Under the Microscope: The Real Cost of the CDI’s Recently Proposed Changes

Insurance in California is evolving and insurers need the right tools to stay ahead of the curve.

Time To Get Ready: The CDI Is Opening the California Market

The recent wave of regulatory movement in California marks a significant opportunity for insurance providers. The California Department of Insurance (CDI) has announced a groundbreaking plan to create a path to allow CAT models in setting wildfire load in base rates, and to pass reinsurance costs directly to policyholders. At the same time, policyholders located in areas considered high-risk can expect to have more access to coverage above and beyond the insurer of last resort, the California FAIR Plan.

Amidst an insurance availability crisis, Commissioner Lara and the CDI have promised additional resources to expedite rate filing approvals. These measures have the potential to get the regulatory gears turning in favor of a more fluid market system.

In return, insurance carriers are expected to shoulder a more significant responsibility: increasing their market share in high-risk wildfire zones that they could previously avoid altogether. This directive aims to lighten the load on the California FAIR Plan. The changes are expected to be finalized in 2024.

Key Takeaway

The CDI is paving the way to a more open California market. But, this openness comes at a price – requiring carriers to skillfully navigate high-risk areas that could previously be avoided.

The Double-Edged Sword of the New Regulations: Adverse Selection

Adverse selection is the unseen undertow in insurance, capable of dragging down even the most robust portfolios. At its core, it thrives on information asymmetry. The classic instance being when a life insurance applicant is privy to more details about their health risks than the insurance company, resulting in miscalculated premiums.

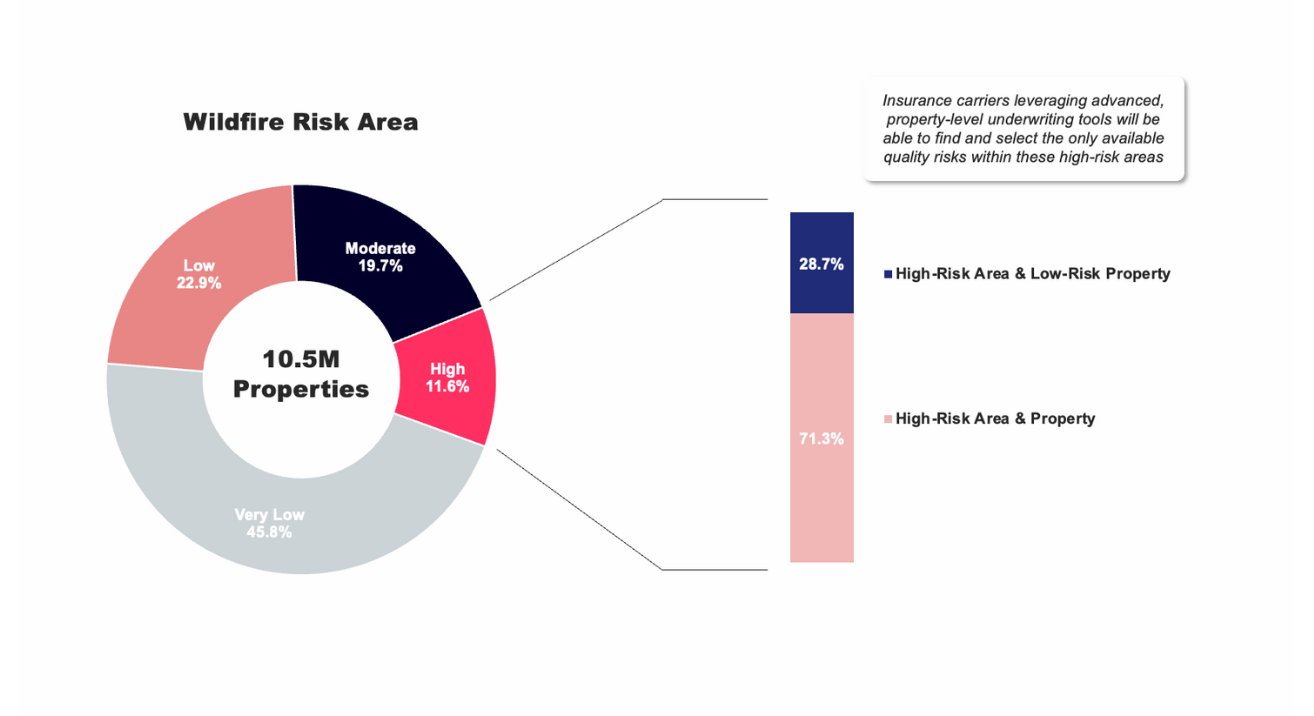

In the world of property insurance, the echo of adverse selection becomes louder when there's an imbalance of knowledge among carriers. The upcoming regulatory shifts will push carriers to pull from the same pool of policies in high-risk areas. Yet, those equipped with richer data will artfully zero in on properties within "high-risk zones" that, in actuality, present minimal hazards; properties with flat slopes, large defensible space, compliance with modern building codes, and fire resistant materials.

