Reports & Research

Explore proprietary research packed with data, insights, and real-world findings to help carriers make smarter decisions.

.png)

AI in Insurance: How to Stay Ahead of the Curve

Artificial intelligence is reshaping the P&C insurance industry, offering new ways to streamline underwriting, enhance risk management, and navigate evolving regulations.

But as AI adoption accelerates, insurers must ensure they’re using these technologies effectively—balancing innovation with compliance.

Our latest guide explores the most impactful AI applications in insurance, including:

- AI-powered underwriting and predictive analytics

- How regulators are shaping the future of AI in insurance

- Best practices for integrating AI while ensuring fairness and transparency

As AI-driven tools become the new standard, insurers who adapt early will gain a competitive edge.

Download our free guide to leverage these innovations while staying aligned with evolving regulations.

The Truth About Roof Age: 5 Critical Insights Every Insurer Should Know

For insurers, accurate roof age data is essential. Yet, self-reported information often falls short.

Our research shows that 1 in 5 homeowners underreport roof age by an average of 8 years. These discrepancies create hidden risks that can impact underwriting, pricing, and overall portfolio performance.

How can insurers get a more accurate picture?

AI-driven insights provide 97% nationwide coverage, combining verified roof age with real-time condition data for a more comprehensive risk assessment.

Download our latest research for a breakdown of five critical insights that every insurer should know about roof age.

Plus, get access to The Roof Age Advantage, an exclusive video that unveils how AI is setting a new standard for risk evaluation.

Now Streaming: Navigating California's Evolving Insurance Landscape

The California Department of Insurance (CDI) has introduced significant updates as part of its Sustainable Insurance Strategy. These new bulletins and draft regulations aim to accelerate regulatory approvals, embrace forward-looking models, and address critical reinsurance challenges.

But what do these changes mean for insurance carriers—and how can you prepare?

On January 29, 2025, we hosted a webinar, California’s Evolving Insurance Landscape: The Future of Insurance in the Golden State.

Designed for Legal & Compliance professionals, Product Managers, Underwriters, Actuaries, and Risk & Innovation leaders, the discussion featured expert insights from:

- Michael Peterson, Deputy Commissioner of Climate & Sustainability, California Department of Insurance

- Karen Collins, VP, Property & Environmental, APCIA

- Bryan Rehor, Head of Regulatory Affairs, ZestyAI

Missed the live event but want to gain actionable insights from industry leaders at the forefront of California’s insurance evolution? Watch on demand now!

Webinar: Regulatory Ready - How to Use AI Responsibly in Insurance

Gain a deeper understanding of the NAIC bulletin's principle-based approach to AI regulation and what it means for carriers.

Regulatory Ready: How to Use AI Responsibly in Insurance Under the NAIC Bulletin

AI innovation is revolutionizing the insurance industry, but with these advancements come new regulatory challenges. To ensure responsible use of AI in insurance, it’s essential to stay informed about the latest regulatory frameworks.

Join us on November 13 at 11 PT / 2 ET for an exclusive webinar where we’ll break down how to navigate AI regulations under the NAIC Model Bulletin.

In this session, led by

- Kevin Gaffney, Vermont’s Commissioner of Financial Regulation and Chair of the NAIC’s Innovation & Tech Committee

- Bryan Rehor, Director of Regulatory Strategy at ZestyAI

you'll gain critical insights on how to align AI usage with evolving regulatory expectations.

What You’ll Learn

This webinar will provide practical takeaways that can help insurance professionals understand and comply with the latest AI standards:

- NAIC Model Bulletin Overview: Understand the core principles behind the NAIC’s AI regulation framework.

- Ensuring AI Compliance: Learn how to ensure responsible AI usage according to NAIC standards.

- Preparing for Regulatory Oversight: Get ready for closer state-level inspections and regulatory scrutiny.

- Vendor & Partner Compliance: Ensure that your partners meet regulatory requirements for transparency and fairness.

- Interactive Q&A: Take advantage of the opportunity to ask our experts about the complex world of AI and insurance compliance.

Meet the Experts

Kevin Gaffney

Vermont Commissioner of Financial Regulation

As an expert in AI regulations and the NAIC’s Model Bulletin, Commissioner Gaffney will provide key insights into how insurance companies can effectively implement responsible AI practices. His experience in overseeing state-level financial regulation will offer attendees a unique perspective on aligning AI innovation with compliance.

