Reports & Research

Explore proprietary research packed with data, insights, and real-world findings to help carriers make smarter decisions.

.png)

ZestyAI Publishes Data-Driven Look at 2022 Wildfire Season

2022 Wildfire Season Overview looks back at 2021 and ahead to what may be a long year of wildfires in 2022.

Today, ZestyAI released its 2022 Wildfire Season Overview. Each year, ZestyAI prepares a comprehensive overview to help guide insurers based on recent wildfire events, persistent drought conditions, and advancements in artificial intelligence for managing wildfire risk.

If it seems like wildfires are burning at all times of the year, it's not just you. Very destructive events, like last December's Marshall Fire, are occurring in months not typically associated with high wildfire danger. Those who study wildfires, including ZestyAI, have begun to start thinking in wildfire "years" instead of wildfire "seasons'. Strong wildfire years, with 10+ million acres burned, have quickly become the new normal. The last 10 years have been the worst on record for property and casualty (P&C) insurers when it comes to wildfire. 8 of the top 20 fires in California history, and more than half of the acreage burned by them, occurred in just the years 2020 and 2021.

What can insurers do to prepare themselves for persistent wildfires?

- Understand the Data: Instead of sticking with decades-old approaches, assess wildfire risk at the property level.

- Continue to Bring Transparency and Education to Homeowners: Insights from AI-based wildfire risk models may be passed on to homeowners and agents, enabling a much better understanding of wildfire risk.

- Find the Right Technology Partner: Aerial and satellite imagery, machine learning, and infinitely scalable cloud computing resources were combined to build the most granular wildfire risk assessment model (Z-FIRE™). Using Z-FIRE™, ZestyAI can accurately estimate an individual property’s wildfire risk, plus highlight the key property-level factors that contribute to that risk.

Click here to download ZestyAI's 2022 Wildfire Season Overview.

ZestyAI offers insurers and real estate companies access to precise intelligence about every property in North America. The company uses AI, including computer vision, to build a digital twin for every building in North America, encompassing 200B property insights accounting for all details that could impact a property’s value and associated risks, including the potential impact of natural disasters. Visit https://zesty.ai for more information.

The 2021 Wildfire Season has Devastating Potential

A Data-Driven Conversation about the US West’s Megadrought

Current climate conditions in the West reveal that 2021 may have a higher than normal risk for wildfire losses. While much of this report focuses on California, historically the worst victim of wildfire in the US, the entire western US is of concern in 2021. In particular, the expansion of deep drought into Colorado is of major concern.

Drought is a leading factor in seasonal wildfire risk. With drought extending through every western state this spring, insurers should consider looking deeply into how they are addressing this growing peril. According to AON, last year’s wildfires in the US West cost insurers over $8 billion.

We've released a complete detailing the devastating potential for 2021's wildfire season. The full report is available here.

Nearly Doubling a Property’s Wildfire Survival Rate: New Study from ZestyAI in Collaboration with IBHS Shows Impact of Key Mitigation Action

Research across more than 71,000 properties involved in wildfires draws significant links between fuel management and property survival.

Oakland,Calif., April 8, 2021: ZestyAI, a leader in climate risk analytics powered by Artificial Intelligence (AI), and the Insurance Institute for Business & Home Safety (IBHS) today released new research on how fuel management impacts destruction rates from wildfires. They found property owners who clear vegetation from the perimeter of their home or building can nearly double their structure's likelihood of surviving a wildfire.

ZestyAI, in conjunction with, IBHS studied more than 71,000 properties involved in wildfires between 2016 and 2019 to assess the relationship between vegetation, buildings, and property vulnerability. To do this, ZestyAI leveraged a combination of computer vision and AI to analyze high resolution satellite and aerial imagery of the properties that fell within the wildfire perimeter, which allowed them to determine what effects a property's physical environment had on its likelihood of survival. They found buildings with a high amount of vegetation within 5 feet of the structure were destroyed in a wildfire 78 percent of the time -- a rate nearly twice as high as those with small amounts of perimeter vegetation. This pattern held true as ZestyAI analyzed the other defensible zones, ranging from 30 to 100 feet around the property.

