Reports & Research

Explore proprietary research packed with data, insights, and real-world findings to help carriers make smarter decisions.

.png)

AI in Insurance: How to Stay Ahead of the Curve

Artificial intelligence is reshaping the P&C insurance industry, offering new ways to streamline underwriting, enhance risk management, and navigate evolving regulations.

But as AI adoption accelerates, insurers must ensure they’re using these technologies effectively—balancing innovation with compliance.

Our latest guide explores the most impactful AI applications in insurance, including:

- AI-powered underwriting and predictive analytics

- How regulators are shaping the future of AI in insurance

- Best practices for integrating AI while ensuring fairness and transparency

As AI-driven tools become the new standard, insurers who adapt early will gain a competitive edge.

Download our free guide to leverage these innovations while staying aligned with evolving regulations.

The Truth About Roof Age: 5 Critical Insights Every Insurer Should Know

For insurers, accurate roof age data is essential. Yet, self-reported information often falls short.

Our research shows that 1 in 5 homeowners underreport roof age by an average of 8 years. These discrepancies create hidden risks that can impact underwriting, pricing, and overall portfolio performance.

How can insurers get a more accurate picture?

AI-driven insights provide 97% nationwide coverage, combining verified roof age with real-time condition data for a more comprehensive risk assessment.

Download our latest research for a breakdown of five critical insights that every insurer should know about roof age.

Plus, get access to The Roof Age Advantage, an exclusive video that unveils how AI is setting a new standard for risk evaluation.

Now Streaming: Navigating California's Evolving Insurance Landscape

The California Department of Insurance (CDI) has introduced significant updates as part of its Sustainable Insurance Strategy. These new bulletins and draft regulations aim to accelerate regulatory approvals, embrace forward-looking models, and address critical reinsurance challenges.

But what do these changes mean for insurance carriers—and how can you prepare?

On January 29, 2025, we hosted a webinar, California’s Evolving Insurance Landscape: The Future of Insurance in the Golden State.

Designed for Legal & Compliance professionals, Product Managers, Underwriters, Actuaries, and Risk & Innovation leaders, the discussion featured expert insights from:

- Michael Peterson, Deputy Commissioner of Climate & Sustainability, California Department of Insurance

- Karen Collins, VP, Property & Environmental, APCIA

- Bryan Rehor, Head of Regulatory Affairs, ZestyAI

Missed the live event but want to gain actionable insights from industry leaders at the forefront of California’s insurance evolution? Watch on demand now!

Webinar: Regulatory Ready - How to Use AI Responsibly in Insurance

Gain a deeper understanding of the NAIC bulletin's principle-based approach to AI regulation and what it means for carriers.

Regulatory Ready: How to Use AI Responsibly in Insurance Under the NAIC Bulletin

AI innovation is revolutionizing the insurance industry, but with these advancements come new regulatory challenges. To ensure responsible use of AI in insurance, it’s essential to stay informed about the latest regulatory frameworks.

Join us on November 13 at 11 PT / 2 ET for an exclusive webinar where we’ll break down how to navigate AI regulations under the NAIC Model Bulletin.

In this session, led by

- Kevin Gaffney, Vermont’s Commissioner of Financial Regulation and Chair of the NAIC’s Innovation & Tech Committee

- Bryan Rehor, Director of Regulatory Strategy at ZestyAI

you'll gain critical insights on how to align AI usage with evolving regulatory expectations.

What You’ll Learn

This webinar will provide practical takeaways that can help insurance professionals understand and comply with the latest AI standards:

- NAIC Model Bulletin Overview: Understand the core principles behind the NAIC’s AI regulation framework.

- Ensuring AI Compliance: Learn how to ensure responsible AI usage according to NAIC standards.

- Preparing for Regulatory Oversight: Get ready for closer state-level inspections and regulatory scrutiny.

- Vendor & Partner Compliance: Ensure that your partners meet regulatory requirements for transparency and fairness.

- Interactive Q&A: Take advantage of the opportunity to ask our experts about the complex world of AI and insurance compliance.

Meet the Experts

Kevin Gaffney

Vermont Commissioner of Financial Regulation

As an expert in AI regulations and the NAIC’s Model Bulletin, Commissioner Gaffney will provide key insights into how insurance companies can effectively implement responsible AI practices. His experience in overseeing state-level financial regulation will offer attendees a unique perspective on aligning AI innovation with compliance.

