April 2026

Regulatory Zest

Accelerating approvals, enabling compliance, and shaping the future of insurance regulation

Welcome

I'm Bryan Rehor, Senior Director of Regulatory & Government Affairs.

Regulatory demands on AI-driven insurance models are rising, and we've built the team to match.

We've strengthened our Regulatory & Government Affairs capabilities to accelerate approvals, navigate emerging requirements, and engage directly with regulators.

This is the first edition of the Regulatory Zest, a periodic update from our team. Whether you're planning filings or just staying up-to-date, we hope you find this valuable.

Expanding Regulatory & Government Affairs

ZestyAI's Regulatory team has formally expanded into Regulatory & Government Affairs, reflecting a broader and more strategic role.

These are the four key areas:

1. Product Approval & Enablement

End-to-end filing strategy support, leveraging ZestyAI's Rate Service Organization (RSO) licenses to streamline approvals and reduce time to market.

2. Regulatory Policy & Standards

Monitoring and interpreting emerging state and NAIC requirements, and translating them into actionable guidance for product development and filings.

3. Government & External Affairs

Building trusted relationships with regulators and policymakers to drive alignment on AI-driven risk models.

4. Technical Leadership & Education

Delivering transparent, technically rigorous explanations of ZestyAI models to support regulatory review and build industry understanding.

This expanded scope enables ZestyAI to serve not just as a model provider, but as a strategic partner in navigating an increasingly complex regulatory environment.

Key Regulatory Developments

Recent developments in Colorado and Utah are shaping how carriers must demonstrate the use of advanced models in the context of property-level risk and mitigation.

Colorado (HB 1182) — Compliance Framework

Colorado's HB 1182 establishes a comprehensive wildfire regulatory framework effective July 1, 2026, requiring carriers to operationalize mitigation, transparency, and consumer engagement across underwriting and rating.

ZestyAI enables end-to-end compliance through a unified platform:

- Mitigation Integration — Z-FIRE incorporates defensible space, structure characteristics, vegetation, wildfire history, and fuel exposure directly into risk scoring.

- Consumer Transparency & Disclosures — Scores, ranges, relative position, key drivers, and mitigation impacts are delivered via API and Z-VIEW for clear, plain-language communication.

- Appeals & Governance — Z-VIEW provides a structured appeals workflow with audit trails, data correction, and regulator-ready documentation aligned with 10/30-day requirements.

- Filing & Model Transparency — Full support for filing documentation, including model methodology, rate impact analysis, and underwriting integration.

- Ongoing Policyholder Engagement — Quarterly imagery refresh and scenario planning ensure mitigation actions are continuously reflected in risk assessments.

Utah (HB 48 & R590-291) – Compliance Framework

Utah’s HB 48 and rule R590-291 establish a WUI-centered regulatory framework requiring insurers to anchor wildfire underwriting and rating decisions to the state-defined Wildland-Urban Interface (WUI) boundary and objectively demonstrate alignment.

The Zest

- Competing against 459 startups from around the world, ZestyAI recently came in second place at the Zurich Innovation Championship.

- As a result, ZestyAI has been partnering with legacy insurer, Zurich, to implement 21st-century insurtech solutions.

- Insights gained from the collaboration between ZestyAI and Zurich reveal the main challenges and keys to success when connecting insurtech startups with large insurers.

The insurtech space is rapidly expanding and the associated opportunities are never-ending. While more technology startups partner with large legacy insurance groups to implement innovation, the conversation around the dynamics of these collaborations increases.

These partnerships were one of many subjects covered at this year’s InsureTech Connect, the world’s largest gathering of insurance leaders and innovators. There, ZestyAI CEO Attila Toth was a featured participant of a four-person panel discussing the challenges present when joining current, state-of-the-art technology and traditional legacy insurers.

Because these apparent issues are not simply limited to the new technology being implemented, Toth was asked to share his thoughts on the keys to success when connecting advanced tech to traditional insurance groups.