"It's common sense that increased vegetation increases wildfire risk, but this study shows just how powerful individual action can be in safeguarding structures. Mitigation actions that can cut risk nearly in half are statistically meaningful to anyone with a stake in this peril," said Attila Toth, CEO of ZestyAI. "These findings also underscore how wildfire research at IBHS and artificial intelligence at ZestyAI translates to real-world impact at the intersection of homeowners, community leaders, regulators, and insurance carriers. This type of collective action will help protect our communities from the devastating impact of wildfire, which unfortunately has continued to increase over the last decade."

The study also supported and confirmed takeaways from IBHS's Suburban Wildfire Adaptation Roadmaps released last year, which go beyond the home ignition zone to detail additional actions needed across eight aspects of a home to address a home's wildfire vulnerability. ZestyAI's new research found that having other structures in close proximity to a property increases its wildfire risk, particularly for properties in areas with moderate to high vegetation coverage. Buildings in these areas that had another structure within 30 to 100 feet from the property were destroyed in a wildfire 60 percent of the time, compared to a 31 percent destruction rate for homes without another structure in close proximity.

"This research further demonstrates to homeowners, community leaders, and policy makers just how impactful taking the mitigation actions laid out in the Suburban Wildfire Adaptation Roadmaps can be in protecting homes from wildfire ignition," said Roy E. Wright, President & Chief Executive Officer at IBHS. "Quantifying the effect of mitigating fuel density risk, one of the critical actions identified in the Roadmaps, is a first piece in the larger puzzle of what groups of mitigation actions most improve the chance of home survival and by what level."

ZestyAI is uniquely equipped to support this type of research because of the proprietary wildfire property loss database it developed for Z-FIRE™, its AI model that generates property-specific predictive risk scores. Z-FIRE™ has been trained on more than 1,200 wildfire events across several decades and accounts for the property-level factors that contribute to wildfire risk, including defensible space, building material, and roof pitch, which legacy models fail to consider.

Wright added, "While it is not possible to eliminate wildfire risk we are not powerless against it. We must take a pragmatic approach to mitigate risk at all levels and ultimately reduce property damage through data and science. Through collaborations with modelling organizations like ZestyAI, advanced technology like computer vision and AI help us better understand the impact of these actions at a larger scale. It is encouraging to see emerging progress in just the first months of 2021."

For additional insights you can read the full research paper, ‘Wildfire Fuel Management and Risk Mitigation - Where to Start?' here. For more information on ZestyAI please visit www.zesty.ai, and for more information on IBHS please visit www.ibhs.org.

About ZestyAI (www.zesty.ai): Increasingly frequent natural disasters, such as wildfires, floods and hurricanes devastated communities and drove $2.2 Trillion in economic losses over the past decade. ZestyAI uses 200Bn data points, including aerial imagery, and artificial intelligence to assess the impact of climate change one building at a time. ZestyAI has partnered with leading insurance companies and property owners helping them protect homes, businesses and support thriving communities. ZestyAI was named Top 100 Most Innovative AI Company in the world by CB Insights in 2020, and Gartner Cool Vendor in Insurance by Gartner Research in 2019. For more information visit: https://www.zesty.ai/

About the Insurance Institute for Business & Home Safety (IBHS)

The IBHS mission is to conduct objective, scientific research to identify and promote effective actions that strengthen homes, businesses and communities against natural disasters and other causes of loss. Learn more about IBHS at DisasterSafety.org.

