Streamlining Appeals and Enhancing Transparency

ZestyAI’s Appeals is the latest evolution in the Z-FIRE model putting control in the hands of carriers and consumers.

Adapting to Today’s Dynamic Regulatory Environment

ZestyAI’s Z-FIRE was the first AI-powered climate risk model to be approved as part of a carrier rate filing in California in 2021. A lot has changed since that original approval - both in terms of the regulatory environment and in how the Z-FIRE model has grown and adapted to meet and anticipate those regulatory changes.

ZestyAI’s regulatory team is deeply engaged with regulators, staying on top of emerging policies and legislation that may impact how a carrier can use our products. When new policies come into place, we are ready with updates to our technology, support, and documentation.

The Push for Transparency

Presently, regulators are continuing to push for additional transparency and accuracy in how insurers treat wildfire risk. AI-powered solutions, like Z-FIRE, provide a clear advantage because of their openness and interpretability.

Some states, like California and Oregon, have implemented mandates for insurers to communicate property-specific information related to wildfire risk to homeowners. Fostering this type of transparency is an excellent way for insurers and homeowners to work together to mitigate risk, but with this transparency, there will inevitably be times when home and business owners question the accuracy of the information and choose to appeal. For example, if homeowners have recently taken measures to mitigate wildfire risk, such as vegetation management or upgrading their roof, those efforts may not yet be reflected in the model used to determine their risk.

If homeowners have recently taken measures to mitigate wildfire risk, such as vegetation management or upgrading their roof, those efforts may not yet be reflected in the model used to determine their risk.

In these instances, it is important for the appeals to be handled quickly and easily, both for the sake of customer satisfaction and to be compliant with regulations. In California, for example, the new California Department of Insurance regulation, Mitigation in Rating Plans and Wildfire Risk Models, mandates that insurers respond to any appeal requests within 30 days with an updated wildfire risk classification.

Built-in Adaptation Makes for Easy Appeals

Many existing wildfire risk tools fall short of providing the necessary data for compliance, but the ZestyAI team understood from its customers that a fast and simple way to address appeals was needed in order to best serve property owners and be compliant with regulations. To do this, we created an appeals feature in Z-FIRE where the policyholder can ask the insurer to update features where a property- or community-specific mitigation action has been taken by the policyholder. Carriers are able to adjust the variables directly in the model to calculate a new risk score in real-time.

ZestyAI’s Z-FIRE Appeal helps carriers and policyholders better manage and mitigate the risk of wildfire on their property in two ways:

- Z-FIRE delivers transparency to carriers and policyholders into the top factors driving risk scores. This visibility empowers policyholders to prioritize mitigation actions to reduce risk.

- Z-FIRE scores can be appealed and revised in real-time as mitigation actions are taken, helping carriers appropriately price relative to risk and aligning incentives with policyholders.

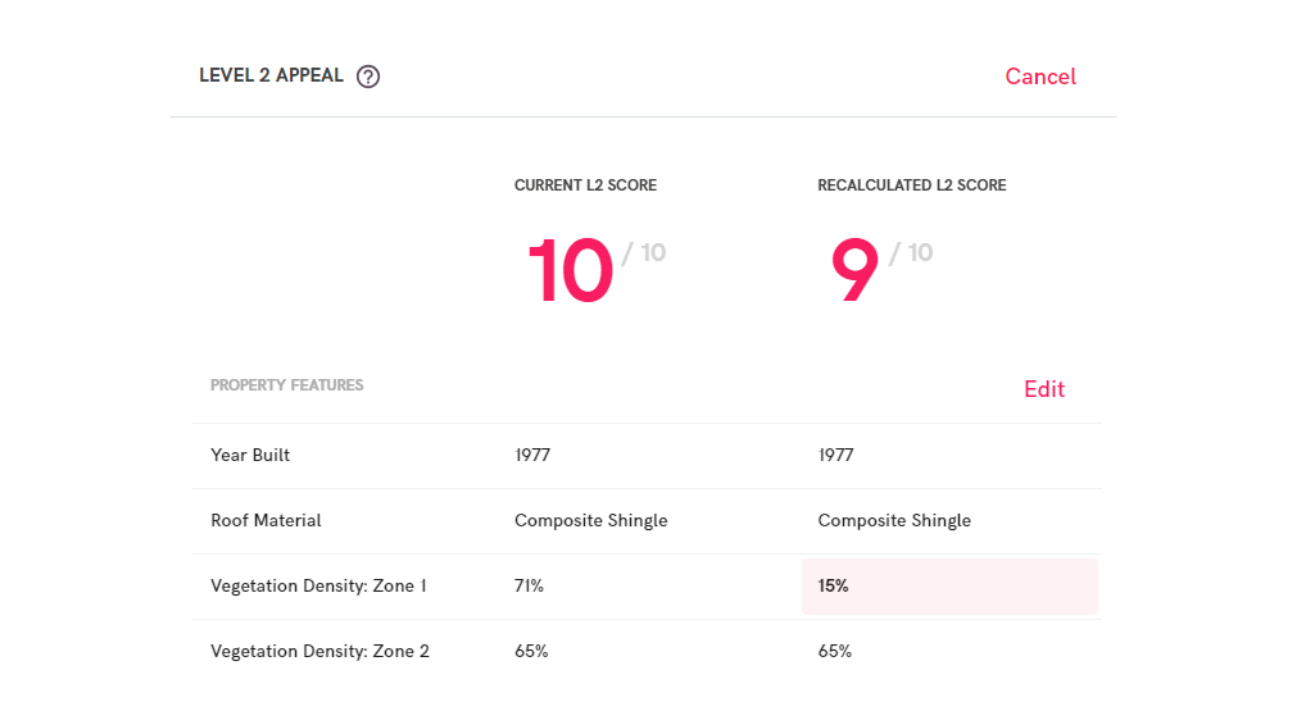

In the above example, the homeowner took mitigation steps to trim the vegetation around the property and reduce their risk of wildfire, taking their Zone 1 property vegetation from 71% to 15%. The homeowner can work with the carrier to update their Z-FIRE score based on the vegetation recently removed, taking their overall Level 2 score from 10 to 9.

The potential resilience of every structure and what the communities and homeowners have done to prepare for wildfire exposure play a significant role in wildfire loss. Research from ZestyAI and IBHS shows that for a more precise understanding of potential losses, insurers need to assess the risk of each individual property.

Research from ZestyAI and IBHS shows that for a more precise understanding of potential losses, insurers need to assess the risk of each individual property.

Modern wildfire risk tools like ZestyAI's Z-FIRE analyze individual property features and measure the impact of those features on the probability of loss. They also factor in nearby vegetation, community preparations, local infrastructure, and the lay of the land, giving valuable information on how and why properties might be damaged by wildfires. These models don't just offer a simple risk score, they also help explain what makes a particular property vulnerable, providing valuable information to the insurer and homeowner about what steps can be taken to lower risk.

For more information on ZestyAI’s Z-FIRE and our Appeals Feature reach out to a team member today.