Bryan Rehor

Director of Regulatory Strategy at ZestyAI

Bryan Rehor will offer practical advice on maintaining AI compliance while harnessing the full potential of AI innovation. His expertise lies in guiding insurers through regulatory demands, ensuring that AI practices meet industry standards while avoiding common pitfalls.

Why You Should Attend

This webinar is tailored for professionals in insurance, particularly those in Executive, Legal, Compliance, Product Management, Underwriting, Actuarial, Risk, and Innovation roles.

Whether you’re navigating the complexities of AI regulation or preparing for the next steps in compliance, this session will provide actionable insights to help you move forward confidently.

Bonus Content

By registering for the webinar, you’ll receive our interactive guide:

“When Innovation & Regulation Meet: What Insurers Need to Know About AI and Regulatory Compliance.”

This resource will deepen your understanding of how to stay compliant while leveraging the power of AI in your insurance operations.

Don’t miss out!

Register for the webinar and ensure your spot in this exclusive event.

.png)

The State of the Industry: AI Adoption in Climate Risk Management

A survey of insurance professionals highlights AI models gaining traction, key insurer priorities, and the impact of transparency and regulatory concerns.

Facing Unprecedented Climate Challenges

The insurance industry is facing unprecedented challenges as natural catastrophic events like convective storms and wildfires become more frequent and severe. Traditional risk models, which often rely on broad territory-based segmentation, are struggling to keep up with these dynamic environmental threats. This has led to significant financial losses for insurers, who are now seeking more accurate and proactive methods to predict and manage climate risk.

AI Adoption in Property and Casualty Insurance

To shed light on the adoption of these cutting-edge techniques, ZestyAI conducted a survey of over 200 executives in the Property and Casualty (P&C) insurance sector. The survey reveals which AI-based models are gaining traction, what features insurers prioritize, and how transparency and regulatory concerns are shaping the industry. It also highlights the specific risks that are top of mind for carriers today.

AI Transforming Risk Assessment Models

The industry is turning to AI-based risk assessment models that offer a new level of precision. Companies like ZestyAI are leading the charge, providing tools that enable insurers to assess risk on a property-by-property basis, considering both individual property features and their interaction with surrounding environmental factors. These advanced models are transforming the way insurers underwrite policies, optimize portfolios, and align coverage with actual needs.

Dive deeper into our findings and explore the full report by clicking below.

