Reports & Research

Explore proprietary research packed with data, insights, and real-world findings to help carriers make smarter decisions.

.png)

What Winter Storm Fern Reveals about Interior Water Losses and Systemic Risk

ZestyAI Product Insights

Winter Storm Fern has evolved into a historic catastrophe for the U.S. insurance industry. Between January 23-27, 2026, the storm shattered records by placing over 230 million Americans under severe winter alerts, with a death toll of 85 as of February 3rd.

Preliminary industry estimates place insured losses at $6.7 billion, potentially making Fern the third-costliest U.S. winter storm on record, trailing Elliott (2022) and Uri (2021). The crisis is far from over. The National Weather Service warns of a "historic duration" of extreme cold, with temperatures 15 to 25 degrees below average, that continues to hamper mitigation efforts.

For carriers, Fern is a complex, multi-peril challenge. Claims teams are navigating a surge of freeze-related losses, ice-driven structural damage, and widespread business interruptions across 34 states.

To understand the stakes, one needs to look no further than February 2021, when Winter Storm Uri brought Texas to its knees and generated over $11 billion in insured losses from a single state. Fern’s footprint is broader, and its secondary effects are still unfolding.

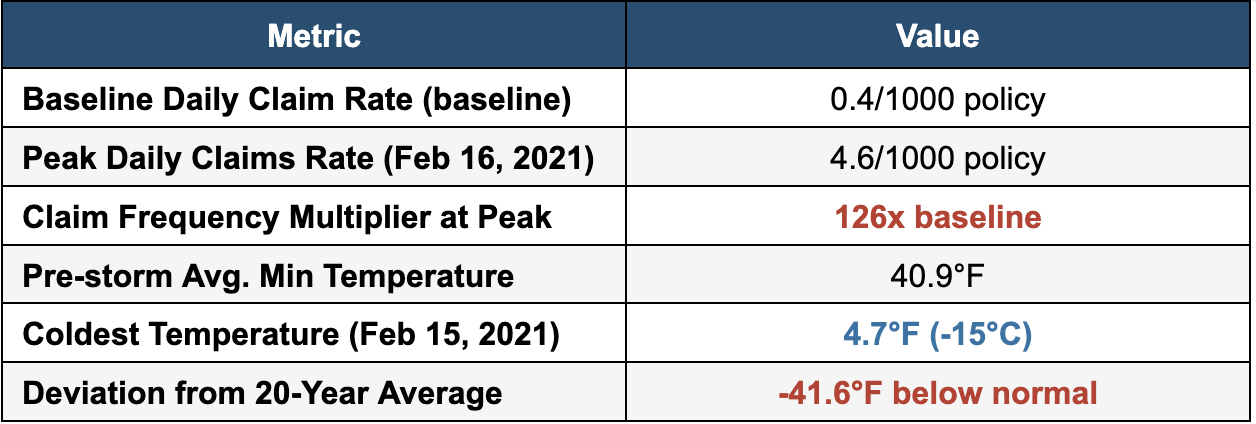

The Cold Hard Numbers from Storm Uri: Why Claims Explode Below 5°F

Our analysis of the 2021 Storm Uri reveals a striking relationship between temperature deviation and claim frequency for the non-weather water and freeze perils. Using data from multiple carriers, we tracked daily claim rates against minimum temperatures: before, during, and after the storm window (February 11-20, 2021).

The results show how rapidly falling temperatures can transform a routine winter pattern into a systemic loss event, allowing us to monitor the market’s response in real-time as conditions deteriorated, peaked, and normalized.

The results are dramatic:

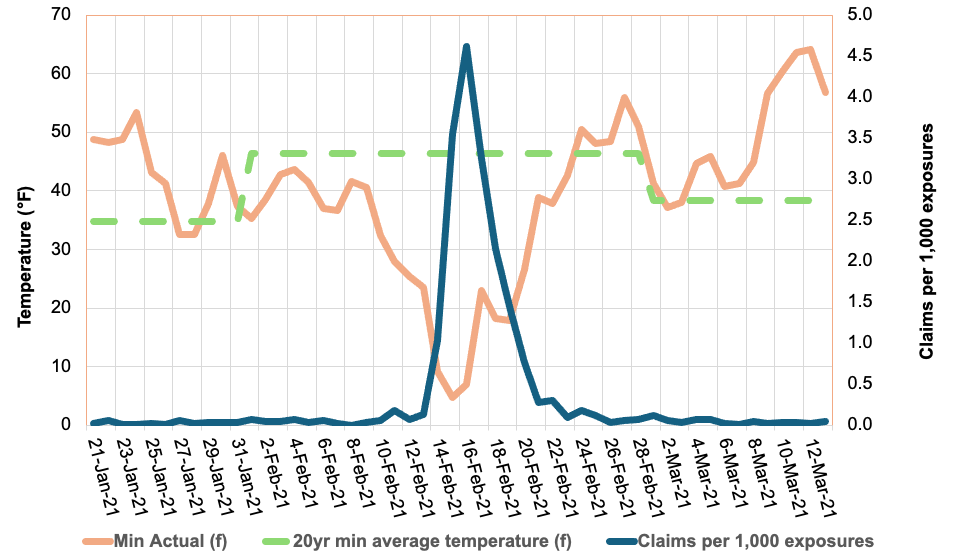

Figure 1: Daily claim rates (blue line) surged 126X above the baseline in a temporal spike as temperatures (orange line) plunged below the 20-year average (dashed green line) during Winter Storm Uri.