Bryan Rehor

Director of Regulatory Strategy at ZestyAI

Bryan Rehor will offer practical advice on maintaining AI compliance while harnessing the full potential of AI innovation. His expertise lies in guiding insurers through regulatory demands, ensuring that AI practices meet industry standards while avoiding common pitfalls.

Why You Should Attend

This webinar is tailored for professionals in insurance, particularly those in Executive, Legal, Compliance, Product Management, Underwriting, Actuarial, Risk, and Innovation roles.

Whether you’re navigating the complexities of AI regulation or preparing for the next steps in compliance, this session will provide actionable insights to help you move forward confidently.

Bonus Content

By registering for the webinar, you’ll receive our interactive guide:

“When Innovation & Regulation Meet: What Insurers Need to Know About AI and Regulatory Compliance.”

This resource will deepen your understanding of how to stay compliant while leveraging the power of AI in your insurance operations.

Don’t miss out!

Register for the webinar and ensure your spot in this exclusive event.

.png)

The State of the Industry: AI Adoption in Climate Risk Management

A survey of insurance professionals highlights AI models gaining traction, key insurer priorities, and the impact of transparency and regulatory concerns.

Facing Unprecedented Climate Challenges

The insurance industry is facing unprecedented challenges as natural catastrophic events like convective storms and wildfires become more frequent and severe. Traditional risk models, which often rely on broad territory-based segmentation, are struggling to keep up with these dynamic environmental threats. This has led to significant financial losses for insurers, who are now seeking more accurate and proactive methods to predict and manage climate risk.

AI Adoption in Property and Casualty Insurance

To shed light on the adoption of these cutting-edge techniques, ZestyAI conducted a survey of over 200 executives in the Property and Casualty (P&C) insurance sector. The survey reveals which AI-based models are gaining traction, what features insurers prioritize, and how transparency and regulatory concerns are shaping the industry. It also highlights the specific risks that are top of mind for carriers today.

AI Transforming Risk Assessment Models

The industry is turning to AI-based risk assessment models that offer a new level of precision. Companies like ZestyAI are leading the charge, providing tools that enable insurers to assess risk on a property-by-property basis, considering both individual property features and their interaction with surrounding environmental factors. These advanced models are transforming the way insurers underwrite policies, optimize portfolios, and align coverage with actual needs.

Dive deeper into our findings and explore the full report by clicking below.

Access the Report

Case Study: Adapting to Escalating Severe Convective Storm Risk

Insights from a 5-year retrospective on ZestyAI’s models in action

The Rising Threat of Severe Convective Storms

The past few decades have seen a dramatic rise in the frequency and intensity of severe convective storms, resulting in significant financial repercussions for the insurance industry. In the last year alone, insured losses from severe convective storms reached an astounding $60 billion, marking an average annual growth rate of over 11% over the past twenty years. This alarming trend means a new approach is needed to manage and mitigate the escalating risks associated with severe weather events.

In the last year alone, insured losses from severe convective storms reached an astounding $60B, marking an average annual growth rate of over 11% over the past twenty years.

The traditional methods of risk assessment and management are no longer sufficient to cope with the increasing unpredictability and severity of these weather events. As the risk evolves, so must the solutions. Changing risks call for innovative solutions that leverage advanced technology and data analytics to enhance the accuracy and effectiveness of risk modeling.

A New Approach

ZestyAI’s Z-HAIL and Z-WIND models are specifically designed to address the challenges posed by severe convective storms. In a new retroactive case study, we explore the performance of these models on a carrier’s book of business over the prior five years, highlighting their effectiveness in delivering comprehensive coverage and precise risk segmentation.

Key findings from the case study include:

