Roof Age in Rate Filings is Down: What’s Taking Its Place?

For the first time in two decades, regulatory filings using Roof Age have declined as a new standard emerges.

For years, insurers asked:

“How old is this roof?”

Now, the real question is:

“How will this roof perform?"

The way insurers assess roof risk has evolved significantly over the past two decades. What began as a simple Roof Age-based surcharge has transformed into a sophisticated approach that considers real-time condition, storm resilience, and structural complexity.

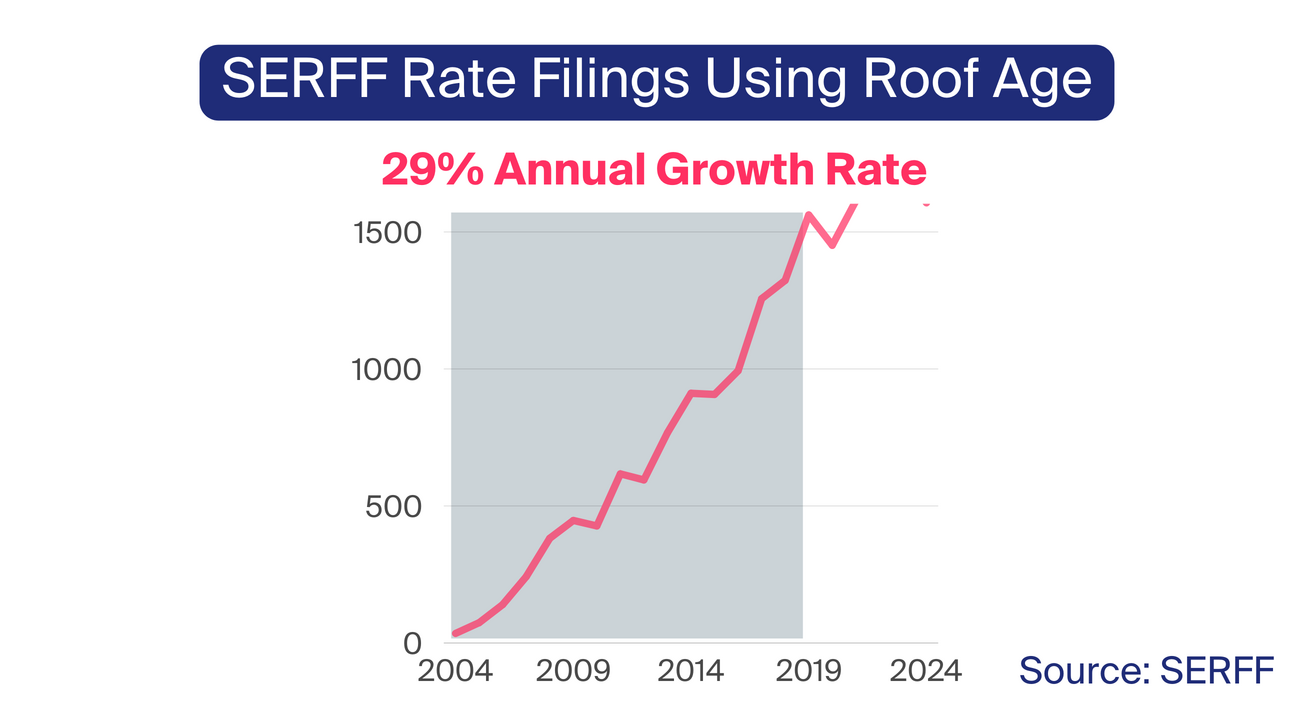

A closer look at SERFF regulatory filings traces the first recorded use of Roof Age back to 2004 when The Hartford introduced Roof Age-based pricing in Iowa.

At the time, the insurer applied a flat 10% surcharge to roofs 26 years and older—a figure that now seems outdated, as many carriers won’t insure roofs older than 15 years.

Roof Age quickly became a key rating factor—by the 2010s, Roof Age adoption in rate filings surged, growing at an annual rate of 29%.

If you fast forward just 10 years after The Hartford’s initial filing, you’ll find a stark contrast in how roof risk was assessed. By 2014, The Hartford’s rate filing in Iowa contained 51 pages of actuarial tables, detailing various roof materials and rate adjustment factors for age.

This shift reflected a broader trend—Roof Age moved from a simple surcharge to a more nuanced risk model that accounted for material durability, wear patterns, and structural longevity.