The chart reveals a clear inverse relationship: as minimum temperatures dropped from the mid-40s°F to below 5°F, daily claim rates didn’t just rise, they increased 126X, from a baseline of 0.04% to 0.46% at the peak. This dramatic surge underscores the significant consequences of extreme cold events on insurance liability.

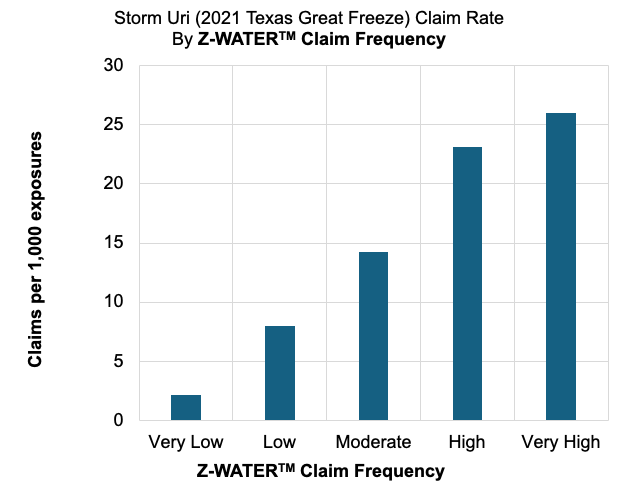

Figure 2: ZestyAI’s Z-WATER™ demonstrated an 11X increase in claim frequency between ‘Very High’ and ‘Very Low’ risk tiers during Winter Storm Uri

We used ZestyAI’s Z-WATER™ to segment the property-specific non-weather water risk across the 10-day storm window. Z-WATER™ is a risk model that accounts for how plumbing design, local climate, and infrastructure reliability interact to drive non-weather water and freeze losses. By capturing real-world dynamics, such as temperature swings that stress pipes and electrical grid failures that amplify claims, the model delivers a scientifically grounded view of property-level risk.

The results were definitive: properties that Z-WATER™ scored as ‘Very High’ risk filed 26 claims per 1,000, compared to just 2.2 claims per 1,000 for those scored as ‘Very Low’, an 11X increase in claim frequency.

This accurate segmentation reveals a clear path to managing volatility. Z-WATER™ provides a deep understanding of a home’s resilience across the full spectrum of loss mechanisms, from everyday plumbing failures to expensive outlier events like Storms Uri and Fern. By enabling precise intra-territory risk splitting, the model allows carriers to price and underwrite more reliably, ensuring premiums reflect the true risk profile while protecting the portfolio against systemic losses.

The January 2026 Storm: History Rhyming?

While we can already see the immediate impact of Winter Storm Fern, the primary difference between Fern and Winter Storm Uri is the duration of the freezing event itself, rather than any changes in how quickly policyholders are filing their claims.

As shown in Figure 1, NWW claims rise rapidly as temperatures fall and taper off quickly once conditions normalize. The risk in prolonged cold events lies in how long properties stay below the Plumbing Design Temperature; the longer the freeze, the greater the likelihood of systemic plumbing failure.

During Winter Storm Uri, extended sub-freezing conditions significantly increased the number of days in which vulnerable properties were exposed to frozen pipe failures, driving aggregate losses to historic levels. Fern is now exhibiting a similar duration profile, with sub-freezing conditions persisting for up to 10 consecutive days across parts of the Northeast. The National Weather Service has warned this “could be the longest duration of cold in several decades,” raising the likelihood of elevated losses even if individual claims remain tightly clustered in time.

For carriers, the warning signs are already flashing:

- The Power Failure Multiplier: During the storm's peak, over 1 million customers lost power. In the South, where homes lack the heavy thermal insulation of northern properties, a power outage is the primary driver of catastrophic pipe bursts. Without active heating, a property can reach the "burst threshold" within hours.

- The $30,000 Claim Severity Benchmark: Recent State Farm data underscores the high stakes of these events. Winter water damage claims totaled over $628 million, with the average claim payment now exceeding $30,000. For carriers, this high per-claim severity means even a moderate frequency surge can quickly erode Q1 margins.