Comprehensive Coverage with High Accuracy

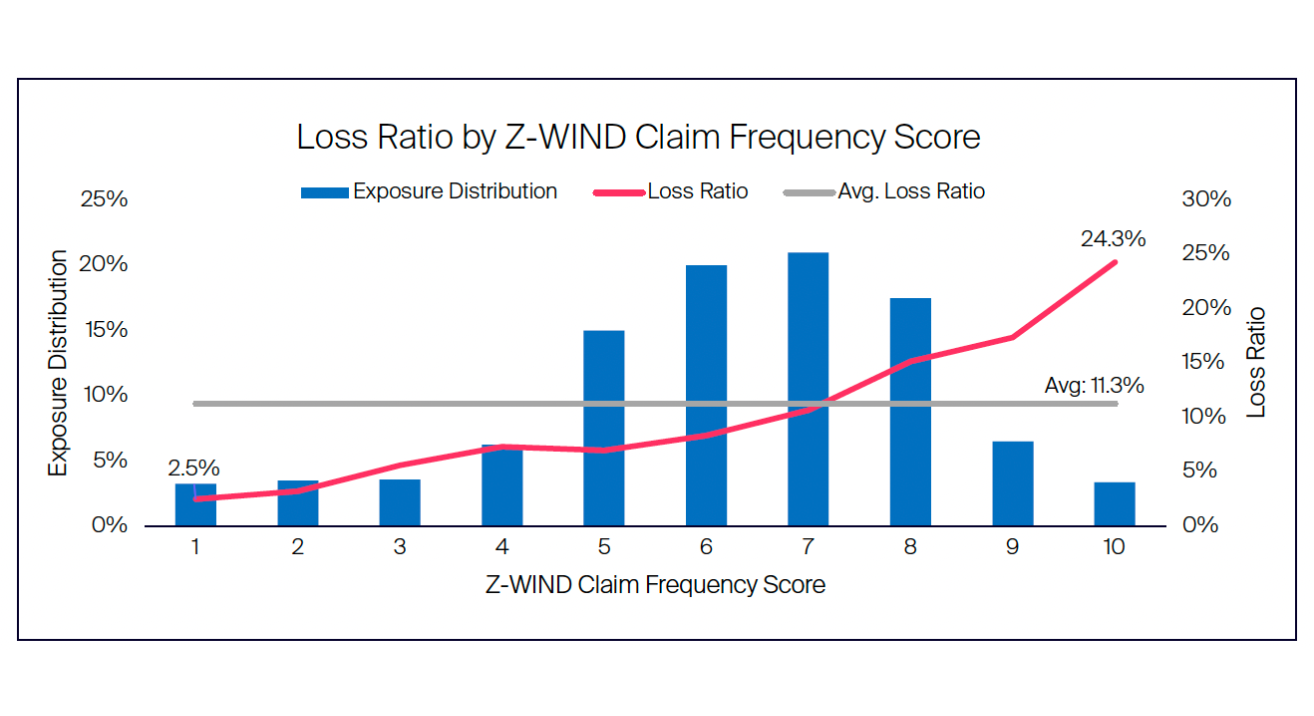

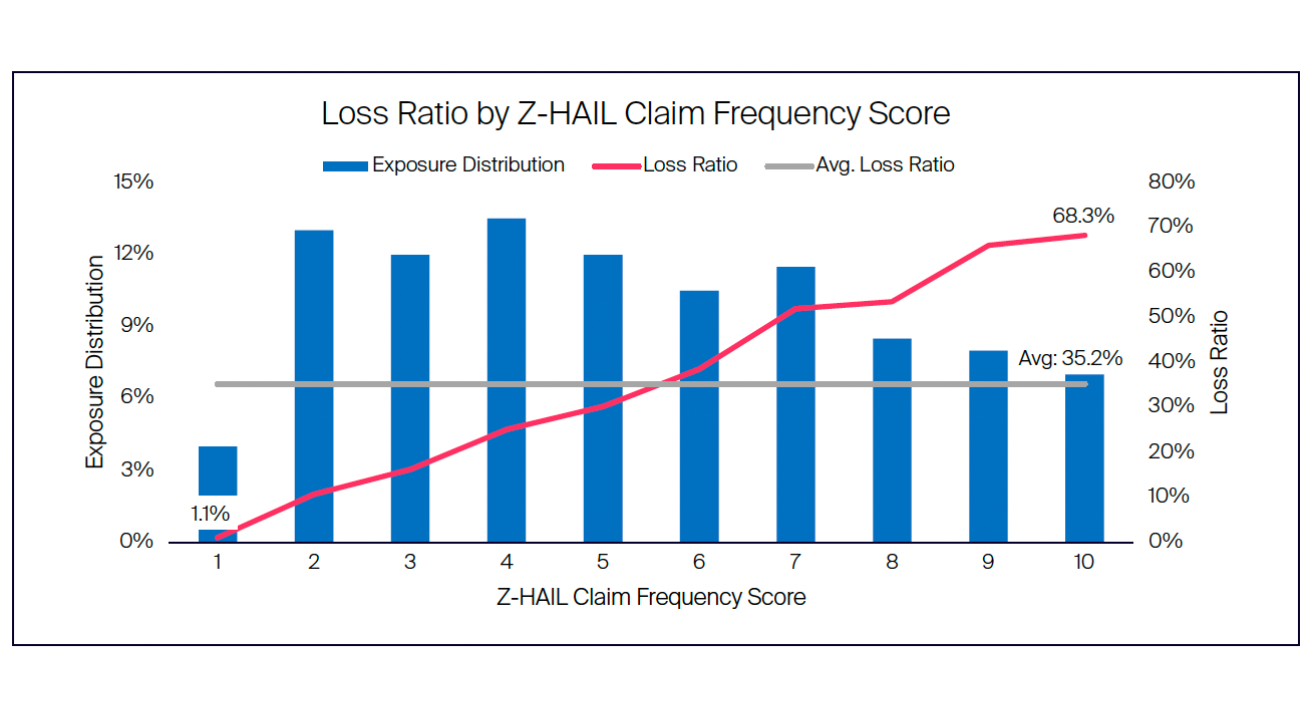

One of the standout results from the case study is the exceptional hit rate of 99.7% achieved by Z-HAIL and Z-WIND. This shows the models were able to accurately identify and assess the risk of severe convective storms for nearly all the properties in the carrier's portfolio.

Strong Risk Segmentation

The models demonstrated remarkable capability in risk segmentation, with Z-HAIL generating a lift of 62X and Z-WIND achieving a lift of 9.7X. This means that the models were able to effectively differentiate between high-risk and low-risk properties, even within small geographic areas such as a single zip code. Accurate risk segmentation allows insurers to tailor their policies and pricing strategies more precisely, leading to better management of their risk exposure.