Access the Report

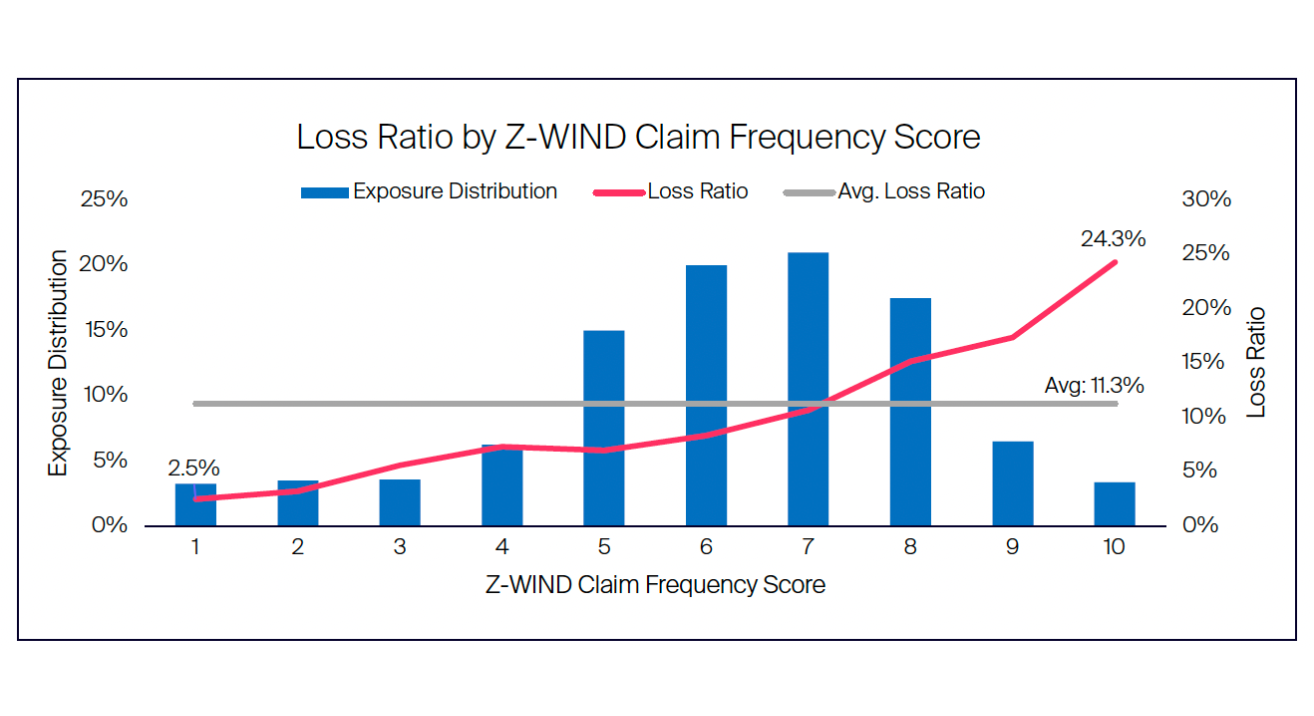

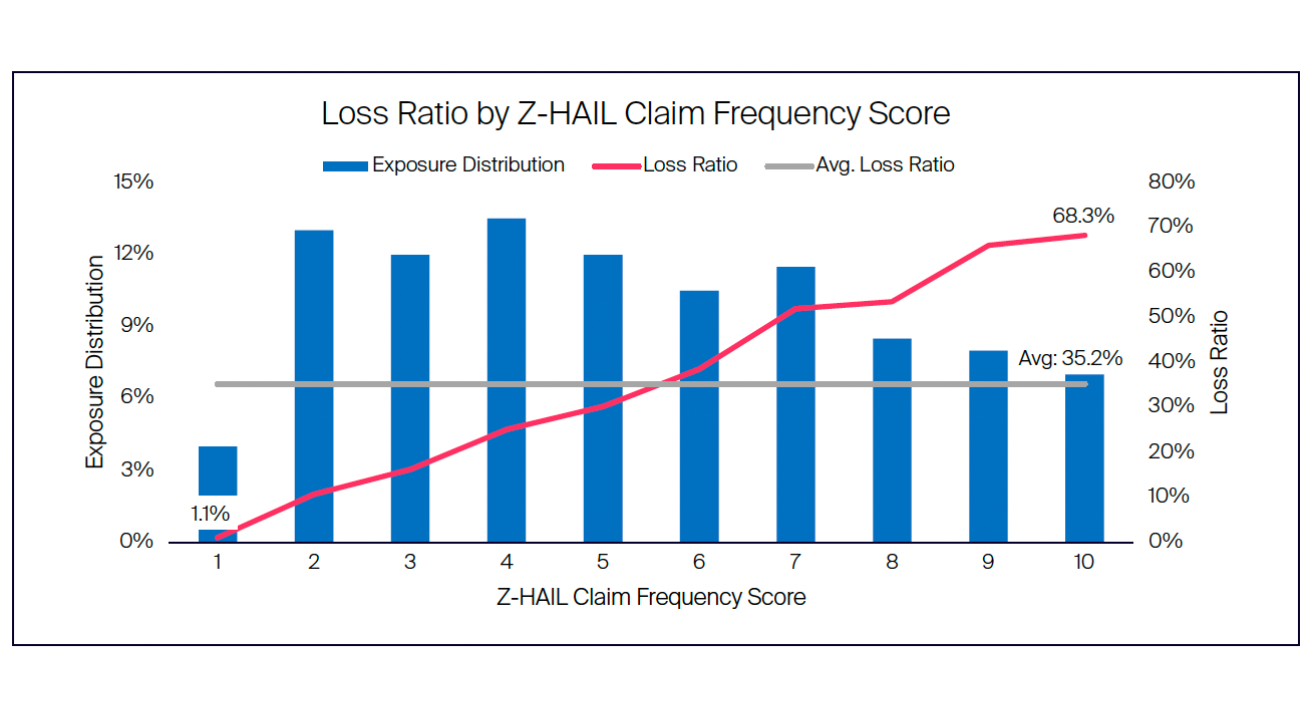

Case Study: Adapting to Escalating Severe Convective Storm Risk

Insights from a 5-year retrospective on ZestyAI’s models in action

The Rising Threat of Severe Convective Storms

The past few decades have seen a dramatic rise in the frequency and intensity of severe convective storms, resulting in significant financial repercussions for the insurance industry. In the last year alone, insured losses from severe convective storms reached an astounding $60 billion, marking an average annual growth rate of over 11% over the past twenty years. This alarming trend means a new approach is needed to manage and mitigate the escalating risks associated with severe weather events.