- Regional Fragility in the South: While the initial assessments are still surfacing, early industry estimates for privately insured losses from Winter Storm Fern puts the damage at $4 billion to $7 billion. With Texas and Tennessee identified as the hardest-hit states, carriers are facing a "Uri-style" scenario in which infrastructure wasn't designed for a 10-day deep freeze.

From Reactive to Predictive: Solving the $6.7 Billion Freeze Risk Equation

The 2021 Texas freeze taught us that traditional approaches to freeze risk are highly insufficient. Many properties that experienced burst pipes were in areas that rarely see extended freezing temperatures, meaning they lacked adequate winterization.

This is where predictive analytics becomes essential. By modelling the interaction between property-level vulnerabilities and local temperature thresholds, carriers can better identify which properties are most vulnerable to freeze events before the damage actually occurs.

Key Risk Drivers Identified in Our Latest Analysis:

- The Design Mismatch: The greatest risk isn't just the cold; it's the sudden change in temperature. Properties in states like Texas or Tennessee face a higher risk because they are built to release heat, not trap it. They lack the heavy insulation and deep-buried pipes needed to survive a 10-day freeze.

- The Power Grid Vulnerability: Our analysis shows that areas prone to power outages face a compounded risk. In the South, a home’s primary defense is its heating system so when the power fails and the heater stops, the "burst threshold" can be reached in just a few hours.

- Building Vulnerabilities: Our analysis shows that older homes and properties with plumbing routed through exterior walls are disproportionately represented among $30,000 non-weather water losses.

The Bottom Line for Carriers

The 2021 Texas freeze was a pivotal moment for the industry, generating more than 500,000 claims and $11.2 billion in insured losses in a single state. Today, Winter Storm Fern represents an even broader systemic threat, with weather alerts impacting 230 million people across more than 30 states.

While the final tally for Fern is still developing, the data is already clear: temperature shocks drive claims at exponential rates. With early industry assessments estimating privately insured losses between $4 billion and $7 billion, it is evident that the prolonged duration and geographic anomaly of extreme weather events are the primary drivers of this volatility.

For carriers looking to protect their Q1 margins, predictive analytics are no longer a luxury; they are a requirement. By analyzing property-level characteristics, regional vulnerabilities, and historical temperature deviations, you can move from reactive claims handling to proactive risk management.

The question isn't whether another major freeze will occur, but whether your portfolio is prepared for the next 126-fold surge.

Learn More About Z-WATER

ZestyAI’s Z-WATER™ provides the industry’s most granular view of interior water risk, helping carriers accurately and reliably assess properties in areas prone to temperature shock events. By analyzing detailed property-level characteristics alongside historical weather patterns and regional risk factors, our advanced models predict the likelihood of Non-Weather Water (NWW) and freeze claims as well as their associated severity. This deeper level of analysis empowers carriers to make smarter pricing decisions before the next major storm hits.

Methodology: Analysis based on aggregated claims from multiple Texas carriers during Winter Storm Uri (February 2021). Temperature data reflects mean daily minimums across the exposure footprint, weighted by ZIP Code to account for geographic density. The claim/exposure ratio was calculated by dividing daily claims by the average policy-day exposure.

-----------------------------------------------------------------

1CNN Weather, "More than 230 million people under alerts for potential ice, heavy snow and extreme cold," January 2026. [link]

2Fox News, "Noem coordinates with Mississippi officials as state recovers from deadly winter storm," January 2026. [link]

3Insurance Innovation Reporter, “KCC Estimates $6.7 Billion in Insured Losses from Winter Storm Fern,“ February 2026 [link]

4Texas Department of Insurance, "Insured Losses Resulting from the February 2021 Texas Winter Weather Event," March 2022. [link]

5Fox Business, “More than 1 million Americans lose power as monster winter storm sweeps across the US,” January 2025 [link]

6Carrier Management, “Frozen Pipes Lead to $628M in Losses for State Farm,” January, 2026 [link]

7 Barrons, “Winter Storm Fern Packed a Wallop. Now the Cost Estimates Are Rolling In.,“ February 2026 [link]

Nearly $1 Trillion in California Homes Labeled “Low Risk” Despite Elevated Wildfire Danger

Wildfire risk in the United States is no longer confined to the edges of forests or traditionally high-risk zones. New analysis using ZestyAI’s property-level wildfire models shows that millions of homes classified as low or no wildfire risk under federal assessments face elevated wildfire danger when evaluated at the property level.

This analysis was recently featured in Vox, which examined how wildfire behavior is evolving — and why broad, backward-looking risk maps are increasingly misaligned with how fires spread today.

👉 Read the full article on Vox → https://www.vox.com/climate/476932/california-wildfire-los-angeles-risk-ai-housing-climate

Wildfire risk is closer — and more granular — than most maps show

Many homes damaged or destroyed in the 2025 Los Angeles wildfires were still classified as “low risk” under federal wildfire assessments. ZestyAI’s property-level analysis provides a different perspective.