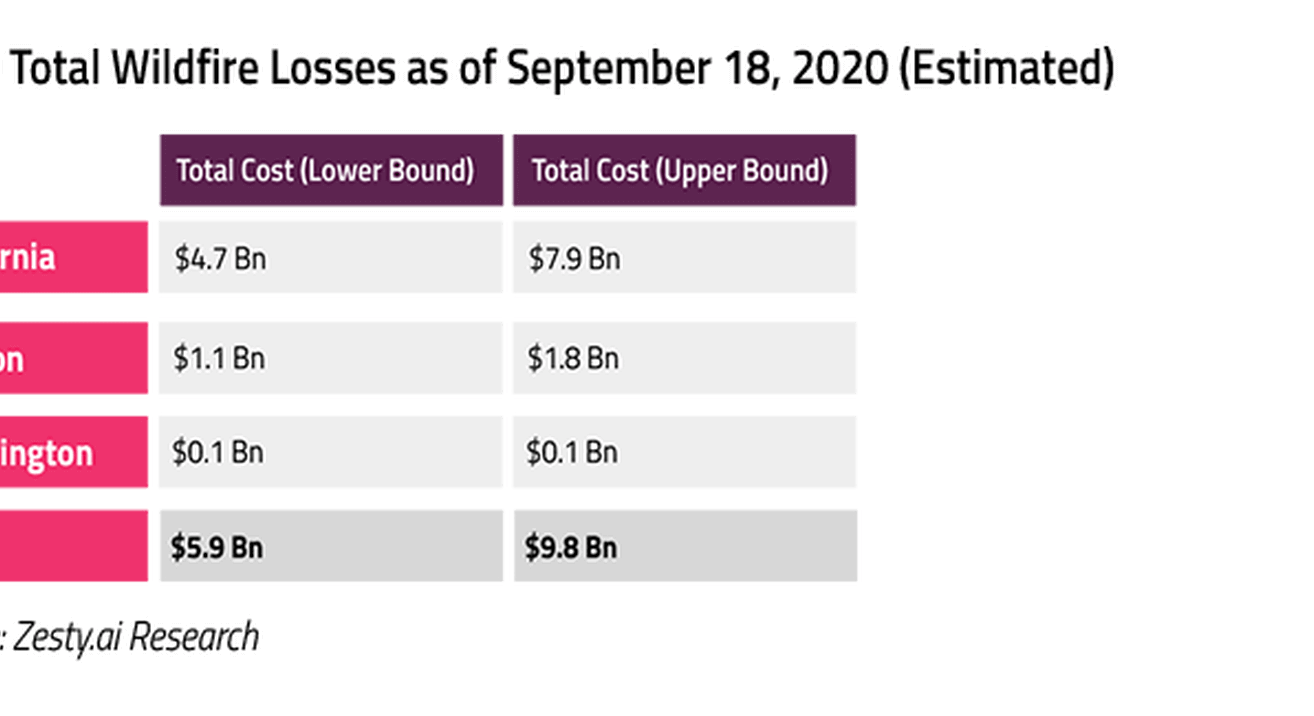

ZestyAI Research: Up to $9.8Bn in Losses Already Caused by Wildfires in 2020

As of September 18th, between $5.9Bn and $9.8Bn in losses have occurred this year alone.

The Zest

ZestyAI has been keeping a close eye on the wildfires burning in the Western United States. Whether by evacuation or smoke, most of our employees have felt the impact firsthand.

Utilizing our vast wildfire data and artificial intelligence resources, we have estimated that as of September 18th, between $5.9Bn and $9.8Bn in losses have occurred this year alone.

What has made 2020 unique?

Two key aspects have made the 2020 Wildfire Season exceptional: the number of acres burned and the timing of the fires.

2018, which previously held the California record for acres burned at 1,975,086 has been eclipsed with months left in the seasons. More than 3.3 million acres have already been charred by wildfire this year in California alone, and more than 5 million in the Western US.

Fire season tends to start in September and peak in November. In August, a large scale lightning event occurred, triggering many of the California wildfires. Oregon, which typically has a shorter wildfire season has also seen early and widespread wildfires.

Analysis Methodology

Using ZestyAI’s comprehensive historical wildfire loss data, up-to-date wildfire perimeter locations for the 2020 season, residential and commercial property information, and fueled by ZestyAI’s AI-driven wildfire damage risk scores, the expected destruction and cost of the 2020 wildfire season so far was calculated for California, Oregon, and Washington.