In the last year alone, insured losses from severe convective storms reached an astounding $60B, marking an average annual growth rate of over 11% over the past twenty years.

The traditional methods of risk assessment and management are no longer sufficient to cope with the increasing unpredictability and severity of these weather events. As the risk evolves, so must the solutions. Changing risks call for innovative solutions that leverage advanced technology and data analytics to enhance the accuracy and effectiveness of risk modeling.

A New Approach

ZestyAI’s Z-HAIL and Z-WIND models are specifically designed to address the challenges posed by severe convective storms. In a new retroactive case study, we explore the performance of these models on a carrier’s book of business over the prior five years, highlighting their effectiveness in delivering comprehensive coverage and precise risk segmentation.

Key findings from the case study include:

Comprehensive Coverage with High Accuracy

One of the standout results from the case study is the exceptional hit rate of 99.7% achieved by Z-HAIL and Z-WIND. This shows the models were able to accurately identify and assess the risk of severe convective storms for nearly all the properties in the carrier's portfolio.

Strong Risk Segmentation

The models demonstrated remarkable capability in risk segmentation, with Z-HAIL generating a lift of 62X and Z-WIND achieving a lift of 9.7X. This means that the models were able to effectively differentiate between high-risk and low-risk properties, even within small geographic areas such as a single zip code. Accurate risk segmentation allows insurers to tailor their policies and pricing strategies more precisely, leading to better management of their risk exposure.