By evaluating individual structures — including vegetation proximity, defensible space, building characteristics, and neighborhood-level fire dynamics — ZestyAI identified more than 3,000 properties worth approximately $2.4 billion in areas impacted by the Palisades and Eaton fires that showed elevated wildfire risk despite being classified as low or no risk under FEMA’s census-level assessments.

Across California, the classification gap is even broader. Approximately 1.2 million properties, representing roughly $940 billion in residential property value, are designated as low or no wildfire risk under federal maps, despite AI-driven property-level models indicating elevated wildfire danger.

Why census-level wildfire maps fall short

Wildfires do not spread evenly across census tracts or counties. Ember-driven ignition, structure-to-structure spread, wind conditions, and localized vegetation patterns create uneven outcomes, where one home survives and the next is destroyed.

Federal wildfire assessments are designed to provide a baseline view of community-level risk. FEMA has noted that its National Risk Index is not intended to serve as a property-specific risk assessment. When risk is evaluated at the individual property level, meaningful differences emerge that aggregated maps are not designed to capture.

What more granular wildfire risk intelligence enables

More detailed wildfire risk data can support:

- Targeted mitigation efforts at the property and neighborhood level

- More informed rebuilding and land-use decisions

- Clearer, more defensible underwriting and portfolio strategies

- Improved dialogue between insurers, regulators, and communities

A shift in how wildfire risk is understood

Wildfire risk is evolving faster than the systems built to measure it. Homes are no longer just adjacent to wildfire hazards; they increasingly influence how fires ignite, spread, and intensify, even in dense urban environments.

Property-level risk intelligence does not remove hard decisions. But without it, those decisions are made using an incomplete picture of where wildfire risk truly exists.

Read the full Vox article here.

The Roof Age Blind Spot in P&C Insurance

Roof age is a powerful predictors of property risk, yet insurers continue to rely on self-reported data that is often wrong. Our analysis uncovers just how costly that blind spot can be.

In property insurance, roof age is one of the most critical factors in assessing risk. Yet too often, carriers rely on self-reported or agent-supplied data that is incomplete or inaccurate.

ZestyAI’s recent analysis of 500,000+ properties revealed widespread discrepancies in reported roof age. The result? Mispriced policies, unexpected losses, and operational inefficiencies that impact the bottom line.

As climate volatility grows and reinsurance pressure intensifies, overlooking the true condition and age of a home’s largest, most exposed surface is a risk no carrier can afford.

What’s Inside

- Uncover the biggest myths and blind spots in roof age records.

- Understand why traditional data sources, like claims systems and permits, fall short in providing accurate roof age.

- Learn how a multi-source verification strategy, combining aerial imagery, permits, tax records, and AI, offers a blueprint for improvement and 97% national coverage.

- Explore why roof age is a predictor of losses across multiple perils, not just wind and hail.

- Discover the one-two punch of verified roof age and real-time condition insights, delivering a complete view of risk, even for young roofs with hidden problems.

- Align your roof age data with growing regulatory expectations, particularly in states like Florida.

Deferred Maintenance Adds $317B in Exposure for Insurers

New research from ZestyAI reveals that 62% of U.S. homeowners are deferring critical home maintenance, adding up to $317 billion in potential claims exposure for insurers.

These findings come as Severe Convective Storms (SCS) caused an estimated $58 billion in insured losses in 2024, surpassing hurricane-related losses and marking the second-costliest SCS year on record.

Tornadoes, hail, and wind events now account for over 60% of all U.S. catastrophe claims, and research from the Insurance Institute for Business & Home Safety (IBHS) shows that roof damage accounts for up to 90% of residential catastrophe losses.

Key Findings from ZestyAI’s Homeowner Survey

According to ZestyAI’s nationally representative survey, 62% of homeowners have delayed essential repairs due to budget constraints, representing nearly 59 million U.S. homes with unaddressed vulnerabilities. Forty percent said they would rely on an insurance claim to cover major repairs like roof replacement, adding up to an estimated $317 billion in potential exposure for carriers.

Alarmingly, 63% of homeowners who weren’t living in their home at the time of the last roof replacement don’t know how old their roof is, making it even harder to detect aging systems before they fail. Meanwhile, 12% admitted they would delay repairs indefinitely, further increasing their risk of property damage.

Severe Convective Storms: The Growing Catastrophe Risk

This blind spot compounds known risks: prior ZestyAI analysis has identified over 12.6 million U.S. properties at high risk for hail-related roof damage, representing $189.5 billion in potential roof replacement costs.

“Deferred maintenance has long been a known risk factor, but today the stakes are higher than ever,” said Kumar Dhuvur, Co-Founder and Chief Product Officer of ZestyAI. "With claim severity rising and storm losses compounding, insurers need more than hazard maps to navigate this landscape."