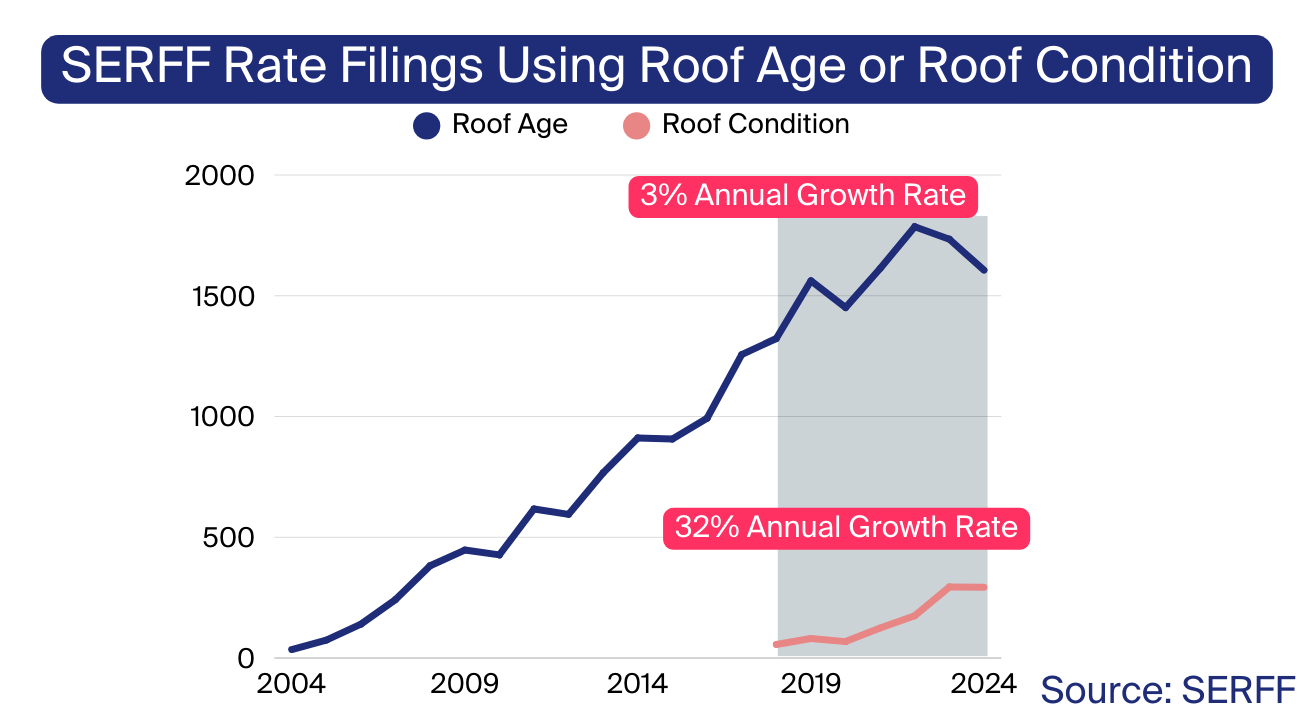

By 2018, insurers began looking beyond Roof Age, and that’s when Roof Condition first appeared in regulatory filings.

Over the past five years, its adoption has surged 32% annually, outpacing Roof Age at its peak. Insurers also began incorporating roof complexity variables, such as pitch and facets, to further refine their risk assessment models.

These advancements provided a more nuanced view of risk, moving beyond the assumption that all old roofs posed the same level of hazard.

Now, for the first time in two decades, Roof Age is plateauing. Over the past two consecutive years, we've seen a decline in the number of filings incorporating Roof Age, bringing its usage close to 2019 levels.

This decline suggests that carriers are moving toward more sophisticated approaches, leveraging real-time condition assessments rather than relying solely on the number of years since installation. After all, a 10-year-old roof in poor condition can present a greater risk than a 20-year-old roof that has been well-maintained—and insurers are recognizing the importance of capturing these distinctions.

With severe convective storm-related insured losses reaching $58 billion in 2024, traditional risk assessment methods can no longer keep up.

A new paradigm is emerging, where advanced AI-driven risk models provide the precision and resilience needed to navigate an increasingly volatile climate.

At ZestyAI, we’re helping insurers make this shift with models like Z-STORM, Z-HAIL, and Z-WIND, which are already filed and approved in 14 states, including Texas, Colorado, Illinois, Oklahoma, and Louisiana.

Those who embrace these innovations will gain a competitive edge—reducing loss costs, improving operational efficiency, and ultimately shaping the future of risk assessment in property insurance.