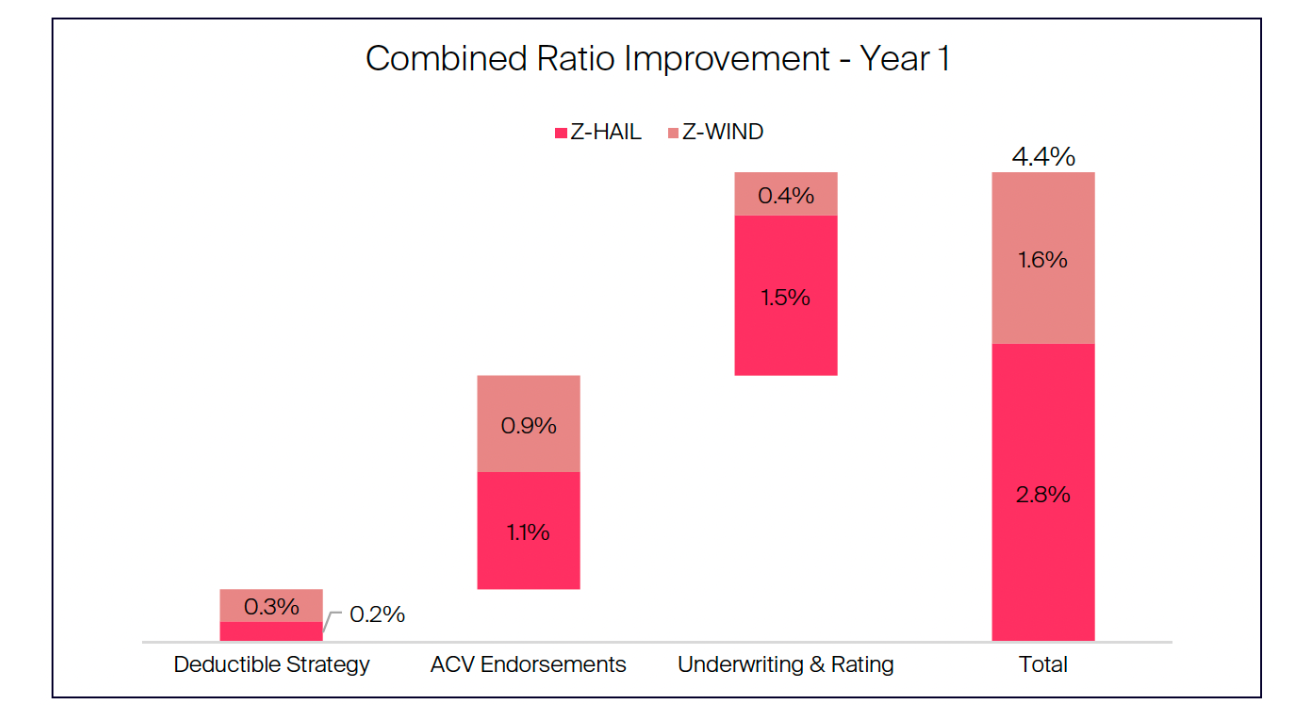

Improved Combined Ratio

Implementing Z-HAIL and Z-WIND would significantly enhance a carrier’s combined ratio, calculated to be approximately 4 points in the first year. This improvement can be attributed to the models’ ability to optimize underwriting, rating, and the application of deductibles and Actual Cash Value (ACV) endorsement strategies. By accurately assessing the risk and applying appropriate measures, insurers can reduce their loss ratios and improve overall profitability.

The Need for Innovative Solutions

As severe convective storms continue to pose significant challenges to the insurance industry, adopting innovative solutions like ZestyAI’s severe convective storm models can help insurers better manage this escalating risk.

These models provide comprehensive coverage, accurate risk segmentation, and improved financial performance. By embracing advanced technology and data-driven analytics, insurers can navigate the complexities of severe weather events and safeguard their portfolios against future losses.

To learn more about the detailed findings and benefits

Download the full case study.

Now Streaming: LA Fires in Focus – What Insurers Need to Know

What Worked, What Didn’t, and What’s Next for Insurers

With insured losses projected to exceed $30 billion, the recent Los Angeles wildfires rank among the costliest in U.S. history—reshaping how insurers think about risk, resilience, and readiness.

Watch the Full Webinar → LA Fires in Focus: What Insurers Need to Know

In this on-demand webinar, experts from the Insurance Institute for Business & Home Safety (IBHS), the Western Fire Chiefs Association, Cal Poly’s WUI Fire Institute, and ZestyAI unpack what really happened—from frontline response to lab-based research and model performance—and share critical strategies insurers can use to prepare for what’s next.

Watch this session if you’re a Product Managers, Underwriters, Actuaries, and Risk & Innovation leaders looking to make informed decisions in an increasingly volatile wildfire landscape.

What You’ll Learn

- Key takeaways from the Los Angeles wildfires

- Research on structure-to-structure fire spread and resilience factors

- How wildfire risk models performed—what we got right (and wrong)

- Practical strategies to reduce exposure and strengthen resilience

Meet the Experts

- Anne Cope, Chief Engineer, IBHS

- Bob Roper, CEO, Western Fire Chiefs Association

- Frank Frievalt, Director, WUI Fire Institute at Cal Poly

- Kumar Duhvur, Co-Founder & CPO, ZestyAI

Connecticut Insurance Department Green Lights AI-Powered Roof Quality Solution

Insurers can leverage AI-driven, property-specific roof condition insights for more accurate underwriting and rating decisions across the state

ZestyAI today announced that the Connecticut Insurance Department (CID) has formally approved its Roof Quality solution for use in residential property underwriting.

CID conducted a comprehensive third-party actuarial review of ZestyAI’s model, evaluating methodology, data integrity, and regulatory compliance against its rigorous standards.

What CID’s Approval Means for Carriers

Part of Z-PROPERTY™ , the Roof Quality model enables insurers to assess and price roof risk with unmatched accuracy.

By combining 3D property analysis, high-resolution aerial imagery, and AI trained on extensive real-world data, the platform replaces subjective or incomplete assessments with objective, property-specific intelligence.

The model classifies roofs into five standardized condition levels, helping insurers assess property risk with greater precision. It distinguishes between surface-level wear and structural issues, flagging meaningful signs of deterioration such as missing shingles, tarps, or water pooling.

Bryan Rehor, Director of Regulatory Affairs at ZestyAI, said:

“Roof condition is one of the strongest predictors of loss, yet historically one of the hardest to assess without costly inspections. This approval affirms the accuracy, fairness, and transparency of our approach and reflects our broader commitment to aligning innovation with consumer protection.”

How ZestyAI’s Roof Quality Model Improves Risk Assessment

ZestyAI maintains active engagement with the National Association of Insurance Commissioners (NAIC) and state-level departments to ensure its models meet evolving standards for fairness, transparency, and consumer protection.

By proactively filing through in-house Rating and Advisory Organizations, ZestyAI ensures its models meet the strictest regulatory standards before reaching the market.