"Property-level insights allow carriers to proactively address known vulnerabilities, improve underwriting precision, and work with homeowners to reduce losses before they happen.”

ZestyAI’s findings support a growing push toward data-driven, preventative underwriting strategies, especially as carriers face rising claim severity and pressure to improve combined ratios across storm-prone states.

.webp)

Now Streaming: LA Fires in Focus – What Insurers Need to Know

What Worked, What Didn’t, and What’s Next for Insurers

With insured losses projected to exceed $30 billion, the recent Los Angeles wildfires rank among the costliest in U.S. history—reshaping how insurers think about risk, resilience, and readiness.

Watch the Full Webinar → LA Fires in Focus: What Insurers Need to Know

In this on-demand webinar, experts from the Insurance Institute for Business & Home Safety (IBHS), the Western Fire Chiefs Association, Cal Poly’s WUI Fire Institute, and ZestyAI unpack what really happened—from frontline response to lab-based research and model performance—and share critical strategies insurers can use to prepare for what’s next.

Watch this session if you’re a Product Managers, Underwriters, Actuaries, and Risk & Innovation leaders looking to make informed decisions in an increasingly volatile wildfire landscape.

What You’ll Learn

- Key takeaways from the Los Angeles wildfires

- Research on structure-to-structure fire spread and resilience factors

- How wildfire risk models performed—what we got right (and wrong)

- Practical strategies to reduce exposure and strengthen resilience

Meet the Experts

- Anne Cope, Chief Engineer, IBHS

- Bob Roper, CEO, Western Fire Chiefs Association

- Frank Frievalt, Director, WUI Fire Institute at Cal Poly

- Kumar Duhvur, Co-Founder & CPO, ZestyAI

Now Streaming: LA Fires in Focus – What Insurers Need to Know

What Worked, What Didn’t, and What’s Next for Insurers

With insured losses projected to exceed $30 billion, the recent Los Angeles wildfires rank among the costliest in U.S. history—reshaping how insurers think about risk, resilience, and readiness.

Watch the Full Webinar → LA Fires in Focus: What Insurers Need to Know

In this on-demand webinar, experts from the Insurance Institute for Business & Home Safety (IBHS), the Western Fire Chiefs Association, Cal Poly’s WUI Fire Institute, and ZestyAI unpack what really happened—from frontline response to lab-based research and model performance—and share critical strategies insurers can use to prepare for what’s next.

Watch this session if you’re a Product Managers, Underwriters, Actuaries, and Risk & Innovation leaders looking to make informed decisions in an increasingly volatile wildfire landscape.

What You’ll Learn

- Key takeaways from the Los Angeles wildfires

- Research on structure-to-structure fire spread and resilience factors

- How wildfire risk models performed—what we got right (and wrong)

- Practical strategies to reduce exposure and strengthen resilience

Meet the Experts

- Anne Cope, Chief Engineer, IBHS

- Bob Roper, CEO, Western Fire Chiefs Association

- Frank Frievalt, Director, WUI Fire Institute at Cal Poly

- Kumar Duhvur, Co-Founder & CPO, ZestyAI

Now Streaming: LA Fires in Focus – What Insurers Need to Know

What Worked, What Didn’t, and What’s Next for Insurers

With insured losses projected to exceed $30 billion, the recent Los Angeles wildfires rank among the costliest in U.S. history—reshaping how insurers think about risk, resilience, and readiness.

Watch the Full Webinar → LA Fires in Focus: What Insurers Need to Know

In this on-demand webinar, experts from the Insurance Institute for Business & Home Safety (IBHS), the Western Fire Chiefs Association, Cal Poly’s WUI Fire Institute, and ZestyAI unpack what really happened—from frontline response to lab-based research and model performance—and share critical strategies insurers can use to prepare for what’s next.

Watch this session if you’re a Product Managers, Underwriters, Actuaries, and Risk & Innovation leaders looking to make informed decisions in an increasingly volatile wildfire landscape.

What You’ll Learn

- Key takeaways from the Los Angeles wildfires

- Research on structure-to-structure fire spread and resilience factors

- How wildfire risk models performed—what we got right (and wrong)

- Practical strategies to reduce exposure and strengthen resilience

Meet the Experts

- Anne Cope, Chief Engineer, IBHS

- Bob Roper, CEO, Western Fire Chiefs Association

- Frank Frievalt, Director, WUI Fire Institute at Cal Poly

- Kumar Duhvur, Co-Founder & CPO, ZestyAI

Connecticut Insurance Department Green Lights AI-Powered Roof Quality Solution

Insurers can leverage AI-driven, property-specific roof condition insights for more accurate underwriting and rating decisions across the state

ZestyAI today announced that the Connecticut Insurance Department (CID) has formally approved its Roof Quality solution for use in residential property underwriting.