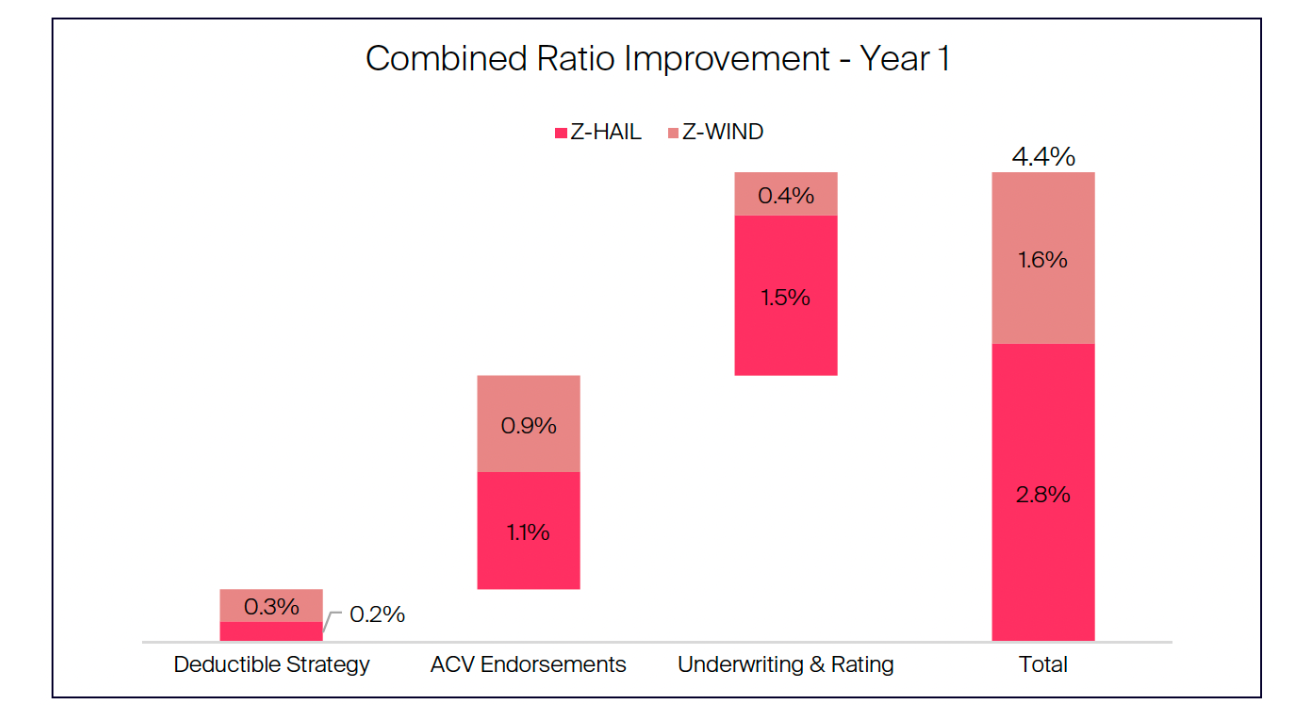

Improved Combined Ratio

Implementing Z-HAIL and Z-WIND would significantly enhance a carrier’s combined ratio, calculated to be approximately 4 points in the first year. This improvement can be attributed to the models’ ability to optimize underwriting, rating, and the application of deductibles and Actual Cash Value (ACV) endorsement strategies. By accurately assessing the risk and applying appropriate measures, insurers can reduce their loss ratios and improve overall profitability.

The Need for Innovative Solutions

As severe convective storms continue to pose significant challenges to the insurance industry, adopting innovative solutions like ZestyAI’s severe convective storm models can help insurers better manage this escalating risk.

These models provide comprehensive coverage, accurate risk segmentation, and improved financial performance. By embracing advanced technology and data-driven analytics, insurers can navigate the complexities of severe weather events and safeguard their portfolios against future losses.

To learn more about the detailed findings and benefits

Download the full case study.

Universal North America Insurance Company Adopts ZestyAI’s Roof Age Solution

Partnership brings AI-powered verified roof age to strengthen risk decisions and portfolio performance

ZestyAI, the leading provider of AI-powered property and climate risk analytics, today announced that Universal North America Insurance Company, a property insurer, part of the One Alliance Group of companies, has adopted ZestyAI’s Roof Age solution to bring greater accuracy and confidence to property risk assessment across its portfolio.

Why Accurate Roof Age Data Matters

Roof-related claims are among the costliest in property insurance. Yet insurers have long struggled with inconsistent or incomplete roof age data. ZestyAI’s analysis shows that nearly one in three roofs are at least five years older than recorded in policy data, creating blind spots that drive higher losses and mispriced policies.

How ZestyAI’s Roof Age Model Works

ZestyAI’s Roof Age solution closes this gap by synthesizing building permit data with two decades of high-resolution aerial imagery, applying advanced machine learning to deliver verified roof age estimates with 97% U.S. coverage.

Strengthening Portfolio Performance

"Accurate roof data is foundational for managing one of the costliest drivers of property insurance losses,” said Miguel Barrales, President of Universal North America Insurance Company. “ZestyAI’s Roof Age solution provides the reliability we need to make more confident risk decisions and strengthen portfolio performance.”

"For years, insurers have had to make critical decisions without reliable roof data, and the cost has been enormous,” said Attila Toth, Founder and CEO of ZestyAI. “Universal North America Insurance Company’s adoption shows what’s possible when carriers embrace trusted, property-level insights to strengthen their portfolios and the market as a whole.”

ZestyAI Secures Regulatory Approval for Z-WATER™ in Wisconsin

AI-powered model addresses the #1 driver of non-catastrophic property losses, non-weather water

ZestyAI, the leading provider of AI-powered property and climate risk analytics, today announced that its non-weather water risk model, Z-WATER™, has received approval in Wisconsin for use in underwriting and rating.

Why Non-Weather Water Losses Are Rising

Non-weather water is one of the costliest and fastest-growing perils in homeowners insurance, now ranking as the fourth costliest peril overall, with claim severity up 80% over the past decade—surpassing hurricanes. These losses stem from everyday risks like burst pipes, appliance failures, and plumbing leaks. With average claim costs now exceeding $13,000, their financial impact rivals catastrophe events.

How the Z-WATER Model Works

Z-WATER is built, tested, and validated with real insurer loss data, ensuring accuracy and regulatory credibility. The model uses computer vision to analyze aerial imagery alongside tax assessor data, permit records, climatology science, and infrastructure insights to assess key property-level risk factors. By modeling how these variables interact, Z-WATER predicts both the frequency and severity of non-weather water claims with up to 18x greater accuracy than traditional models.