ZestyAI’s models are trusted by regulators and insurers to assess risk in the nation’s most climate-exposed regions with Z-FIRE, ZestyAI’s wildfire risk model, approved by regulators in all western states. Its Severe Convective Storm suite is approved in 16 states across the Midwest, Great Plains, and South.

Farmers and Mechanics Mutual Insurance Company of West Virginia Adopts ZestyAI to Strengthen Underwriting and Risk-Based Pricing

AI-powered property risk insights support greater rating precision, lower inspection costs, and smarter underwriting decisions across West Virginia.

ZestyAI today announced a new partnership with Farmers and Mechanics Mutual Insurance Company of West Virginia (FMIWV) to strengthen underwriting accuracy and improve risk-based pricing.

Why Accurate Roof Data Matters More Than Ever

Roof claims are the leading driver of insurance losses, yet many carriers still depend on self-reported data, which can be unreliable, or physical inspections, which are costly and hard to scale. Recent research shows that 15% of roofs are at least eight years older than reported, highlighting the need for more reliable, data-driven alternatives.

To address long-standing challenges in accessing reliable property insights, FMIWV selected Z-PROPERTY™.

Why FMIWV Chose Z-PROPERTY

Dan Otto, Senior Vice President and Chief Financial Officer at FMIWV, said:

"After evaluating several options in recent years, we chose ZestyAI based on their strong coverage and ease of implementation. Getting started using the technology was easy. We’re particularly focused on using their property insights to provide additional underwriting information for new business and renewals.”

ZestyAI’s advanced insights help FMIWV:

- Identify high-risk properties early to prioritize mitigation and prevent losses

- Enhance risk selection and pricing precision with objective, property-level data

- Reduce inspection costs and turnaround time by minimizing the need for on-site assessments

- Streamline straight-through processing for low-risk properties to improve efficiency and speed to bind

- Reduce premium leakage by aligning pricing with actual exposure

“FMIWV is showing how regional carriers can lead with data-driven underwriting that improves operations and elevates the customer experience,” said Attila Toth, Founder and CEO of ZestyAI.

“By grounding decisions in reliable, property-level data, they’re improving efficiency, reducing risk, and raising the bar for underwriting and rating precision.”

Wildfire Risk Across the Nation

We’ve created a visual guide to where wildfire risk is rising—and where opportunities for mitigation exist.

Wildfire Risk Is Rising Nationwide

Wildfire seasons are getting longer, more destructive, and harder to predict—and they’re no longer just a Western U.S. concern. From the Southeast to the Midwest, wildfire risk is emerging in places many insurers haven’t traditionally watched.

What the Latest Data Reveals About Wildfire Exposure

Drawing from the latest national datasets and insights from ZestyAI’s Z-FIRE™ model, this visual guide to wildfire risk in the U.S. shows:

- New wildfire hotspots: Discover where risk is rising fastest.

- Mitigation gaps: Learn how a lack of defensible space is putting thousands of homes in danger across the country.

- Top risk drivers: See how features like overhanging trees and wooden roofs are fueling destruction in high-risk areas.

BONUS: You’ll also get access to our latest online event with IBHS and Western Fire Chiefs Association, The LA Fires in Focus: What Worked, What Didn’t, What’s Next for Insurers.

ZestyAI Product Updates: Smarter Models, Faster Workflows, and Richer Imagery

At ZestyAI, we’re continually enhancing our platform to help insurers better understand property risk, strengthen underwriting precision, and streamline operations. Over the last few months, our team has launched a series of updates that make our AI-powered solutions even more powerful and accessible.

From improvements in roof geometry and manufactured home modeling to expanded wildfire data on home hardening and structural vulnerability, plus faster APIs and faster APIs, these updates reflect our deep commitment to product excellence and customer success.

Smarter Risk Modeling for Manufactured Homes

Updated Manufactured Home Model in Z-PROPERTY

We’ve released an upgraded model for manufactured homes within Z-PROPERTY, trained on a broader set of imagery sources to improve data coverage and model accuracy.

This new version reduces the false positive rate, giving carriers greater confidence when evaluating mobile home risk—a critical upgrade for lines of business that rely on nuanced property insights.

Better Roof Geometry Analysis with the Roof Facet Model

Enhanced Accuracy and Speed in Roof Modeling

As part of our Digital Roof product, the Roof Facet model has been refined to deliver sharper roof geometry insights with faster processing times. This enhancement is especially valuable for customers scoring large portfolios, improving both speed and data quality.