CID conducted a comprehensive third-party actuarial review of ZestyAI’s model, evaluating methodology, data integrity, and regulatory compliance against its rigorous standards.

What CID’s Approval Means for Carriers

Part of Z-PROPERTY™ , the Roof Quality model enables insurers to assess and price roof risk with unmatched accuracy.

By combining 3D property analysis, high-resolution aerial imagery, and AI trained on extensive real-world data, the platform replaces subjective or incomplete assessments with objective, property-specific intelligence.

The model classifies roofs into five standardized condition levels, helping insurers assess property risk with greater precision. It distinguishes between surface-level wear and structural issues, flagging meaningful signs of deterioration such as missing shingles, tarps, or water pooling.

Bryan Rehor, Director of Regulatory Affairs at ZestyAI, said:

“Roof condition is one of the strongest predictors of loss, yet historically one of the hardest to assess without costly inspections. This approval affirms the accuracy, fairness, and transparency of our approach and reflects our broader commitment to aligning innovation with consumer protection.”

How ZestyAI’s Roof Quality Model Improves Risk Assessment

ZestyAI maintains active engagement with the National Association of Insurance Commissioners (NAIC) and state-level departments to ensure its models meet evolving standards for fairness, transparency, and consumer protection.

By proactively filing through in-house Rating and Advisory Organizations, ZestyAI ensures its models meet the strictest regulatory standards before reaching the market.

ZestyAI’s models are trusted by regulators and insurers to assess risk in the nation’s most climate-exposed regions with Z-FIRE, ZestyAI’s wildfire risk model, approved by regulators in all western states. Its Severe Convective Storm suite is approved in 16 states across the Midwest, Great Plains, and South.

Farmers and Mechanics Mutual Insurance Company of West Virginia Adopts ZestyAI to Strengthen Underwriting and Risk-Based Pricing

AI-powered property risk insights support greater rating precision, lower inspection costs, and smarter underwriting decisions across West Virginia.

ZestyAI today announced a new partnership with Farmers and Mechanics Mutual Insurance Company of West Virginia (FMIWV) to strengthen underwriting accuracy and improve risk-based pricing.

Why Accurate Roof Data Matters More Than Ever

Roof claims are the leading driver of insurance losses, yet many carriers still depend on self-reported data, which can be unreliable, or physical inspections, which are costly and hard to scale. Recent research shows that 15% of roofs are at least eight years older than reported, highlighting the need for more reliable, data-driven alternatives.

To address long-standing challenges in accessing reliable property insights, FMIWV selected Z-PROPERTY™.

Why FMIWV Chose Z-PROPERTY

Dan Otto, Senior Vice President and Chief Financial Officer at FMIWV, said:

"After evaluating several options in recent years, we chose ZestyAI based on their strong coverage and ease of implementation. Getting started using the technology was easy. We’re particularly focused on using their property insights to provide additional underwriting information for new business and renewals.”

ZestyAI’s advanced insights help FMIWV:

- Identify high-risk properties early to prioritize mitigation and prevent losses

- Enhance risk selection and pricing precision with objective, property-level data

- Reduce inspection costs and turnaround time by minimizing the need for on-site assessments

- Streamline straight-through processing for low-risk properties to improve efficiency and speed to bind

- Reduce premium leakage by aligning pricing with actual exposure

“FMIWV is showing how regional carriers can lead with data-driven underwriting that improves operations and elevates the customer experience,” said Attila Toth, Founder and CEO of ZestyAI.

“By grounding decisions in reliable, property-level data, they’re improving efficiency, reducing risk, and raising the bar for underwriting and rating precision.”

Wildfire Risk Across the Nation

We’ve created a visual guide to where wildfire risk is rising—and where opportunities for mitigation exist.

Wildfire Risk Is Rising Nationwide

Wildfire seasons are getting longer, more destructive, and harder to predict—and they’re no longer just a Western U.S. concern. From the Southeast to the Midwest, wildfire risk is emerging in places many insurers haven’t traditionally watched.

What the Latest Data Reveals About Wildfire Exposure

Drawing from the latest national datasets and insights from ZestyAI’s Z-FIRE™ model, this visual guide to wildfire risk in the U.S. shows:

- New wildfire hotspots: Discover where risk is rising fastest.

- Mitigation gaps: Learn how a lack of defensible space is putting thousands of homes in danger across the country.

- Top risk drivers: See how features like overhanging trees and wooden roofs are fueling destruction in high-risk areas.

BONUS: You’ll also get access to our latest online event with IBHS and Western Fire Chiefs Association, The LA Fires in Focus: What Worked, What Didn’t, What’s Next for Insurers.

ZestyAI Product Updates: Smarter Models, Faster Workflows, and Richer Imagery

At ZestyAI, we’re continually enhancing our platform to help insurers better understand property risk, strengthen underwriting precision, and streamline operations. Over the last few months, our team has launched a series of updates that make our AI-powered solutions even more powerful and accessible.