This new insurance landscape creates a backdrop where well-informed carriers siphon off the cream of the crop, leaving the lesser-known, higher-risk properties for the wider market. Amplifying this divide are sophisticated, property-specific pricing models. Carriers not armed with granular insights might unknowingly overburden their lower-risk policies, inadvertently raising prices in seemingly secure zones. The domino effect? Their portfolio’s competitive edge wanes and the overall book reshapes due to noncompetitive pricing.

Carriers not armed with granular insights might unknowingly overburden their lower-risk policies, inadvertently raising prices in seemingly secure zones.

In order to navigate these high-risk areas (adverse selection aside) users with traditional, ZIP code-based models will be unequipped to effectively navigate these areas. Relative risk levels in these high-risk areas are not likely to differ much when the risk assessment tool being used only provides a regional assessment of the hazard probability.

The battle will be fought finding and selecting the properties with the highest likelihood of survival. For this task, carriers need a property-specific model, designed and built to split risk within a fire perimeter. Which properties will survive? Which ones will sustain only smoke damage? Which ones will be a total loss? None of these questions are answered by stochastic models today.

Key Takeaway

While the regulations aim to make the insurance landscape more inclusive, they introduce risks that can only be intelligently navigated with superior insights and tools. There is a small pool of favorable policies to fight for, and they will go to carriers with a property-specific lens.

The Power of Precision: Property-Specific Models

Remember your school days when, armed with a magnifying glass, you would excitedly explore the minuscule wonders of the world? That was just scratching the surface. The real magic lay beneath, visible only through the potent lens of a microscope.

In the insurance realm, stochastic models are akin to those magnifying glasses. They offer a better view of risk and can be useful for portfolio management and reinsurance use-cases, but they miss the intricate details for individual risk selection. Enter AI-powered, property-specific models like Z-FIRE, the microscopes of the insurance world.

ZestyAI’s Z-FIRE model has quickly become the leader in property-specific wildfire risk assessment. Using AI trained on more than 1,500 wildfire events across 20 years of historical loss data, Z-FIRE provides accuracy and transparency that is of essential value to both insurers and homeowners. The model considers features such as topography and historical climate data in combination with factors extracted from high-resolution imagery of the property itself and its surroundings, including property owner and community mitigation efforts, to provide both neighborhood and property-specific risk scores. ZestyAI’s Z-FIRE model was built with regulatory compliance in mind and has been widely adopted across the Western US including California, where its use has been approved for both underwriting and rating.

ZestyAI’s Z-FIRE model was built with regulatory compliance in mind and has been widely adopted across the Western US including California, where its use has been approved for both underwriting and rating.

While stochastic models provide an overarching portfolio view, their capabilities are restrictive when it comes to identifying the safest properties.

The holistic approach of models like Z-FIRE delves into factors often overlooked, such as:

- True granularity in data, capturing each property's unique risk profile.

- Frequent updates, ensuring the data reflects the current risk landscape.

- A multivariate understanding of risk, considering several factors together.

- Being deeply rooted in actual loss data, offering a clear picture of potential claims.

- Furthermore, while stochastic models demand manual input of secondary modifiers, Z-FIRE offers an automated, granular analysis, transitioning the perspective from a broad territorial view to an individual property's precise risk assessment.

Even in the most challenging environments, the model’s robustness and risk-splitting power speaks for itself.

Key Takeaway

The nuances of property-specific risks take center stage with the proposed changes, and the stakes are too high to navigate the market with a blindfold. A shift from generic models to AI-powered, granular insights is needed - precision is the ultimate competitive advantage.

Take the Leap Into the Future

Insurance in California is evolving, and with tools like Z-FIRE, you can stay ahead of the curve. Don't leave your decisions to chance. Arm yourself with precision, clarity, and insight. Reach out to the ZestyAI team today, and together, let's redefine insurance in the Golden State.

Want industry-leading wildfire risk insights?

Get a demo of Z-FIRE!