Connecting 21st Century Tech to Traditional Legacy Insurers

One of the largest global insurance carriers with $33.4 billion gross premiums Zurich holds a global startup tournament, the Zurich Innovation Championship (ZIC). This year, ZestyAI won the silver medal at the championship among 459 startups from around the world.

As one of the winners, ZestyAI has gained unparalleled insight into making a smooth, successful connection between a 21st-century insurtech startup and a legacy insurer.

ZestyAI has been working with the global insurance group to leverage artificial intelligence to model the impact of natural catastrophes, such as wildfires, on communities and the business of insurance carriers.

Within 7 months of the inception of the partnership, the pair has concluded a successful pilot program within a business unit and is in the process of executing one with another. At InsureTech Connect, Toth shared the details of how the startup and legacy group made the connection work.

Major Challenges

The biggest challenge most legacy insurers and agile insurtech startups face in working with one another is syncing the startup’s funding cycle with a larger insurance company’s technology adoption cycle.

Toth explains that traditional adoption cycles for carriers are longer than those of startups funding cycles.

“Traditional technology adoption cycles for insurance carriers can range anywhere from 2 years to even 5+ years. On the other hand, venture capital funding cycles last only 12-18 months.”

During these cycles, both the carriers and startups must show proof of progress.

Between funding cycles, startups are required to provide clear evidence of success in the form of product and commercial milestones being met. Insurers, on the other hand, follow a different timeline and structure to award those contracts.

The difference between the insurtech startup’s funding cycle and insurer’s tech adoption cycle often leads to a lack of synchronization. Uncoordinated cycles then result in a myriad of failed pilots between underfunded startups and innovation-hungry large carriers.

Key Success Factors

To begin to bridge the gap, insurance companies must approach the unique partnership with insurtech startups differently than those with incumbent technology or data providers.

According to Toth, both parties would benefit from insurers rethinking their procurement processes with insurtech startups in mind.

“Traditional insurers should streamline their entire technology procurement processes when engaging with insurtechs. They should move from year-long vetting processes with overly rigorous info security reviews to quick pilots and exponentially increase the speed of their learning.”

Zurich proves to be a successful example of this structure. For instance, the carrier completely re-engineered its new technology evaluation process by establishing the ZIC, which acts as a structured, time-bound vetting process of global startups.

To shorten the long adoption cycle, Zurich began by narrowing down their list of tech startups at a country-level. Then, the selection process took place at the continent-level before finally ending on a global level.

In addition to rethinking processes around technology selection, there are three major elements, which must be in place for a successful partnership between the insurtech startup and the insurer:

- A well-constructed, thoroughly flushed-out business case needs to be agreed upon by both parties.

- The insurance company needs to assign a senior executive from the business to sponsor the initiative. Best if the executive has direct product and/or Profit & Loss oversight over the potential benefit provided by the partnership.

- Clear performance indicators need to be established up front to measure success at every step of the process.

According to Toth, Zurich is on the right track to more successful partnerships with insurtech startups.

“Through the ZIC, Zurich has found a creative solution to dramatically accelerate adoption of innovative new technologies,” Toth says. “I hope many more carriers and reinsurers will follow suit and rethink the way they engage with insurtech startups.”

About Zesty.ai

Zesty.ai is the leading partner for property & casualty insurance companies embarking on digital transformation. The company harnesses the power of artificial intelligence on cutting-edge data sources including aerial imagery to model risk to real property. Zesty.ai leverages predictive algorithms on 130+Bn data points to understand the potential impact of natural catastrophes on individual properties with unprecedented accuracy. Insurance companies rely on these property risk insights to make smart marketing, underwriting and rating decisions. For more information, visit https://zesty.ai.