What This Approval Enables for Insurers

With this approval, insurers in Wisconsin can begin using Z-WATER to:

- Set more accurate, property-specific rates

- Align coverage with actual home vulnerabilities

- Optimize inspections and mitigation strategies, such as the adoption of water sensors

- Reduce cross-subsidization and improve portfolio performance

Regulatory Confidence in Explainable AI

“Non-weather water is one of the most frequent and expensive sources of loss for insurers, and it behaves differently than other perils,” said Bryan Rehor, Director of Regulatory Strategy at ZestyAI.

“Z-WATER captures the property-level features that truly drive risk—such as plumbing systems, home design, and even vegetation patterns, giving insurers a much clearer picture of where losses are likely to occur.

"This approval demonstrates that regulators recognize the value of AI models that are explainable, data-driven, and validated against real claims," he added.

Part of a Growing Nationwide Regulatory Track Record

This approval adds to ZestyAI’s growing regulatory momentum. Across five perils, including wildfire, hail, wind, storm, and now non-weather water, ZestyAI has secured more than 70 approvals coast-to-coast.

In addition to these peril models, ZestyAI’s Z-PROPERTY™ solution has also earned nationwide approvals, giving insurers trusted roof and parcel-level insights with the same regulatory credibility.

Southern Oak Deploys ZestyAI’s Risk Platform to Improve Risk Visibility and Reduce Losses in Florida

Granular insights into roof and parcel-level risk help reduce storm losses and strengthen portfolio performance across Florida’s high-risk market

Southern Oak Insurance Company, a Florida-based insurer specializing in personal residential property coverage, has adopted ZestyAI’s AI-powered property risk platform to improve visibility into property condition and exposure across its homeowners portfolio.

By analyzing structural and environmental vulnerabilities, such as roof degradation, overhanging vegetation, yard debris, and secondary structures, ZestyAI’s platform equips Southern Oak to take targeted actions that help reduce losses and manage exposure more effectively. These granular, property-level insights also offer a clearer view of changing risk conditions across one of the most challenging insurance markets in the country.

Southern Oak is leveraging two core capabilities within ZestyAI’s Z-PROPERTY solution:

- Digital Roof applies AI to high-resolution aerial imagery to assess roof complexity, materials, and condition, flagging structural vulnerabilities before they become claims.

- Location Insights evaluates the broader parcel to surface risk factors such as vegetation overhang, yard debris, and secondary structures that can amplify storm losses or drive claim severity.

“ZestyAI stood out for its ability to provide deep, 3D visibility into the condition and complexity of the properties we insure.”

“ZestyAI stood out for its ability to provide deep, 3D visibility into the condition and complexity of the properties we insure,” said Tony Loughman, CEO of Southern Oak Insurance Company. “These insights help us improve our risk decisions and manage exposure more effectively across a high-risk geography, while continuing to deliver value and stability to our policyholders.”

“Southern Oak is taking a proactive, data-driven approach to strengthen portfolio decisions,” said Attila Toth, Founder and CEO of ZestyAI. “In Florida’s uniquely challenging insurance market, resilience depends on seeing risk clearly at the property level—and acting on it.”

Mitigation Aware Scoring for Severe Convective Storm Risk

Changes such as upgrading or replacing roofs and addressing structural deficiencies will automatically influence risk scores

ZestyAI today announced a new enhancement to its Severe Convective Storm (SCS) risk suite that enables carriers to adjust model inputs and risk scores based on mitigation efforts.

The enhancement gives insurers a structured and scalable way to reflect real-world improvements, such as upgrading roof materials, replacing aging roofs, or addressing structural deficiencies, directly within property-level risk assessments.

What the New Capability Enables

Carriers can now instantly update risk scores based on verified property data, enabling three key use cases:

- Reflecting completed mitigation: Recognize risk-reducing actions like roof upgrades or structural improvements in real time, improving rating accuracy and customer satisfaction.

- Correcting inaccurate data: If errors are identified, such as incorrect roof material, carriers can transparently correct inputs to ensure fairer, more accurate risk assessments.

- Simulating future changes: Carriers can model the potential impact of proposed upgrades before they occur, helping agents and homeowners understand the value of mitigation and reinforcing behavior that reduces future losses.

Why It Matters for Carriers and Policyholders

Kumar Dhuvur, Co-Founder and Chief Product Officer of ZestyAI, said:

“Models should be powerful, but also flexible and responsive to real-world improvements.”