To estimate the destruction and damages, ZestyAI identified every structure involved in the 2020 wildfire perimeters and their associated wildfire vulnerabilities. Using the historical relationship between the risk profile of the structure, asset value, and economic loss, ZestyAI was able to estimate the full economic loss of those events (including non-insured assets such as uninsured property, and non-insured economic cost). Actual information from CalFire on CZU and LNU incident was used to validate the methodology.

From our extensive historical loss data, a relationship between structural damage expected and the cost of wildfire events was developed based on local property and loss information and expanded to include additional considerations such as smoke damage, displacement costs, and construction.

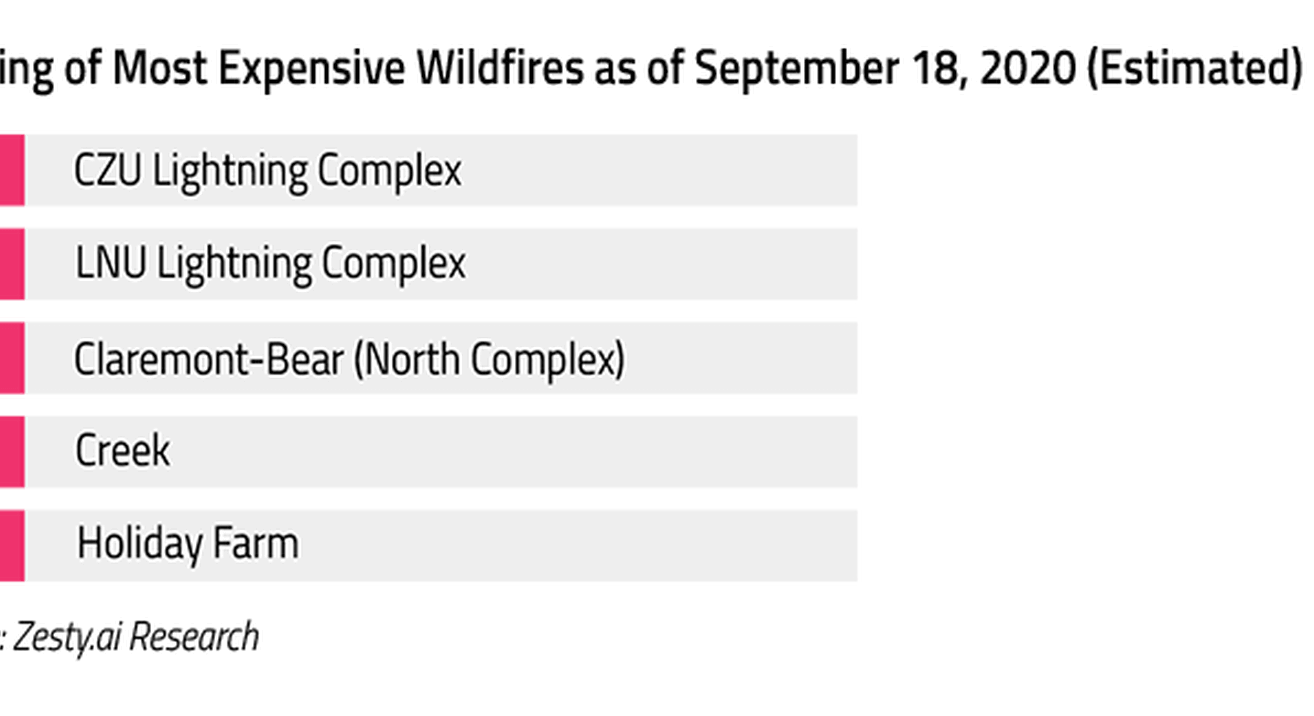

The 5 Most Destructive Fires So Far

Our estimates place the Claremont-Bear (North Complex) at the top of the list of most destructive in terms of number of properties lost. Four of these five wildfires occurred in California with the Alameda Drive fire occurring in Oregon.

The 5 Most Expensive Fires So Far

While the Claremont-Bear (North Complex) fire is estimated to have destroyed the most properties, the CZU Lightning Complex fire is currently estimated to be the most costly at up to $2.6B. That makes it responsible for ~27% of all total economic losses from fires in the 2020 season so far.