Expanded Wildfire Risk Data Coverage

Compliance Pre-Fill Now Covers 99%+ of Wildfire Properties

We’ve expanded our Compliance Pre-Fill solution to support all wildfire-prone states, with property-level coverage now exceeding 99%. New on-demand access to critical wildfire mitigation features—including enclosed eaves, six-inch vertical clearance for siding, and noncombustible fencing—allows underwriters and compliance teams to make more accurate decisions with current data and zero added latency.

3D That Tells the Whole Story

Access to Richer 3D and Historical Imagery

ZestyAI now provides access to a broader and deeper catalog of high-resolution and historical imagery, powered by best-in-class sources of imagery. These enhancements improve underwriting workflows and allow insurers to “time travel” and evaluate how a property’s condition has changed over time.

This capability is especially valuable in regulatory environments that require proof of property degradation before policy changes are made. Historical imagery also gives underwriters a fuller view of prior conditions, providing context for past underwriting decisions.

Performance Gains Across All APIs

Reduced Latency and Improved API Response Times

We’ve optimized our APIs to significantly reduce latency, improving the speed and reliability of data delivery across all ZestyAI products. Whether batch scoring, running real-time underwriting, or executing renewal workflows, you’ll experience faster performance and greater efficiency—saving valuable time across your organization.

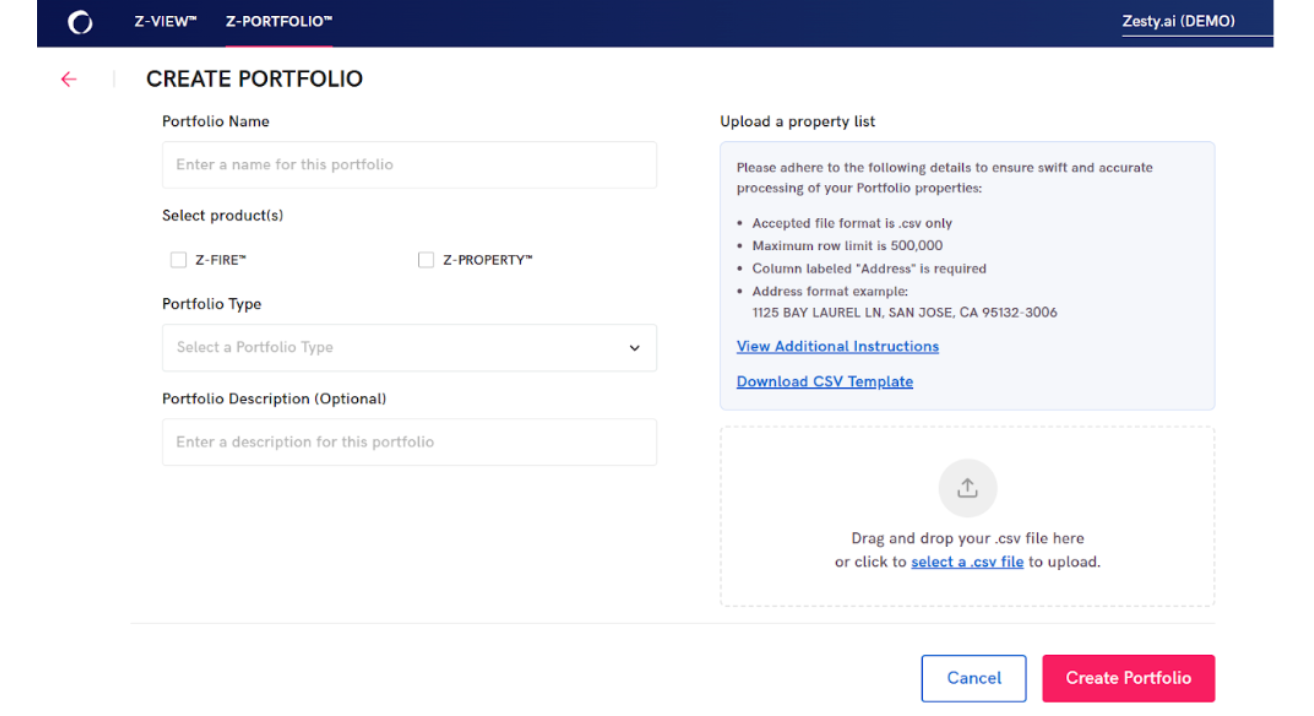

A New and Improved Upload Experience in Z-PORTFOLIO

Redesigned Upload Page for Streamlined Workflow

We’ve redesigned the Z-PORTFOLIO upload experience to make portfolio submissions more intuitive and efficient. Instructions and templates are now centralized in one place, and users can specify the purpose of the upload—such as renewal or dislocation analysis—to unlock deeper insights into usage patterns. This update enhances the self-service experience and helps customers extract maximum value from portfolio analyses.