“By giving carriers the ability to incorporate mitigation and field data into model outputs, we’re supporting transparent, action-oriented risk management that benefits both insurers and homeowners.”

This mitigation-aware functionality is already in use across ZestyAI’s wildfire products, including Z-FIRE™ and Compliance Pre-Fill, where it supports critical regulatory filings and enables carriers to reflect mitigation actions like defensible space and Class A roofs. Extending this capability to the SCS suite ensures a consistent, carrier-controlled approach to incorporating verified improvements across perils.

Built for Transparency and Human-in-the-Loop Decisioning

This enhancement reflects ZestyAI’s broader commitment to human-in-the-loop AI, where insurers remain in control of key decisions and have visibility into the data behind every score.

By combining transparency with the ability to incorporate verified updates, ZestyAI helps carriers build trust with both regulators and policyholders while ensuring model outputs remain grounded in real-world conditions.

The score adjustment capability is seamlessly integrated into the ZestyAI platform and supports a wide range of use cases, including improving product fit, optimizing inspection workflows, enhancing underwriting decisions, and ensuring rating accuracy.

The Z-HAIL™, Z-WIND™, and Z-STORM™ models are built on real-world claims data and leverage property-specific features such as roof geometry, condition, and vegetation to deliver more accurate risk insights than traditional territory-based models.

ZestyAI’s storm models are approved for use in over 20 states across the Great Plains, Midwest, and U.S. South, regions most impacted by severe convective storms, and are actively used by carriers for rating and underwriting.

Steadily Selects ZestyAI to Strengthen Underwriting for Landlord Insurance

Top-rated insurer deepens partnership with ZestyAI to strengthen landlord underwriting with parcel-level hail and wind insights

ZestyAI today announced an expanded partnership with Steadily, a top-rated insurer for rental properties, to deliver advanced hail and wind risk models that enable more precise underwriting. Building on a successful rollout in 2024, Steadily is broadening its use of ZestyAI’s property-specific insights to better assess storm risk and support growth across high-exposure states.

With operations in all 50 states and $300 million in annualized gross written premium, Steadily is one of the fastest-growing insurers in the U.S.

Steadily first adopted ZestyAI’s Z-HAIL™ and Z-WIND™ models in four high SCS states. With a successful proof of concept, the company is now extending usage to additional states in the coming months.

Datha Santomieri, Co‑Founder & COO of Steadily, said:

“Expanding our use of ZestyAI’s hail and wind models reaffirms our commitment to precision and efficiency in landlord underwriting. These insights help us make informed decisions quickly and manage exposure with greater confidence.”

ZestyAI’s platform predicts the likelihood and severity of storm-related claims by analyzing how localized climatology interacts with individual property characteristics — a sharp contrast to traditional models that rely on ZIP code or territory-level assessments. Each model is built and validated on extensive real-world claims data and delivers transparent explanations of the key factors behind every risk score.

Together, Z-HAIL and Z-WIND help insurers identify storm risk at the parcel level by evaluating roof condition, structural complexity, historical losses, and local storm exposure, enabling the granularity needed to underwrite confidently in volatile regions.

“Steadily is modernizing a critical segment of the market with their customer-centric, tech-forward approach,” said Attila Toth, Founder and CEO of ZestyAI.

“We’re proud to support their growth with AI-driven insights that enable better pricing, smarter underwriting, and more resilient portfolios.”

ZestyAI’s severe convective storm models are currently approved by regulators in 19 states and used by leading insurers across the country.

Enterprise Data Quality: The Hidden Risk in Insurance

In insurance, data is destiny. The problem is that most carriers don’t actually trust the data they’re working with.

After years of working with leading insurers, one reality has become undeniable: enterprise data quality is one of the biggest hidden risks in the industry.

The Problem: Carriers Don’t Trust Their Own Data

Data enters the system at the quote stage. That means it often comes directly from agents and policyholders—well-intentioned, but subjective. Did the policyholder really know the exact roof age? Did the agent catch the secondary structures in the backyard?

Inspection resources are limited, and most carriers can’t validate this information at scale. The result is a house of cards: data that looks complete in the policy system, but is riddled with blind spots and inconsistencies.

And even when the data is accurate in the moment, it quickly decays. Structures are living assets, meaning:

- Roofs degrade.

- Weather events roll through.