Putting Numbers on Destruction

By ZestyAI estimates, between $5.9Bn and $9.8Bn of economic losses have occurred in California, Oregon, and Washington so far this year. California, which also leads in acres burned (5M+) makes up the lion’s share at up to $7.9B.

It’s important to state that the fire season is not yet over. In much of the Western US, it could be just beginning. With a number of fires still active and the potential for more to start, these numbers are almost certain to rise between now and the end of the year.

Looking Forward

Multiple estimates place the 2018 wildfire season at around $15Bn in total losses. While exceptional in terms of total acres burned, the 2020 wildfire season has not yet reached that level of economic loss. Without any doubt, this will be one of the costliest years on record, and with months left in the season, the potential exists for this year to surpass 2018 if it continues at its current pace.

ZestyAI will continue to monitor this fire season. As in years past, new data continues to refine our models and analyses. Insurance professionals and media who would like more information about this analysis or about how artificial intelligence can help insurers protect themselves and their customers from wildfire should contact us.

Report: Severe Convective Storm Preview 2025

Get the insights to manage risk in 2025 before claims surge.

Severe convective storms (SCS)—including tornadoes, hail, and damaging wind events—resulted in $58 billion in insured losses across the U.S in 2024.

Insurers face a dual challenge: navigating the uncertainty of storm patterns while ensuring their portfolios remain resilient enough to absorb the financial strain from clustered, high-loss events.

Research with IBHS confirms that SCS damage accumulates over time, particularly affecting rooftops after multiple exposures to intense storm activity. As housing stock deteriorates, insurers must reassess their portfolios to ensure underwriting, rating, and loss cost controls align with their risk appetite and maintain premiums that accurately reflect evolving exposure.

Get ahead of rising storm risks with expert insights that help you strengthen underwriting, risk assessment, and claims management.

$2.15 Trillion in Property Value at Risk as Wildfire Exposure Expands Across the U.S.

ZestyAI Identifies 4.3 Million U.S. Homes with High Wildfire Risk.

A staggering $2.15 trillion worth of U.S. residential property is at high risk of wildfire damage, according to a new AI-powered analysis from ZestyAI, the leader in climate and property risk analytics. The study, which assessed 126 million properties nationwide, found that 4.3 million individual homes face heightened wildfire risk—far beyond traditionally recognized high-risk areas.

Using advanced AI models trained on over 2,000 historical wildfires, ZestyAI mapped wildfire exposure at the property level, integrating satellite and aerial imagery, topography, and structure-specific characteristics. While California leads the nation with $1.16 trillion in wildfire-exposed property, other states such as Colorado ($190.5 billion), Utah ($100.3 billion), and North Carolina ($71.2 billion) also face significant risk.

Wildfire Risk is a Nationwide Challenge

While the Western U.S. has historically seen the most severe wildfire activity, ZestyAI’s findings confirm that high-risk properties exist across the country. States like North Carolina (4.6% of homes at high risk), Kentucky (2.9%), Tennessee (2.3%), and even South Dakota (11.0%) are now seeing increased wildfire exposure.

As more homes and businesses are built in fire-prone landscapes, the Wildland-Urban Interface (WUI) continues to expand. This, combined with intensifying climate conditions, is driving higher insurance costs and growing availability concerns. Today, one in eight U.S. homeowners already lacks adequate insurance coverage, and that number is expected to rise.

AI Expands Insurance Access in High-Risk Areas

Attila Toth, Founder and CEO of ZestyAI said:

"Wildfires are threatening more properties than ever before, with billions of dollars in exposure even in areas many people don’t associate with fire risk. Yet, too many homeowners are finding themselves uninsured or underinsured just as these disasters become more frequent and severe. Insurers have traditionally relied on broad, regional models that don’t account for individual property characteristics."

"That means some homeowners are denied coverage even when their true risk is much lower than their neighbors'.’"