Driving Continuous Innovation in Insurance Risk Intelligence

These product updates are more than just technical enhancements; they’re part of a larger mission to transform property risk assessment through AI. By improving model precision, reducing friction in workflows, and delivering richer, more current data, we’re helping insurers stay ahead of emerging risks and changing market demands.

If you’d like to learn more about any of these updates or request a demo, reach out to your Customer Success Manager or contact us below.

Why Non-Weather Water Losses Are Quietly Eroding Profitability

New research reveals how insurers can rethink their strategy for the 4th costliest peril in homeowners insurance

The Silent Peril Reshaping Homeowners Insurance

Non-weather water damage rarely makes headlines, but it’s quietly eroding profitability across the country.

It is now the fourth costliest peril in homeowners insurance, and claim severity has increased 80% in the last decade—a trend that’s accelerating even as frequency remains relatively flat.

Traditional risk models struggle to capture the early warning signs behind these losses, leading to mispriced policies, undetected exposure, and rising volatility for carriers.

Want the full analysis? Download the complete “Winning the Fight Against Non-Weather Water Losses” guide.

Why Loss Severity Keeps Rising

Aging homes and overlooked system failures

Many of the most expensive losses stem from aging plumbing, deteriorating materials, and slow-burn failures that often go undetected until damage is significant.

Frequency is flat—severity is not

Loss patterns suggest that while the number of events hasn’t surged, the financial impact of each event has—a signal that traditional models are not capturing the right property-level predictors.

The Property Features Most Predictive of Water Losses

The overlooked attributes that traditional models miss

Standard territory- or age-based assessments often ignore the property-specific details that meaningfully influence water loss risk, including:

- supply line material and age

- plumbing configuration

- occupancy patterns

- system maintenance and upgrades

- moisture exposure and prior loss indicators

These factors vary widely between neighboring homes—yet most models treat them as identical.

Where Traditional Underwriting Falls Short

ZIP-code and age-based proxies mask true risk

Legacy approaches rely heavily on broad territory-level assumptions that overlook structural vulnerabilities and system conditions.

Limited visibility creates mispriced policies

Without property-level insight, high-risk homes are often underpriced while lower-risk homes subsidize them—driving loss ratio volatility over time.

Get deeper insights on the drivers of water loss severity in our full guide → “Winning the Fight Against Non-Weather Water Losses”

How AI and Property-Level Data Are Changing the Landscape

AI models trained on real-world claims data can identify early signals of potential water loss by analyzing the interaction between:

- plumbing systems

- property attributes

- historical patterns

- material degradation

- repair history

This enables carriers to segment risk accurately, adjust pricing, and reduce preventable losses—long before small issues turn into major claims.

What Homeowners Actually Understand About Water Risk

Misconceptions around coverage and prevention

ZestyAI’s research shows that many policyholders:

- misunderstand what is and isn’t covered

- underestimate how much damage water can cause

- rarely take preventive actions unless prompted

This disconnect creates an opportunity for carriers to strengthen education, mitigation, and customer engagement.

Steps Carriers Can Take Today

Improve segmentation and rating accuracy

Property-level signals enable more precise risk tiers and more stable long-term portfolios.

Strengthen mitigation and reduce loss severity

Insights help identify which homes are at elevated risk and where targeted mitigation can reduce exposure.

Enhance underwriting workflows with explainable insights

Transparent, explainable AI helps underwriters understand the key drivers behind elevated risk—supporting both decision-making and regulatory review.

Get the Full Guide

Our new research paper, Winning the Fight Against Non-Weather Water Losses, breaks down the trends reshaping this growing peril—and the strategies carriers can use to get ahead of it.

Access the Guide

See How Insights Turn Into Decisions

ZestyAI transforms data into action. Get a demo to see how the same AI powering our reports helps carriers make faster, smarter, regulator-ready decisions.