From improvements in roof geometry and manufactured home modeling to expanded wildfire data on home hardening and structural vulnerability, plus faster APIs and faster APIs, these updates reflect our deep commitment to product excellence and customer success.

Smarter Risk Modeling for Manufactured Homes

Updated Manufactured Home Model in Z-PROPERTY

We’ve released an upgraded model for manufactured homes within Z-PROPERTY, trained on a broader set of imagery sources to improve data coverage and model accuracy.

This new version reduces the false positive rate, giving carriers greater confidence when evaluating mobile home risk—a critical upgrade for lines of business that rely on nuanced property insights.

Better Roof Geometry Analysis with the Roof Facet Model

Enhanced Accuracy and Speed in Roof Modeling

As part of our Digital Roof product, the Roof Facet model has been refined to deliver sharper roof geometry insights with faster processing times. This enhancement is especially valuable for customers scoring large portfolios, improving both speed and data quality.

Expanded Wildfire Risk Data Coverage

Compliance Pre-Fill Now Covers 99%+ of Wildfire Properties

We’ve expanded our Compliance Pre-Fill solution to support all wildfire-prone states, with property-level coverage now exceeding 99%. New on-demand access to critical wildfire mitigation features—including enclosed eaves, six-inch vertical clearance for siding, and noncombustible fencing—allows underwriters and compliance teams to make more accurate decisions with current data and zero added latency.

3D That Tells the Whole Story

Access to Richer 3D and Historical Imagery

ZestyAI now provides access to a broader and deeper catalog of high-resolution and historical imagery, powered by best-in-class sources of imagery. These enhancements improve underwriting workflows and allow insurers to “time travel” and evaluate how a property’s condition has changed over time.

This capability is especially valuable in regulatory environments that require proof of property degradation before policy changes are made. Historical imagery also gives underwriters a fuller view of prior conditions, providing context for past underwriting decisions.

Performance Gains Across All APIs

Reduced Latency and Improved API Response Times

We’ve optimized our APIs to significantly reduce latency, improving the speed and reliability of data delivery across all ZestyAI products. Whether batch scoring, running real-time underwriting, or executing renewal workflows, you’ll experience faster performance and greater efficiency—saving valuable time across your organization.