AI-driven risk analytics are reshaping the way insurers assess wildfire exposure. By providing granular, property-specific insights, we’re helping insurers make smarter underwriting decisions—keeping coverage available in high-risk areas while ensuring that homeowners who take mitigation steps are recognized.

Last year, our models helped insurers extend coverage to 511,000 properties that had previously struggled to secure insurance due to outdated risk models. In 2025, we expect that number to reach a million, ensuring that even in high-risk areas, responsible homeowners have access to protection when disaster strikes.

.png)

ZestyAI’s AI-Powered Hail and Wind Risk Models Continue Rapid Expansion with Approvals in Five States

Amid rising storm threats, regulatory approvals in Oklahoma, North Carolina, Louisiana, Wisconsin, and Arkansas bring AI-driven risk insights to millions of properties.

Property and climate risk analytics leader ZestyAI today announced regulatory approval of its Severe Convective Storm Suite in Oklahoma, North Carolina, Louisiana, Wisconsin, and Arkansas—covering more than 12 million residential and commercial properties.

Severe convective storms caused $58 billion in insured losses in 2024, marking the second-costliest year on record. A recent ZestyAI analysis revealed that in these five newly approved states, more than 2.1 million properties face a high risk of filing a hail claim—putting over $31 billion in potential roof replacement costs on the line.

Unlike traditional models, ZestyAI’s AI-driven risk models predict the likelihood and severity of claims at the individual property level by analyzing the interaction of local climatology with property-specific characteristics.

Built, tested, and validated on an extensive claims database, the models provide a granular, transparent understanding of risk—delivering the top risk factors for each property, and equipping insurers with the accuracy needed to improve underwriting, optimize pricing, and reduce preventable losses.

“Severe convective storms now cost insurers more than hurricanes, yet traditional underwriting tools don’t provide the precision needed to keep pace with rising losses,” said Bryan Rehor, Director of Regulatory Affairs at ZestyAI.

“These approvals reinforce the insurance industry’s shift toward data-driven, property-level risk assessment."

ZestyAI’s SCS models have now been thoroughly vetted and approved by regulators across 14 states—covering more than 44 million properties across the Midwest, Great Plains, and South.

.webp)

Lemonade Partners with ZestyAI to Elevate Underwriting Precision

See how Lemonade is leveraging ZestyAI’s advanced risk insights to strengthen coverage.

ZestyAI announced today that Lemonade, the digital insurance company powered by AI and social impact, has adopted the ZestyAI platform to further optimize underwriting for key catastrophe perils in the U.S., building on the company’s existing technology and underwriting operations.

ZestyAI’s predictive analytics platform leverages advanced AI models to analyze the interplay of climatology, geography, and the unique characteristics of each structure and roof, enabling precise and transparent property risk assessments.

By leveraging unique risk insights, Lemonade can make smarter catastrophe risk mitigation decisions. Additionally, ZestyAI’s proactive regulatory approach, with approvals in key states, simplifies compliance and enables Lemonade to implement these models faster.

“Since our launch, we've always been committed to using technology to create smarter, more accessible insurance products,” said Ori Hanani, Senior Vice President of Insurance at Lemonade.

“In leveraging ZestyAI’s advanced risk models, we're able to further support homeowners in securing comprehensive coverage for their most valuable assets, while also continuing to strengthen our underwriting capabilities as we continue to grow."

Attila Toth, Founder and CEO of ZestyAI, said:

Lemonade is a natural partner for ZestyAI.

“Their innovative approach to insurance and customer-centricity aligns perfectly with our commitment to provide actionable insights that drive smarter risk decisions.”

This partnership reflects a shared vision for addressing increasing climate risks and sets a new standard for resilience, efficiency, and innovation in the insurance industry.

Colorado FAIR Plan Taps ZestyAI to Expand Insurance Accessibility Amid Climate Risks

AI-driven risk models to improve wildfire, hail, and wind assessments while enhancing insurance availability and affordability in Colorado.

ZestyAI today announced a partnership with the Colorado FAIR Plan to expand insurance access for homeowners facing coverage challenges.