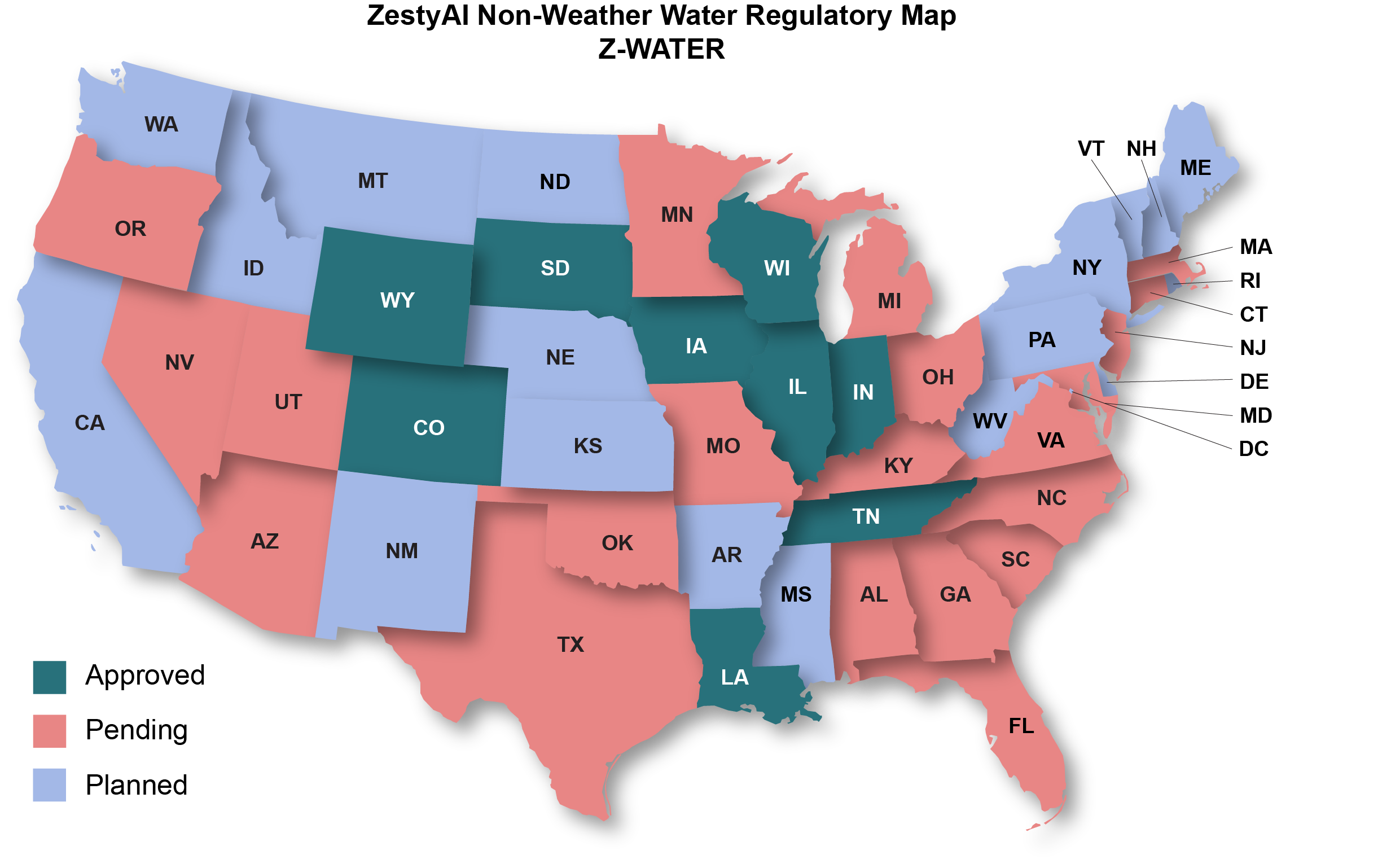

Filing Strategy: Scaling Adoption of Risk Models

ZestyAI continues to advance a proactive, scalable filing strategy focused on accelerating adoption of all of our models.

Across all programs, ZestyAI’s approach emphasizes:

- Clear documentation of model methodology and validation

- Alignment with state-specific regulatory requirements

- Reusable filing artifacts to improve speed and consistency

- Early and direct engagement with regulators to streamline review

.png)

Approval by Model

.png)

.png)

.png)

Planning filings in the next 6 - 12 months?

Now is the time to align on regulatory strategy. Our team is actively working with carriers to navigate these requirements.

Reach out to discuss your roadmap.