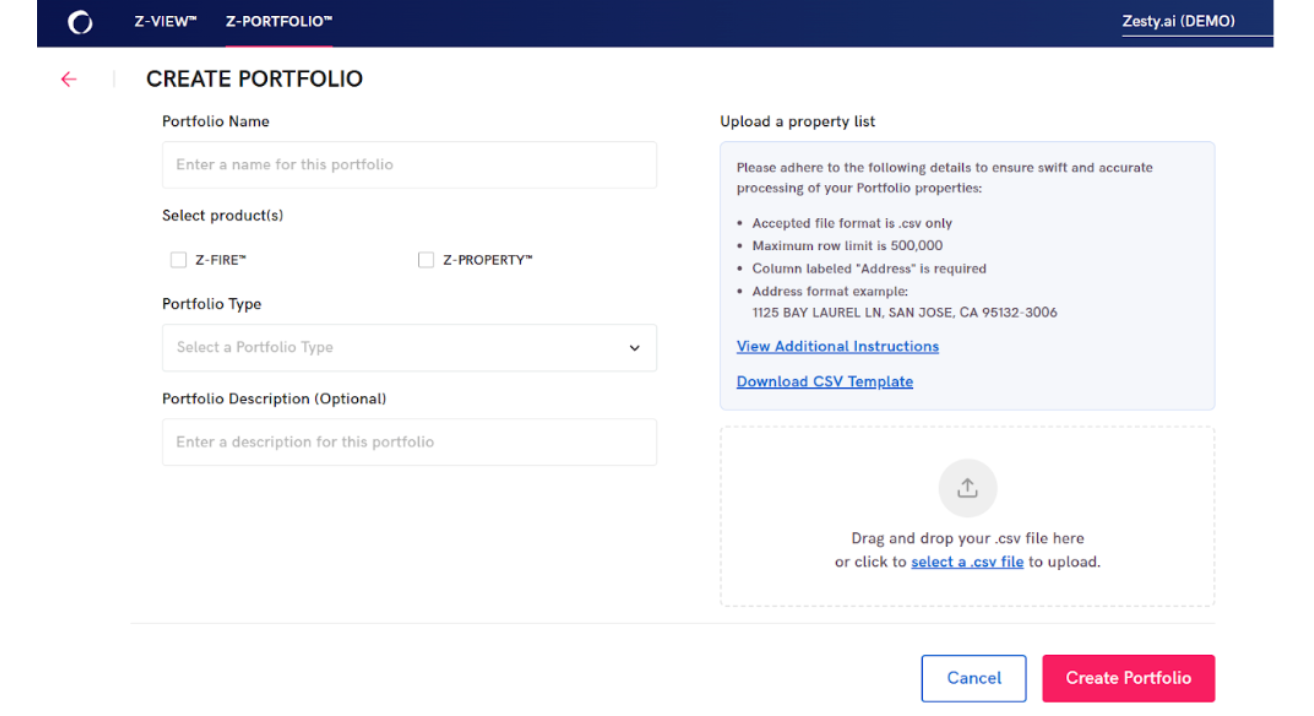

A New and Improved Upload Experience in Z-PORTFOLIO

Redesigned Upload Page for Streamlined Workflow

We’ve redesigned the Z-PORTFOLIO upload experience to make portfolio submissions more intuitive and efficient. Instructions and templates are now centralized in one place, and users can specify the purpose of the upload—such as renewal or dislocation analysis—to unlock deeper insights into usage patterns. This update enhances the self-service experience and helps customers extract maximum value from portfolio analyses.

Driving Continuous Innovation in Insurance Risk Intelligence

These product updates are more than just technical enhancements; they’re part of a larger mission to transform property risk assessment through AI. By improving model precision, reducing friction in workflows, and delivering richer, more current data, we’re helping insurers stay ahead of emerging risks and changing market demands.

If you’d like to learn more about any of these updates or request a demo, reach out to your Customer Success Manager or contact us below.

Why Non-Weather Water Losses Are Quietly Eroding Profitability

New research reveals how insurers can rethink their strategy for the 4th costliest peril in homeowners insurance

The Silent Peril Reshaping Homeowners Insurance

Non-weather water damage rarely makes headlines, but it’s quietly eroding profitability across the country.

It is now the fourth costliest peril in homeowners insurance, and claim severity has increased 80% in the last decade—a trend that’s accelerating even as frequency remains relatively flat.

Traditional risk models struggle to capture the early warning signs behind these losses, leading to mispriced policies, undetected exposure, and rising volatility for carriers.

Want the full analysis? Download the complete “Winning the Fight Against Non-Weather Water Losses” guide.

Why Loss Severity Keeps Rising

Aging homes and overlooked system failures

Many of the most expensive losses stem from aging plumbing, deteriorating materials, and slow-burn failures that often go undetected until damage is significant.

Frequency is flat—severity is not

Loss patterns suggest that while the number of events hasn’t surged, the financial impact of each event has—a signal that traditional models are not capturing the right property-level predictors.

The Property Features Most Predictive of Water Losses

The overlooked attributes that traditional models miss

Standard territory- or age-based assessments often ignore the property-specific details that meaningfully influence water loss risk, including:

- supply line material and age

- plumbing configuration

- occupancy patterns

- system maintenance and upgrades

- moisture exposure and prior loss indicators

These factors vary widely between neighboring homes—yet most models treat them as identical.

Where Traditional Underwriting Falls Short

ZIP-code and age-based proxies mask true risk

Legacy approaches rely heavily on broad territory-level assumptions that overlook structural vulnerabilities and system conditions.

Limited visibility creates mispriced policies

Without property-level insight, high-risk homes are often underpriced while lower-risk homes subsidize them—driving loss ratio volatility over time.

Get deeper insights on the drivers of water loss severity in our full guide → “Winning the Fight Against Non-Weather Water Losses”

How AI and Property-Level Data Are Changing the Landscape

AI models trained on real-world claims data can identify early signals of potential water loss by analyzing the interaction between:

- plumbing systems

- property attributes

- historical patterns

- material degradation

- repair history

This enables carriers to segment risk accurately, adjust pricing, and reduce preventable losses—long before small issues turn into major claims.

What Homeowners Actually Understand About Water Risk

Misconceptions around coverage and prevention

ZestyAI’s research shows that many policyholders:

- misunderstand what is and isn’t covered

- underestimate how much damage water can cause

- rarely take preventive actions unless prompted

This disconnect creates an opportunity for carriers to strengthen education, mitigation, and customer engagement.

Steps Carriers Can Take Today

Improve segmentation and rating accuracy

Property-level signals enable more precise risk tiers and more stable long-term portfolios.

Strengthen mitigation and reduce loss severity

Insights help identify which homes are at elevated risk and where targeted mitigation can reduce exposure.

Enhance underwriting workflows with explainable insights

Transparent, explainable AI helps underwriters understand the key drivers behind elevated risk—supporting both decision-making and regulatory review.

Get the Full Guide

Our new research paper, Winning the Fight Against Non-Weather Water Losses, breaks down the trends reshaping this growing peril—and the strategies carriers can use to get ahead of it.

Access the Guide

See How Insights Turn Into Decisions

ZestyAI transforms data into action. Get a demo to see how the same AI powering our reports helps carriers make faster, smarter, regulator-ready decisions.