- Families expand, renovate, and change how they use the property.

- Secondary structures, pools, trampolines, and solar panels appear overnight.

The underwriting file that was “clean” at binding can be outdated and incomplete by renewal. Over time, carriers lose confidence that they have a real view of risk.

The Six Dimensions of Data Quality

Data quality isn’t one thing—it’s multidimensional. For carriers, the challenge is ensuring property data is:

- Accurate: Correct at the point of use, not just at intake.

- Complete (and unbiased): Captures all risk-relevant details, verified against independent sources so fields aren’t left blank, misstated, or skewed by incentives.

- Consistent: Aligned across systems, from quoting to claims.

- Valid: Structured to meet business and regulatory rules.

- Timely: Refreshed when things change, not years later.

- Unique: De-duplicated, with a single source of truth.

By this standard, most carrier data today is falling short.

From Data Quality to Data Integrity

Data quality is foundational, but it’s only part of the picture. True data integrity comes from combining accurate data with the right context and continuous observability.

That means not just having the right roof age or square footage, but knowing whether that data has changed, and whether it aligns with other signals in the environment. It means having a complete, transparent, and continuously updated picture of every property.

The ZestyAI Solution: Verified, Transparent Property Data

At ZestyAI, we built our property intelligence platform to solve exactly this problem. By unifying multiple independent data streams—and applying AI to synthesize them—we deliver property data that carriers can trust.

Here’s how we do it:

Imagery + Computer Vision

We ingest aerial, satellite, and terrestrial imagery, then apply over 90 proprietary computer vision models. These models don’t just “see” a property; they interpret it. That means extracting hard-to-get details like:

- Roof condition and penetrations

- Yard debris and overhanging vegetation

- Secondary structures and solar panels

This creates a dynamic, objective record of what’s on the ground, property by property.

Geospatial and Hazard Data

Context matters. We overlay geospatial layers to understand how a property interacts with its environment, including wildfire exposure, flood risk, and more.

Building Permits

Using large language models (LLMs), we extract and synthesize the real changes reflected in building permits: bathrooms added, kitchens renovated, roof replacements, solar installations. Permits reveal what’s changed, not just what was once approved.

Market and Public Records

We enrich the picture with MLS transactions, tax assessments, climatology, topography, and infrastructure data. Together, these data sources confirm and contextualize what imagery and permits reveal.

Standards and Designations

We integrate authoritative designations, such as IBHS Fortified™ standards, to validate resilience features.

Each data source adds a layer of verification. Together, they create a comprehensive, continuously updated property record that carriers can rely on.

Why This Matters: Enterprise Data Quality Transformed

When carriers bring ZestyAI data into their systems, the impact is immediate:

- More Accurate Underwriting and Rating: Quote data is validated against independent sources. That means fewer surprises at claim time, more consistent rating, and appropriate premiums.

- Change Detection and Accurate Renewals: Our models detect what’s changed since policy inception, leading to smarter renewal decisions, more proactive outreach to policyholders, and reduced leakage.

- Better Reinsurance Negotiations: Clean, transparent data helps carriers secure the right terms, conditions, and pricing from reinsurers—because they can prove their book is based on verified risk, not guesswork.

- Operational Efficiency: By replacing guesswork and manual inspection with AI-verified data, carriers reduce expenses and focus resources where they matter most.

- More Accurate Customer Communications: Data quality isn’t just about pricing and underwriting. It’s about trust. Verified property details enable carriers to send personalized, timely, and accurate communications.

- Renewal notices, policy updates, or even hurricane prep guidance land with credibility because they reflect the customer’s real property. That strengthens engagement, reduces confusion, and builds long-term retention.

The Bottom Line

Carriers can’t compete in today’s market with messy, decaying data. Enterprise data quality is no longer a “back office” concern. It’s a competitive edge.

ZestyAI’s property intelligence platform solves the problem at its core: by continuously verifying property data with imagery, geospatial science, permits, and AI-powered interpretation.

That’s how carriers build trust in their data. That’s how they write better risks, renew smarter, negotiate stronger, and communicate with customers more effectively.

Want to see how ZestyAI can transform your enterprise data quality? Contact us for a demo.

See How Insights Turn Into Decisions

ZestyAI transforms data into action. Get a demo to see how the same AI powering our reports helps carriers make faster, smarter, regulator-ready decisions.