The partnership leverages ZestyAI’s AI-driven risk models—Z-FIRE™, Z-HAIL™, and Z-WIND™—to deliver property-specific risk assessments for wildfire, hail, and wind. These insights will support risk-based pricing and help the Colorado FAIR Plan guide homeowners on mitigation strategies.

“Our mission is to ensure every Coloradan has access to insurance that reflects their property’s actual risk, not outdated assumptions,” said Kelly Campbell, Executive Director of the Colorado FAIR Plan.

“ZestyAI’s models will help us bring greater fairness and resilience to the market while equipping homeowners with practical mitigation guidance.”

Over the next year, Colorado FAIR Plan expects to provide coverage to nearly 30,000 families previously classified as high-risk under traditional models.

By incorporating granular risk data, the plan can better align premiums with actual risk while offering homeowners actionable steps to protect their properties.

Those who invest in mitigation may also transition back to the standard insurance market over time.

Colorado regulators have prioritized risk-based pricing and transparency to stabilize the insurance market. Colorado Insurance Commissioner Michael Conway has led efforts to integrate mitigation into coverage decisions, aligning with the FAIR Plan’s adoption of ZestyAI’s AI-driven insights.

“This partnership ensures risk assessments reflect real property conditions—not just broad classifications—so homeowners can access both coverage and meaningful mitigation guidance,” said Bryan Rehor, Director of Regulatory Affairs at ZestyAI.

“Through AI-powered insights, we’re helping homeowners secure risk-aligned coverage options.”

ZestyAI’s risk platform integrates aerial imagery, historical building permits, geospatial data, and structural attributes to provide precise, property-level risk insights.

Insurers using ZestyAI’s models can assess key risk factors—including vegetation proximity, roof condition, and building materials—to inform underwriting, pricing, and mitigation recommendations to policyholders.

The collaboration builds on ZestyAI’s success with the California FAIR Plan, which expanded coverage for hundreds of thousands of homeowners in 2024.

ZestyAI Recognized as a Top Startup Employer by Forbes

We’re excited to share that, for the second year in a row, ZestyAI has been named one of America’s best startup employers by Forbes. This recognition highlights our commitment to fostering an exceptional workplace culture while fostering a healthier insurance market.

What It Means to Be a Top Startup Employer

Forbes, in partnership with research firms, evaluated over 20,000 U.S. startups based on three key factors: employer reputation, employee satisfaction, and business growth. Only 500 companies made the final cut, and we’re incredibly proud to be among them.

At ZestyAI, we believe that fostering a collaborative and supportive work environment isn’t just beneficial for our team—it’s essential to our mission. By enabling insurers to make more precise, data-driven decisions, we help drive resilience across communities, ultimately benefiting the homeowners and business owners they serve.

A Remote-First, People-First Culture

As a fully remote company, ZestyAI gives team members the flexibility to design a work-life balance that fits their needs. We go beyond traditional benefits by offering an unlimited time-off policy, which includes vacation and mental health days to support well-being and prevent burnout.

For team members across North America, our local hubs bring “Zesties” together for in-person events and networking, fostering connection and collaboration.

“Culture is not just a buzzword at ZestyAI—it’s the glue that holds our team together,” said Attila Toth, Founder and CEO of ZestyAI.

“Like a great sports team, we believe that the whole is greater than the sum of its parts. Our commitment to collaboration and well-being empowers us to deliver exceptional results.”

Industry Recognition

This honor joins a list of awards celebrating our work. ZestyAI has also been recognized by Inc. 5000 as one of America’s fastest-growing private companies, included in the Deloitte Technology Fast 500, and named to the CB Insights Insurtech 50. We have also received an AI Breakthrough Award for Machine Learning and a PropertyCasualty360 Insurance Luminary award for Risk Management Innovation.

Interested in joining us? Check out our careers page!

See How Insights Turn Into Decisions

ZestyAI transforms data into action. Get a demo to see how the same AI powering our reports helps carriers make faster, smarter, regulator-ready decisions.