracy and transparency for consumers.

The Roof Age Advantage Webinar Now Available On Demand

Achieve unmatched accuracy in risk management

Costing insurers approximately $19 billion every year, roof claims stand as the primary driver of property insurance losses.

Traditional methods of obtaining roof age information are deeply flawed. Most carriers depend on policyholder or agent-reported data, which is often inaccurate, leading to blind spots in assessing property risk. In a recent ZestyAI survey, 63 percent of homeowners reported not knowing the age of their roof if they were not in their homes the last time it was replaced.

Join our expert panel for a deep dive into leveraging roof age analytics for a cutting-edge underwriting process and gain insider knowledge on:

- The Leading Cause of Claims: unveil the hidden truths behind roof-related claims and the costly consequences of outdated assessment methods.

- A New Era of Data: Learn about ZestyAI’s pioneering approach to roof age analytics, incorporating building permits, historical imagery, and AI for a comprehensive view

- Precision at Scale: See how to apply precise, AI-driven roof age data across your entire portfolio for consistent and reliable underwriting and claims decisions

- Technical Decision Making: Empower your actuaries and underwriters with the insights needed to enhance risk selection and optimize pricing strategies

- Efficiency in Operations: Streamline inspections and operations, focusing resources where they’re needed most, improving time-to-quote, and enriching the customer experience

- Best Practices: Learn how leading carriers are using roof age, roof condition, and peril-specific models to improve risk selection and lower combined ratios

This transformative session is available on demand. Learn how to enhance accuracy, efficiency, and profitability in property insurance.

Save Your Spot

See How Insights Turn Into Decisions

ZestyAI transforms data into action. Get a demo to see how the same AI powering our reports helps carriers make faster, smarter, regulator-ready decisions.